By: Russ Kamp, CEO, Ryan ALM, Inc.

Milliman has once again released its monthly Milliman 100 Pension Funding Index (PFI), which analyzes the 100 largest U.S. corporate pension plans. It would be fascinating to see how these 100 plans differ from a list just 20-years ago.

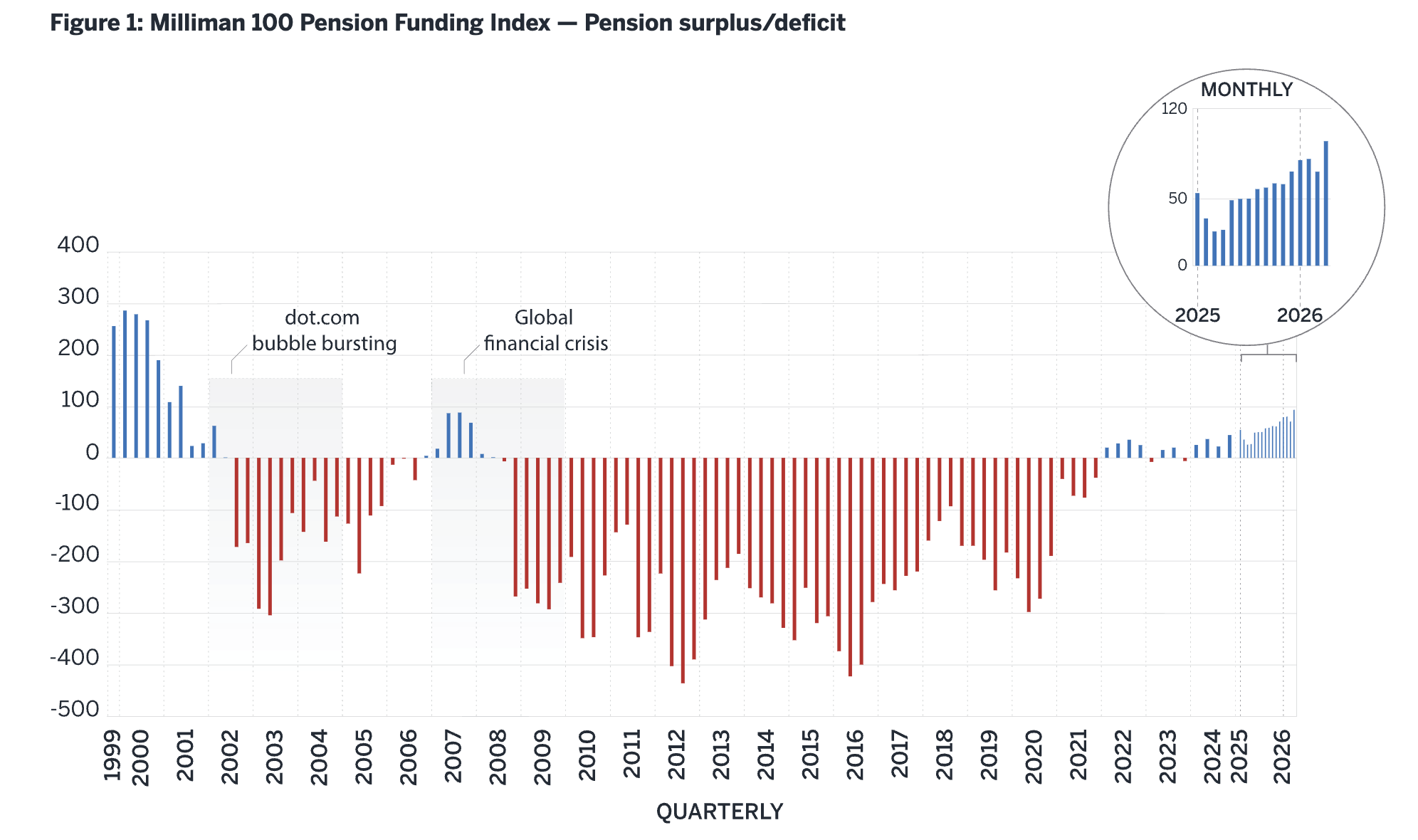

As for today’s members, the Milliman 100 PFI plans showed improved funding by $23 billion during April. These stellar results were driven by strong equity returns as the constituents averaged a 2.13% gain. As a result, the funded ratio dramatically improved from 105.9% at the end of March to 107.8% at the end of April representing the highest level of funding since October 2007, when it stood at 108.1%. Strong investment gains increased assets by $20 billion and now stand at $1.297 trillion, while the projected benefit obligation fell slightly to $1.204 trillion, as the monthly discount rate edged up one basis point, to 5.66% from 5.65%.

“After a flat first quarter, the funding surplus grew to $94 billion at the end of April, primarily due to strong market returns,” said Zorast Wadia, author of the Milliman 100 PFI. “This means plan sponsors continue to have more pension risk management options as plans move further into surplus territory.”

Plan sponsors would be wise to seek risk reducing strategies. The previous high watermark was achieved in October 2007, just prior to the start of the Great Financial Crisis, which pummeled markets through March of 2009. As the graph below highlights, the Milliman 100 went from a small surplus in the Q3’07 to a major deficit within 6 months. It would be another 13-years before a surplus was once again created.

Plan sponsors should secure the pension promises through a cash flow matching (CFM) strategy and then actively manage surplus assets since they’ve now created a much longer investing horizon for those assets. Ryan ALM, Inc. is always willing to provide a free analysis of what is possible through CFM.

For the full Milliman report, click on the link below.