By: Russ Kamp, CEO, Ryan ALM, Inc.

U.S. fixed income benefitted tremendously from the nearly 4-decade decline in interest rates. From 1981 through 2021, the U.S. enjoyed a significant collapse in bond yields helping to fuel an unprecedented rally in risk assets. However, as Bob Dylan said, “the times they are a changin”!

The U.S. Federal Reserve’s FOMC announced on March 16, 2022, that the new Fed Fund’s target would be 0.25%-0.5% beginning on St. Patrick’s day 2022. This action marked the beginning of a rate regime change resulting from Covid-19 implications, including abundant stimulus creating massive demand for goods and services that couldn’t be met as production/manufacturing activities were disrupted.

The U.S. Fed Fund’s rate would eventually rise to 5.25%-5.50% in July 2023 (following 11 rate increases). Today, the Fed Fund’s rate stands at 3.5%-3.75%. For context, the average Fed Fund’s rate since 1971 is 5.39%, which includes a peak of nearly 20% in December 1980, and ultimately 0% in December 2008, in reaction to the GFC. It would once again hit 0% during Covid.

As a result, bond investors, such as pension plans, have ridden a rollercoaster of performance. Performance looked terrific for much of the nearly 40-year bull market but has been challenging since the Fed’s initial action in 2022. In fact, the Aggregate Index (Lehman, Barclays, Bloomberg, etc.) has produced only a 3.3% return for 20-years through March 2026. It is worse if you look at shorter timeframes, as the Index was up only 1.7% for 10-years, 0.3% for 5-years, and -0.1% YTD (all through March 31, 2026).

For pension plan sponsors and their advisors who are reluctant to utilize cash flow matching (CFM) as it might harm the pension plan’s ability to achieve the ROA, those performance #s above should be a wake-up call! As a reminder, the YTM of a CFM portfolio is a good proxy for what the fund will achieve for the period that liabilities are defeased. Given that Ryan ALM, Inc. is currently generating a YTM of 5.02% for a client with a 30-year defeasement and a 4.6% YTM for another with a 10-year CFM mandate, which result do you think is more harmful to the pension plan?

Furthermore, the CFM portfolio’s return is not predicated on the direction of interest rates, as it very much is with active core fixed income strategies. Importantly, CFM provides all the liquidity needed to meet the monthly benefit payments without having to sell assets, perhaps at inappropriate times. By cash flow matching bond principal and interest income with the plan’s liability cash flows (benefits and expenses), CFM secures the pension promises and reduces the FV cost (with certainty) of those obligations in the process. For the client with the 30-year CFM mandate, we are reducing future funding costs by -31.1% and for the 10-year CFM program, we have reduced funding cost by -28.0%.

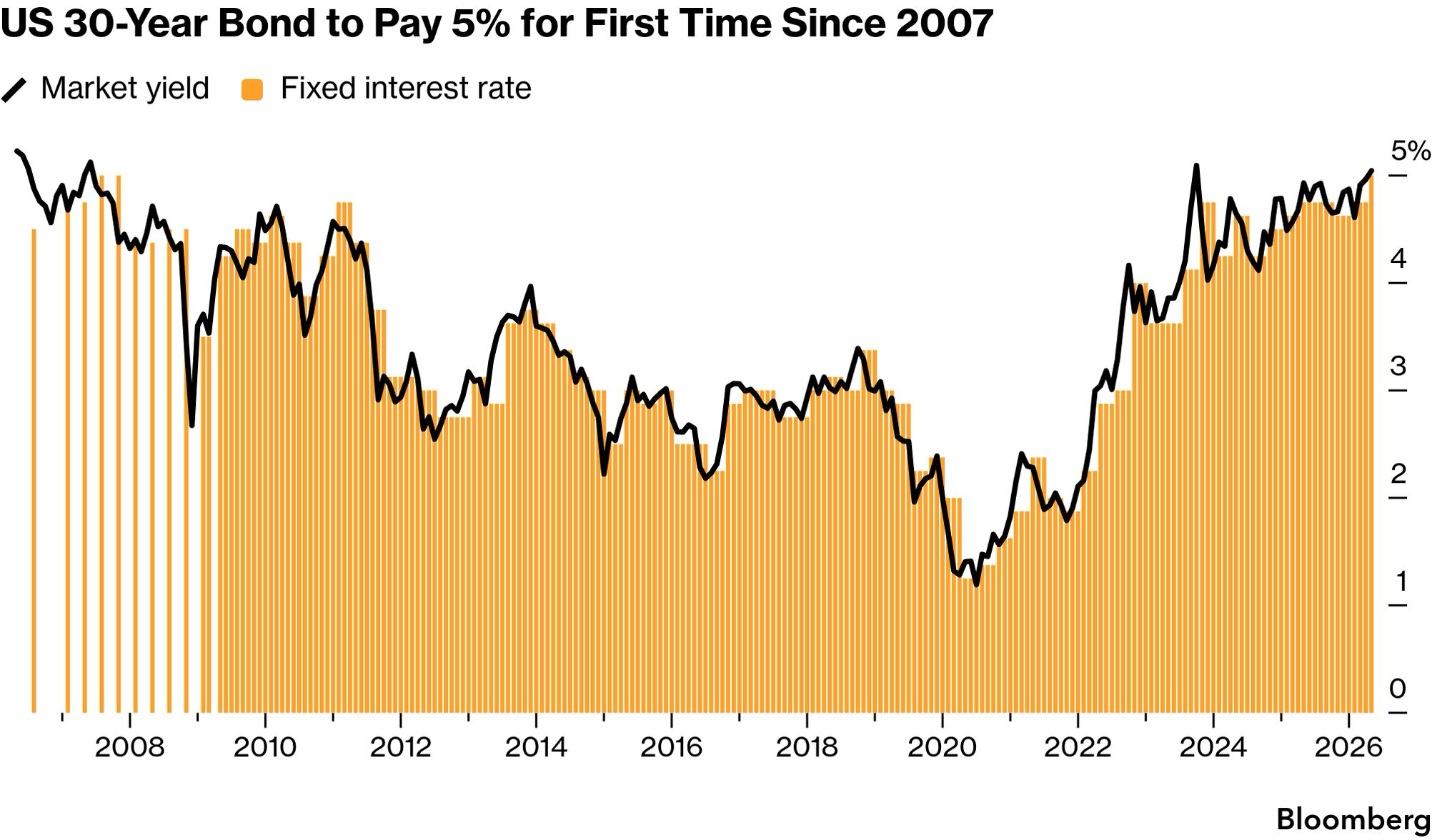

Where are we today? After a brief respite, U.S interest rates are once again trending higher, as greater inflation takes hold. Who knows where inflation and interest rates will eventually land, but a pension plan (or E&F) could benefit tremendously in this environment by engaging Ryan ALM, Inc. and our CFM capability. The 30-year Treasury bond yield history below highlights the rising rate environment. As a reminder, Ryan ALM builds CFM portfolios using investment-grade corporate that have yields substantially higher than comparable Treasury maturities.

So, I ask: Why sit with active fixed income and subject your plan’s bond allocation to the whims of an unknown interest rate environment when you can SECURE the pension promise with near certainty (absent any defaults)? Wouldn’t it be wonderful to know that your liquidity needs are all set for some prescribed period? Wouldn’t your plan participants want to know that the promises given have been secured? Now is the time to bring an element of certainty to the management of pension assets that doesn’t currently exist. Given the geopolitical uncertainty and the potential impact on inflation, rates, and other markets, creating funding certainty should be priority #1. Why isn’t it?