By: Russ Kamp, CEO, Ryan ALM, Inc.

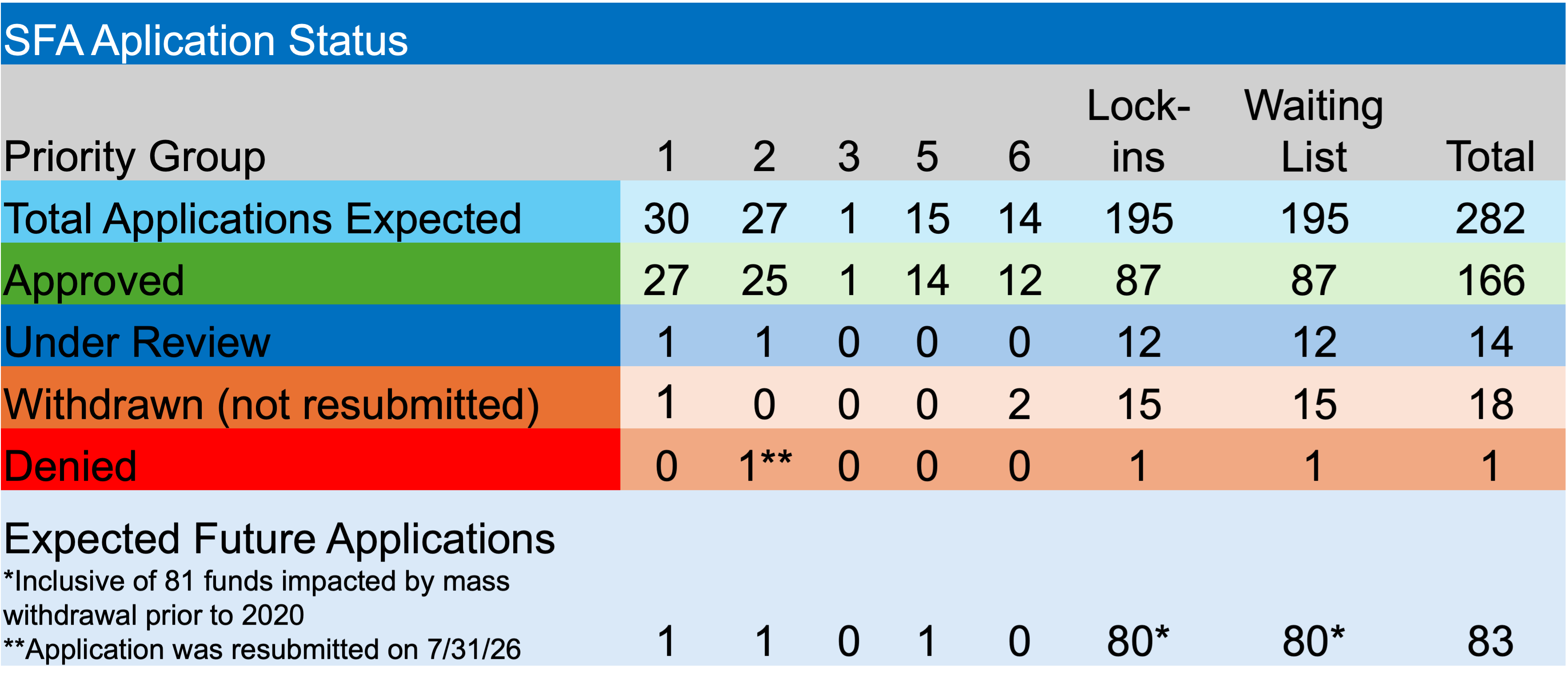

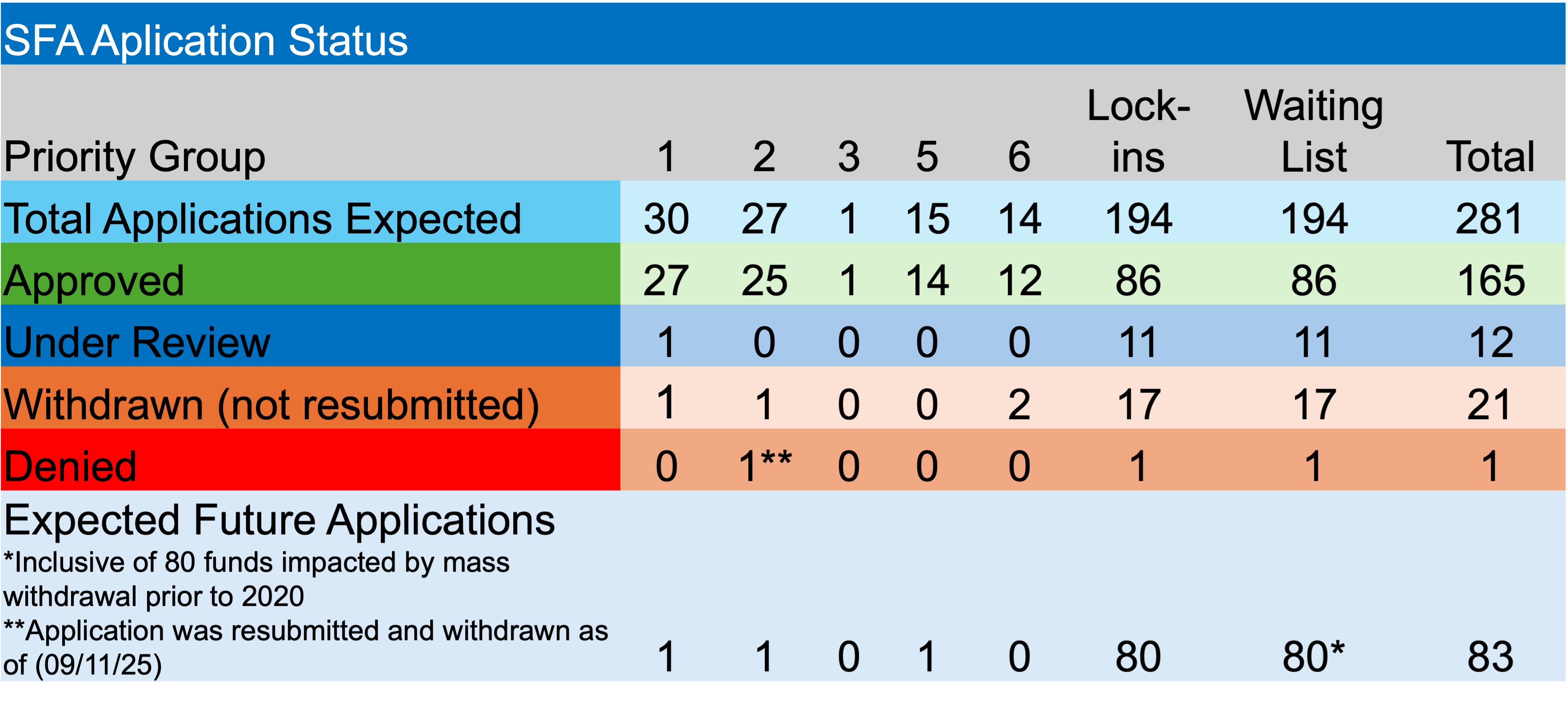

As regular readers of this blog know, I report weekly on the PBGC’s effort to implement the ARPA pension legislation. In those frequent updates I’ve reported that there are currently 81 pension funds that were placed on the waiting list and described as having been impacted by mass withdrawal prior to 2020. One of those pension funds, Retirement Plan of Local 1102 Retirement Fund is the first SFA candidate invited to submit an application. I’ve asked, is this a unique situation or are the others likely to follow?

After much reading on the subject, Local 1102 is unique as the first plan from the pre-2020 mass-withdrawal group to be invited to submit a full SFA application, but I believe that it won’t be the last. The critical development behind Local 1102’s advancement to being under review, is the litigation involving Bakery Drivers Local 550 and the Supreme Court’s May 18, 2026, decision not to review the Second Circuit ruling from April 2025.

The PBGC’s original position related to the “mass withdrawal” plans was clear: “a multiemployer plan that terminated by mass withdrawal before the 2020 plan year generally could not qualify for SFA because the funding-status rules used to establish “critical and declining” status no longer applied after termination.” The PBGC made its position quite clear in its 2022 final rules.

However, that interpretation was challenged by the Bakery Drivers Local 550 and Industry Pension Fund after initially being denied the opportunity to submit its application in January 2023. The Second Circuit ruled against PBGC in April 2025. The case involved a plan that terminated by mass withdrawal in 2016 but subsequently resumed activity and asserted that it was again in critical-and-declining status. The Second Circuit concluded that PBGC’s treatment of the prior termination was wrong.

Not surprisingly, the PBGC then asked the Supreme Court to hear the case. On May 18, 2026, the Supreme Court denied “certiorari*”, leaving the Second Circuit decision standing. That timing is significant when viewed alongside what happened next. As I mentioned in my July 24 ARPA update, the PBGC invited the Retirement Plan of Local 1102 Retirement Fund to submit an application, which I mentioned was the first of the 81 plans on the waiting list categorized as “Plan Terminated by Mass Withdrawal before 2020 Plan Year” to be invited to submit a grant application.

This may not be the opening of the flood gates, as I asked in that same blog post. The Local 550 decision does not necessarily mean that every plan terminated by mass withdrawal before 2020 is now eligible, as there can still be plan-specific questions about whether a multiemployer pension fund satisfies one of ARPA’s statutory eligibility tests. For instance, the Local 550 litigation involved the additional claim that the fund claimed it had effectively been “restored” after its 2016 termination.

Given that reality, the PBGC still has room to evaluate each applicant’s particular situation. That said, the PBGC’s says it will provide every eligible plan an opportunity to file, subject to its ability to process applications within the statutory 120-day review period. When capacity opens, the PBGC contacts plans at the top of the waiting list and permits them to file.

The pace of grant application submissions could still be slow because PBGC meters applications based upon its capacity to complete the 120-day review. As mentioned in my weekly update as of August 7, 2026, there are currently 14 pension funds under “review”. I would be very surprised if Local 1102 proved to be the only one of the 81 plans invited to apply.

I don’t know how much these additional plans may ultimately receive, but I do know that many American workers will now receive the benefits that they were initially promised. That is only fair.

* If a court denies Certiorari, it usually does not mean it agrees with the lower court’s ruling, it simply declines to review the case.