By: Russ Kamp, CEO, Ryan ALM, Inc.

I recently attended a public pension conference in which the following question was asked by the moderator: Should public pension funds once again adopt a 60%/40% asset allocation framework? As a reminder, there may be an average exposure that results from a review of all public fund data, but there is NO such thing as an appropriate or standard asset allocation. Given that every defined benefit plan has its own unique liabilities, funded status/funded ratio, different workforces, ability to contribute, etc., how could there be a standard exposure to any asset class, let alone a standard 60% equity/40% fixed income allocation.

I’m sure that this question originates through the belief that the pension objective is to achieve a return on asset (ROA) assumption, as if there is some magic combination of assets and weightings that will enable the pension plan to achieve the return target. However, as regular readers of this blog know, we, at Ryan ALM, think that the primary objective when managing a DB pension plan is NOT a return objective but it is to SECURE the promised benefits at a reasonable cost and with prudent risk.

Pursuing a return objective guarantees volatility – volatility of returns, contributions, and funded status. It does not guarantee success! Regarding the volatility of returns, the annual standard deviation for a pension plan’s asset allocation is roughly 12%-15%. Refocusing on the plan’s unique liabilities secures, through cash flow matching (CFM), the monthly promises (benefit payments) from the first month out as far as the allocation will cover. Through this process the necessary liquidity is provided each month, while also providing the additional benefit of extending the investing horizon for the remainder of the assets that are no longer needed as a source of liquidity. We refer to these residual assets as the alpha or growth assets that now can grow unencumbered.

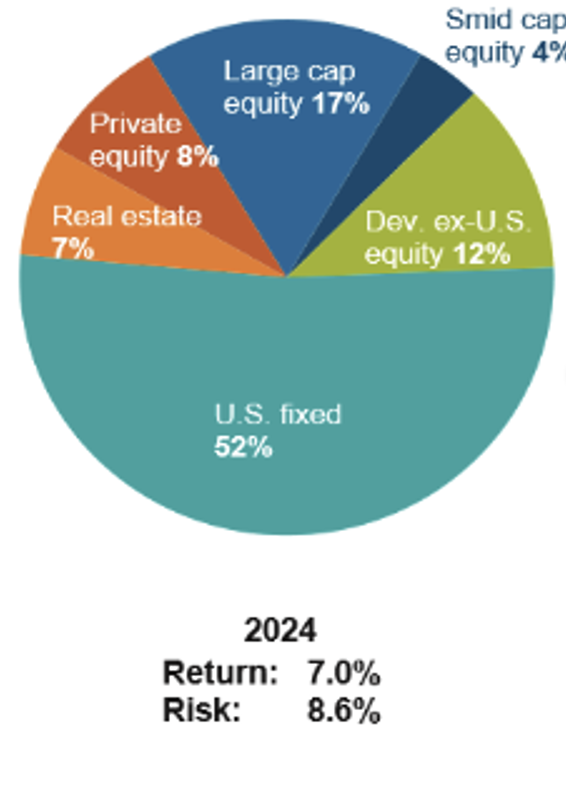

These growth assets can be invested almost anyway that you want. You can decide to just buy the S&P 500 index at low fees or construct a more intricate asset allocation with exposures and weightings of your choice. Again, there is no one size fits all solution. We do suggest that the better the funded ratio/status of your plan, the greater the allocation to the CFM strategy. If your plan is less well funded today, start with a more modest CFM allocation, and expand it as funding levels improve. In any case, you are bringing an element of certainty to what has been historically a very uncertain process.

So, please remember that every DB plan is unique. Don’t let anyone tell you that your fund needs to have X% in asset class A or Y% in asset class B. Securing the benefits should be the most important decision. How you build the alpha portfolio will be a function of so many other factors related specifically to your plan and its governance.