By: Russ Kamp, CEO, Ryan ALM, Inc.

Another Monday, another ARPA update. If this legislation wasn’t so important to so many American workers promised a benefit that had a very uncertain future, you’d probably say “enough already”. But we know that DB pension benefits provide retirees with some certainty and contribute to a more dignified retirement.

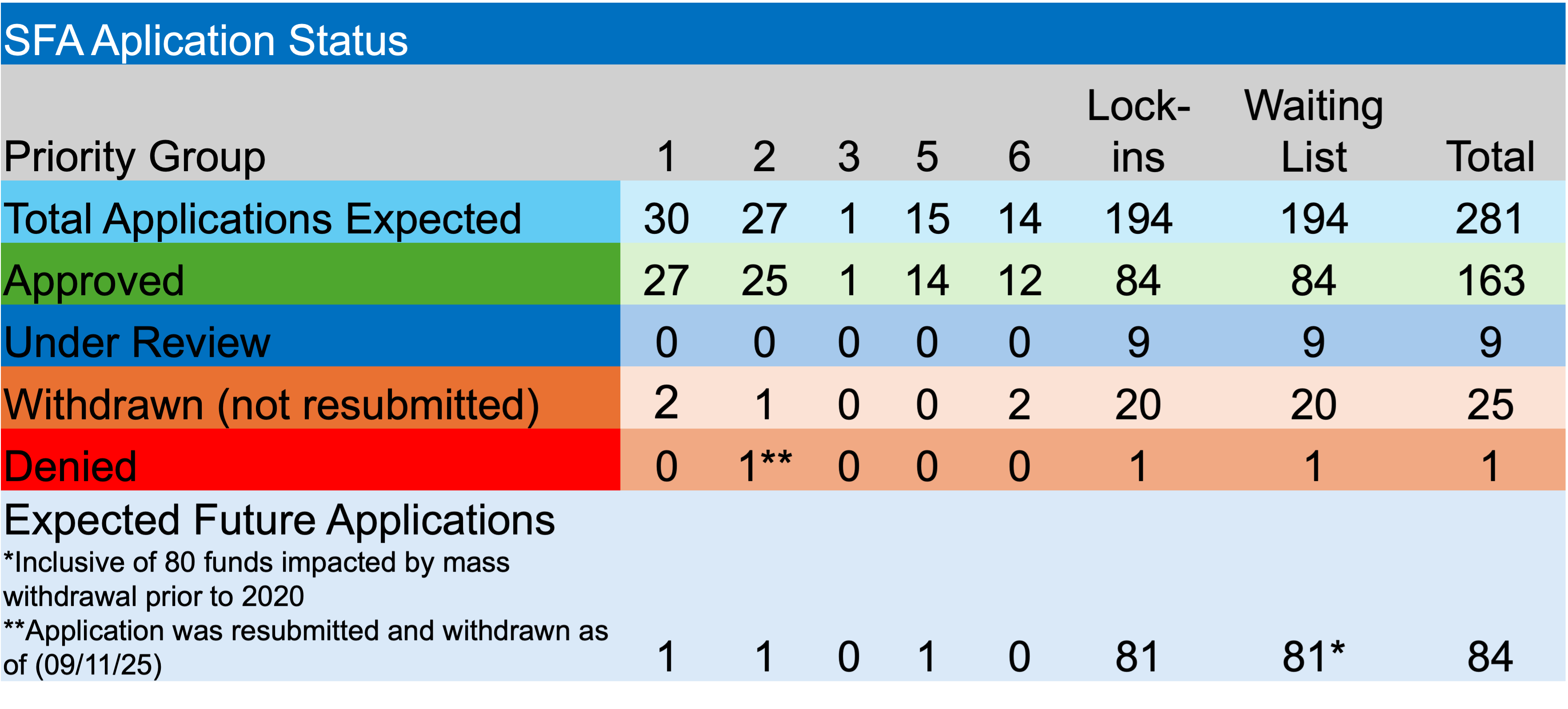

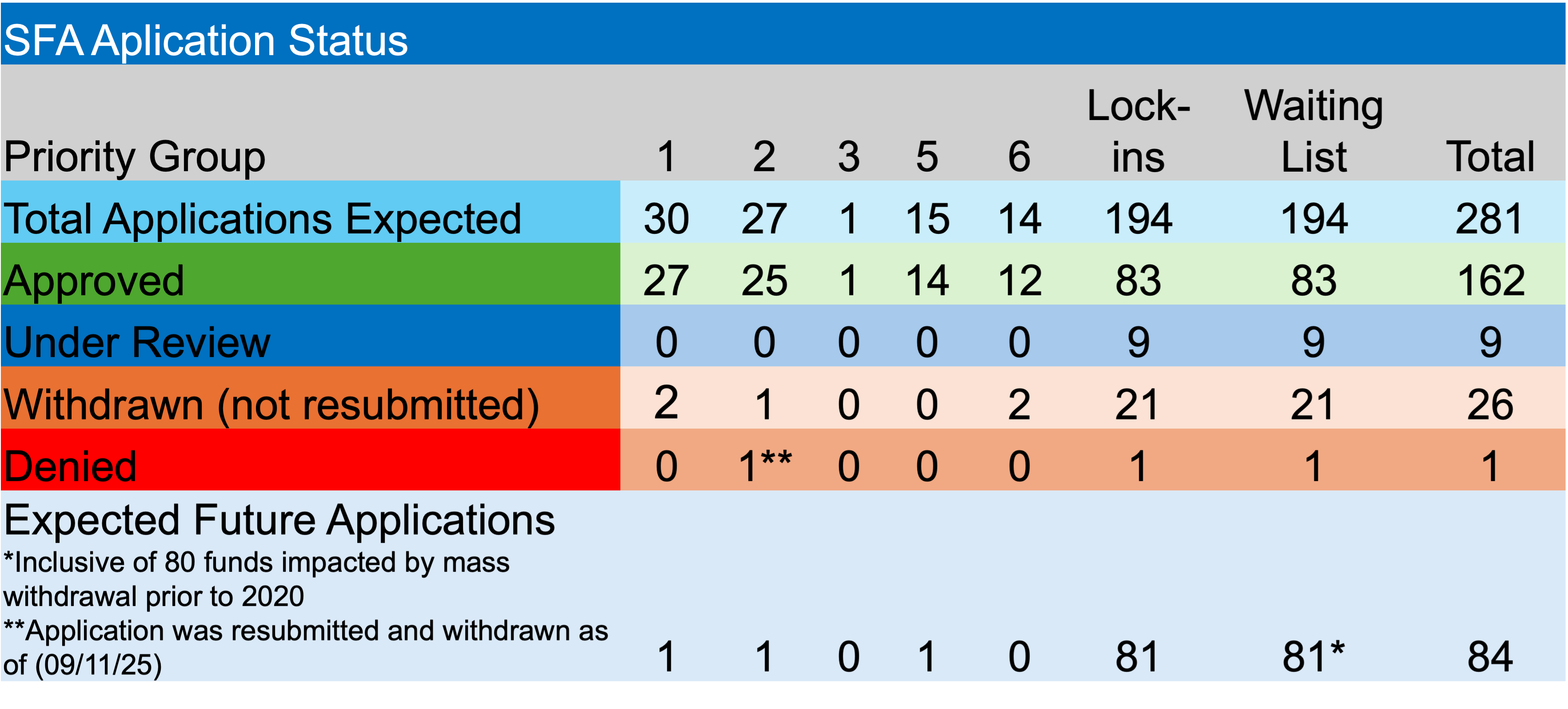

The ARPA legislation, and the PBGC’s implementation of this critical program, is less than 6-months from its completion. As a result, weekly activity is waning. The previous highlights this trend, as only 1 pension fund received approval of its SFA application. Iron Workers-Laborers Pension Plan of Cumberland, Maryland, will receive $22.7 million for the plan’s 754 participants, as this non-priority group member received approval for its revised SFA application on July 8th.

There was no other apparent activity during the previous week, as no applications were received, denied, or withdrawn. The waitlist still has one non-Mass Withdrawal fund that has yet to submit an application to the PBGC.

There are currently eight applications before the PBGC. Roofers and Slaters Local No. 248 Pension Plan’s application must be acted on by July 18th by the PBGC, or they will automatically receive an SFA grant, currently estimated at $5.1 million.

For pension plans still waiting to receive SFA or for those that have recently received their grant, U.S. rates continue to be near cycle highs, providing pension sponsors with the opportunity to secure those future benefits with greater cost reduction.

Lastly, the PBGC continues to codify its rules regarding permissible investments for the SFA proceeds, which seems surprising given that we are 5-years into the program and their oversight. Ron Ryan and I will provide our thoughts on the latest proposed changes in a separate post.