By: Russ Kamp, CEO, Ryan ALM, Inc.

Clara Peller became famous as a result of her participation in the 1984 Wendy’s ad campaign in which she famously asks, “where’s the beef?”. Her comment was of course in reference to Wendy’s competitors whose burgers were less than impressive in size.

Yesterday, I produced a post highlighting the many benefits of cash flow matching (CFM), including providing ALL the necessary liquidity, creating an extended investing horizon, providing certainty and security, lower management fees, stable contributions/funded ratio, and the elimination of interest rate risk.

Despite the plethora of benefits, we occasionally receive push back from plan sponsors and their advisors on the use of CFM because some folks believe that they can identify a fixed income manager or group of bond managers that will “outperform” a CFM portfolio thus supporting the ROA target, as if that was the primary objective. As we’ve stated many times, the primary objective in managing a defined benefit plan is to SECURE the promised benefits at a reasonable cost and with prudent risk. It is NOT a return objective.

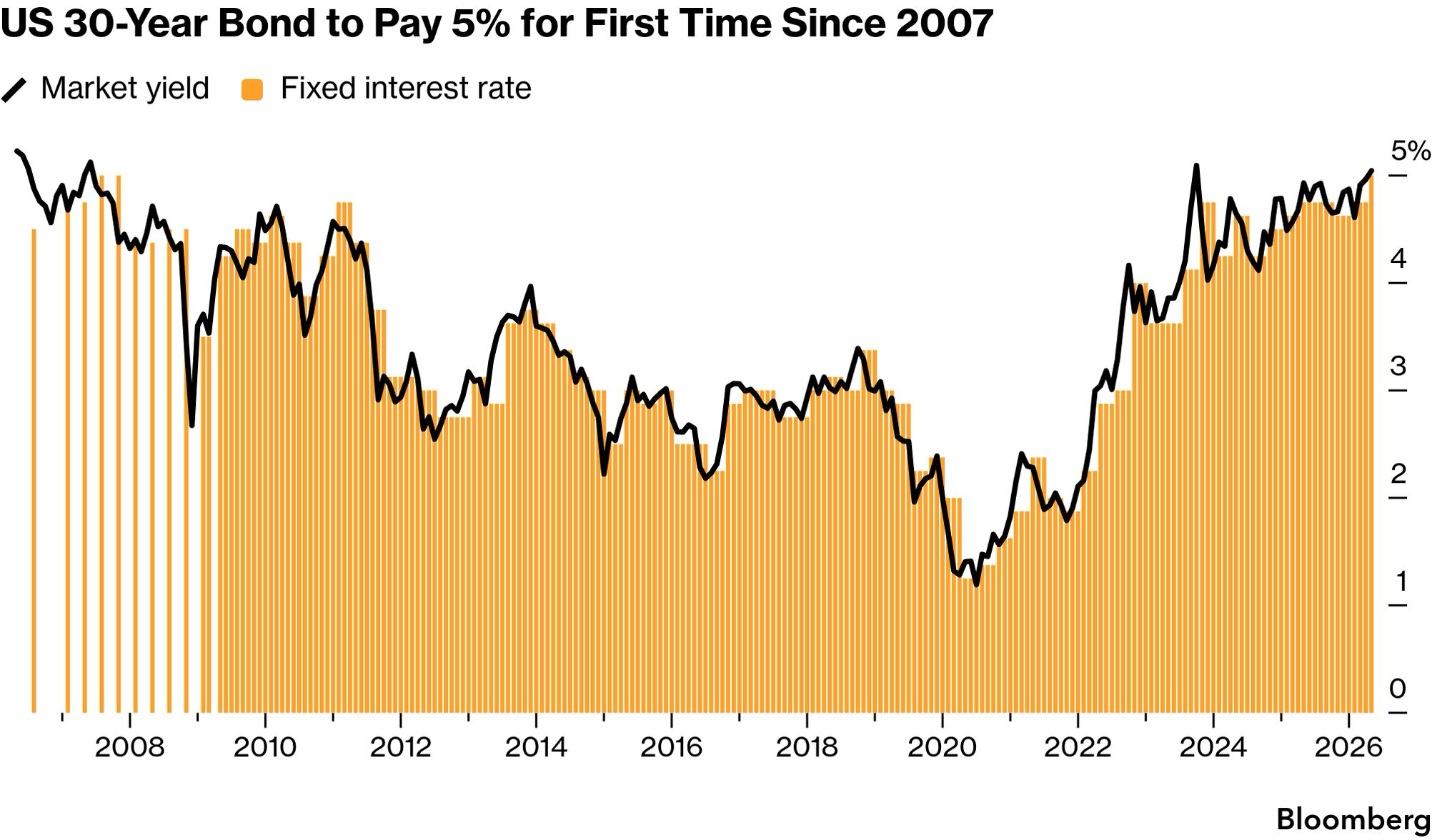

But, let’s just say for argument’s sake that using bonds in your fund was for return purposes. The greatest risk in managing U.S. fixed income is interest rate risk. Yes, most of us grew up in this industry during the last 40+ years when interest rates declined from ridiculous levels (10-year Treasury yield was 15.1% on the day I entered this business (October 1981)) to the zero-rate environment created by Covid-19. Most core fixed income managers continue to use the Barclays Aggregate (formerly Lehman) Index as the benchmark. The YTW on that index is 4.67%. A yield that is certainly below most, if not all, ROA targets for DB pensions (certainly public and multiemployer plans). Moreover, the yield on the Ryan ALM CFM is over 5.00% since it is a portfolio of primarily A/BBB+ corporate bonds. Our CFM should outperform the Agg by the yield difference given the same or similar duration.

Furthermore, that core fixed income manager(s) will actively position exposures related to the types of bonds, including Treasuries, agencies, MBS/ABS/CMOs, corporates, duration, sectors, etc. relative to the index to try to capture some excess return. But is “active management” adding value and what is the annual volatility or standard deviation associated with that activity? Many bond investors benefited from the nearly 4 decade decline in rates, as bond prices rose when yields fell. However, most investors today weren’t around for the 28-years prior to 1981 when U.S. interest rates rose! Things were much different for bond managers then.

Do you know in which direction interest rates will travel during the next 1-, 3-, 5- or more years? We, at Ryan ALM, certainly don’t and we don’t need to know. Given that the greatest risk to an active core bond strategy is rates, why do you remain confident that your manager(s) will consistently meet or exceed the index’s return? With CFM, there is no guessing as to what rates will do. On the day that the CFM portfolio is created, asset cash flows of principal and interest are matched against the liability cash flows of benefits and expenses. As rates move (either up or down), that careful match remains, which is how we can claim that both security and certainty (barring a default) is achieved. Your core manager can’t make that claim because the Aggregate index looks nothing like your unique liabilities.

By the way, the “Agg” is up only 0.17% for the 5-years ending May 31, 2026. On a YTD basis, the index has produced a 0.38% return. Do you think that those results are helping or hurting your fund? As Clara asked 42-years ago (oh, my!), “where’s the beef?” I can tell you. It is found in a CFM strategy and it is a whopper!