By: Russ Kamp, CEO, Ryan ALM, Inc.

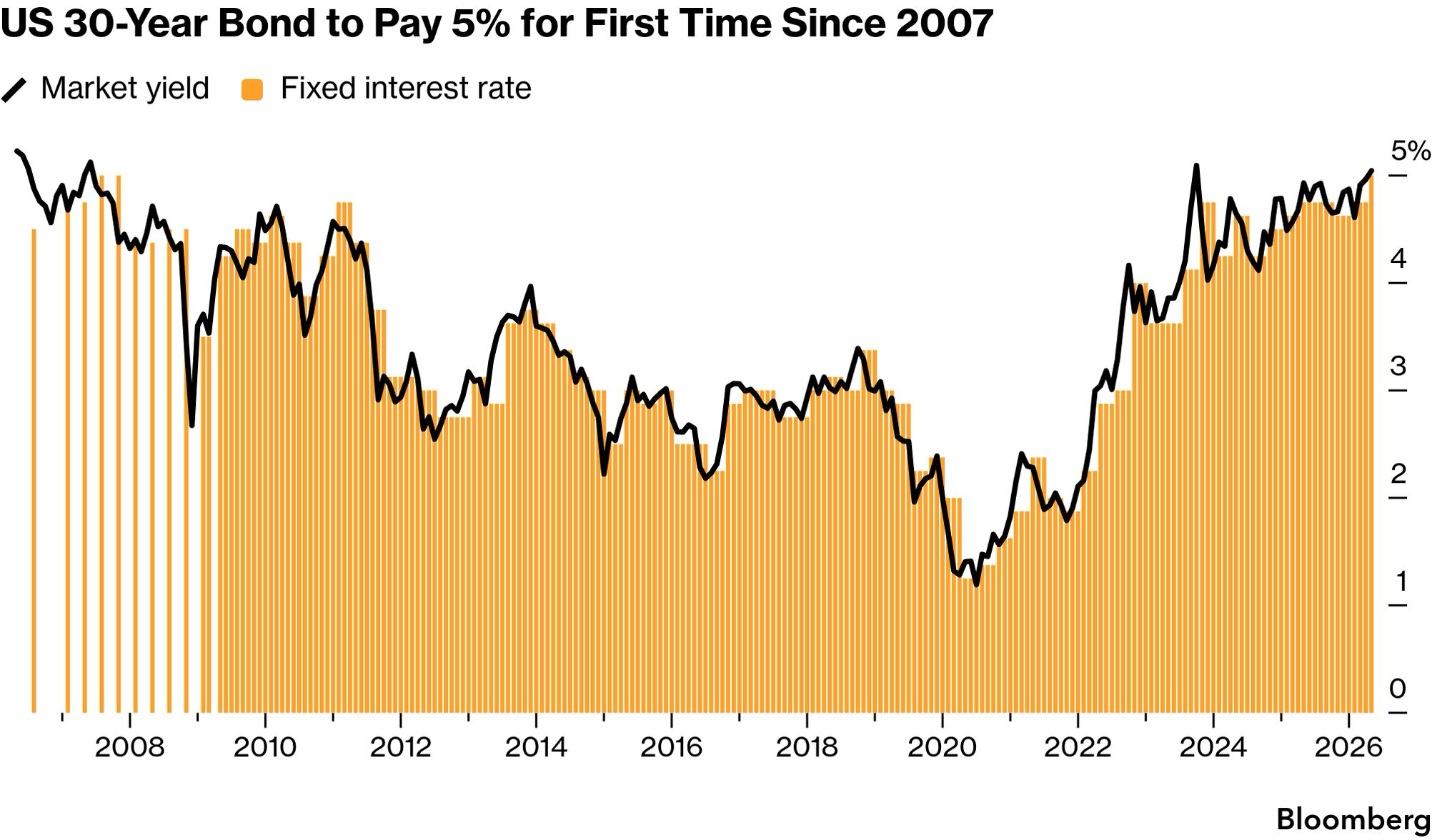

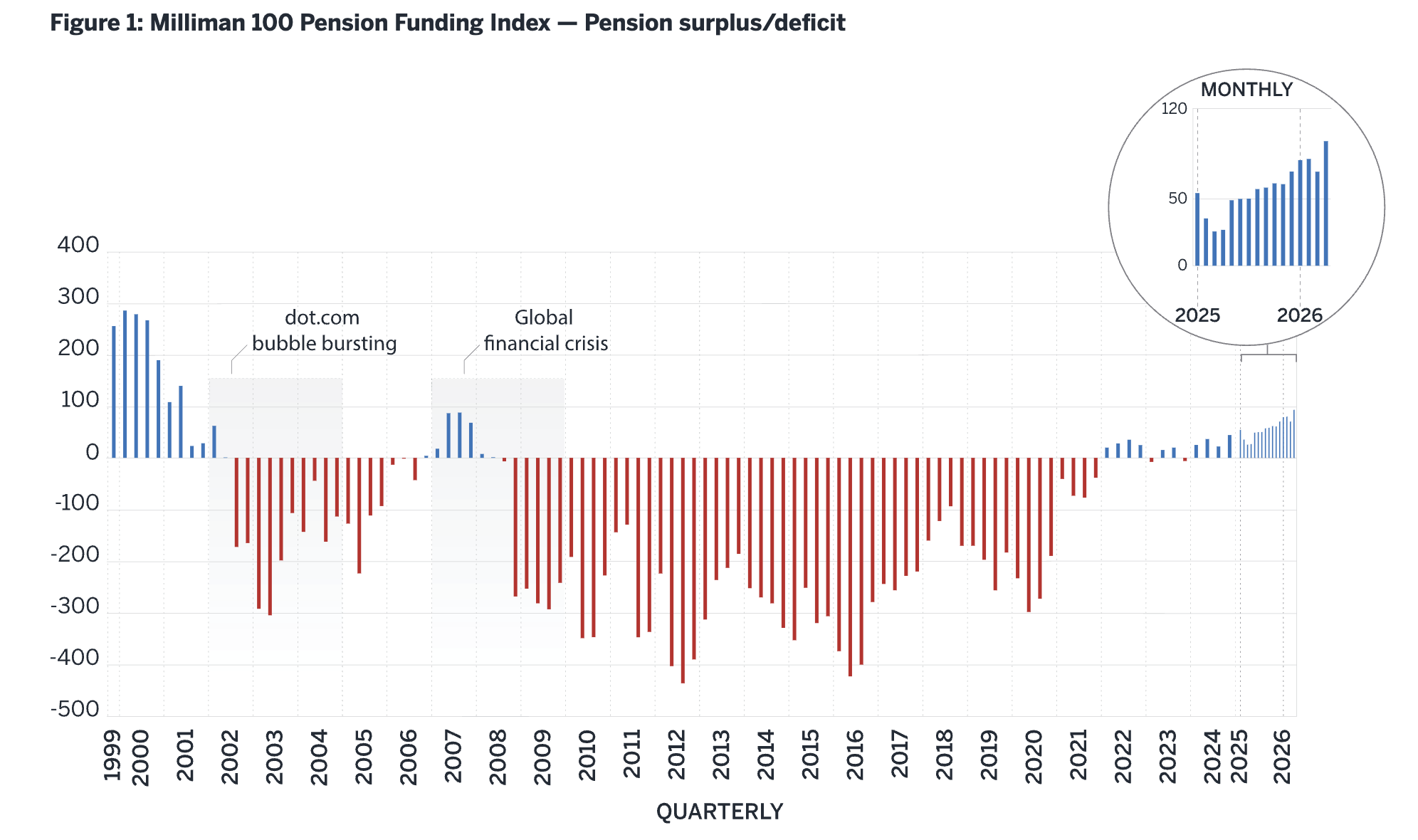

Rising interest rates can often create stresses in an economy and within the capital markets. They certainly make financing big ticket items more painful. They can destabilize equity markets, although it seems as if the current equity market is immune to any risk at this time. They harm most fixed income managers/strategies, as rising rates lower the present value of their bonds.

However, rising rates are GREAT for cash flow matching (CFM) strategies, as the higher rates reduce the cost of those future pension promises (benefit payments). We were recently asked by a public pension fund to provide them with an analysis of what CFM could potentially do for them in this environment. They provided us with the requisite data – projected benefits, expenses, and contributions as far into the future as possible – which we then ran through our cost optimization model that we call the Liability Beta Portfolio (LBP).

The output is compelling! We can secure this fund’s net (after contributions) liabilities (all of them!) through September 30, 2053. The future value (FV) of those liabilities is $86.2 million. However, the plan needs to set aside only $50.1 million in present value (PV) assets to defease those liabilities with certainty. The $36.1 million cost reduction is locked in on the day that the portfolio is created. That “savings” equates to a cost reduction of 41.9%!

So, this plan sponsor can now SECURE pension payments for 27-years. The residual assets not needed in the CFM portfolio can now grow unencumbered. If I were them I’d just buy a S&P 500 ETF creating considerable savings from lower management fees and far less complexity. Furthermore, the plan sponsor now knows what contributions will look like for the next nearly three decades. They won’t have to be alarmed should markets suffer a deep and extended correction, as the assets AND liabilities will move in lockstep.

By the way, these benefits were achieved without taking substantial risk, as our process only uses investment-grade corporate bonds rated BBB+ or better. Defaults, which are the only risk within the strategy, have been 0.2% (2/1000 bonds) annually for the last 40-years according to S&P.

Why use CFM? The benefits are incredible, including; certainty, security, all the necessary liquidity, an extended investing horizon, lower management fees, stable contributions, and improved sleep! If these benefits sound attractive to you, provide us the same info that our public fund prospect did (see above) and we’ll provide you with a free analysis, too. We are confident that you’ll be as blown away as they were and the many clients that we are proud to support.