By: Russ Kamp, CEO, Ryan ALM, Inc.

I’m sure that folks were very (perhaps bitterly) disappointed not to get my weekly update yesterday on the PBGC’s implementation of the ARPA pension legislation. I was traveling for business yesterday, but unlike many travelers, my experience at Newark Airport was shockingly positive. I have heard of 4-6 hour waits to get through security and planes that are forced to leave the gate with as few as 5 passengers. Various estimates put the daily impact of these disruptions at $285 million to $580 million once a 10% reduction in flights occurs.

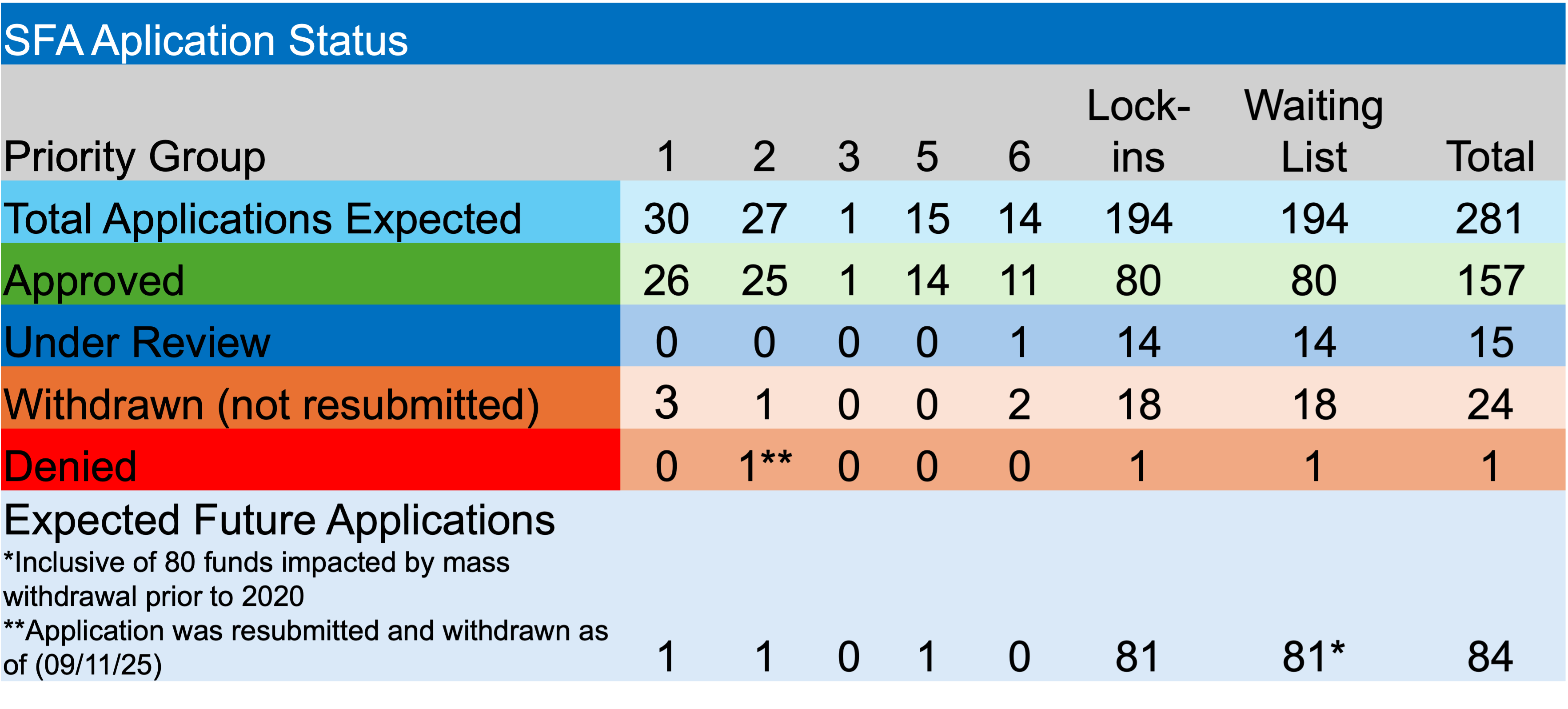

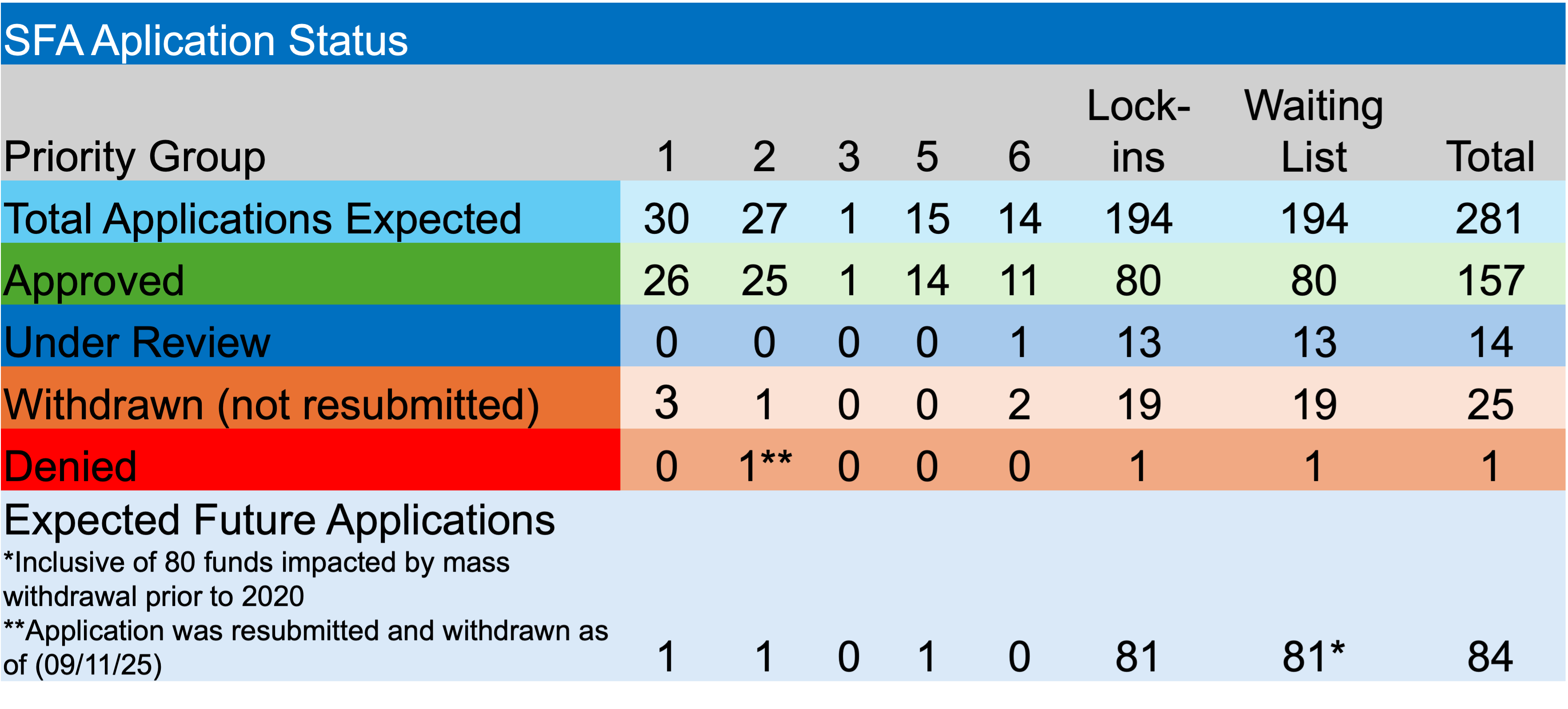

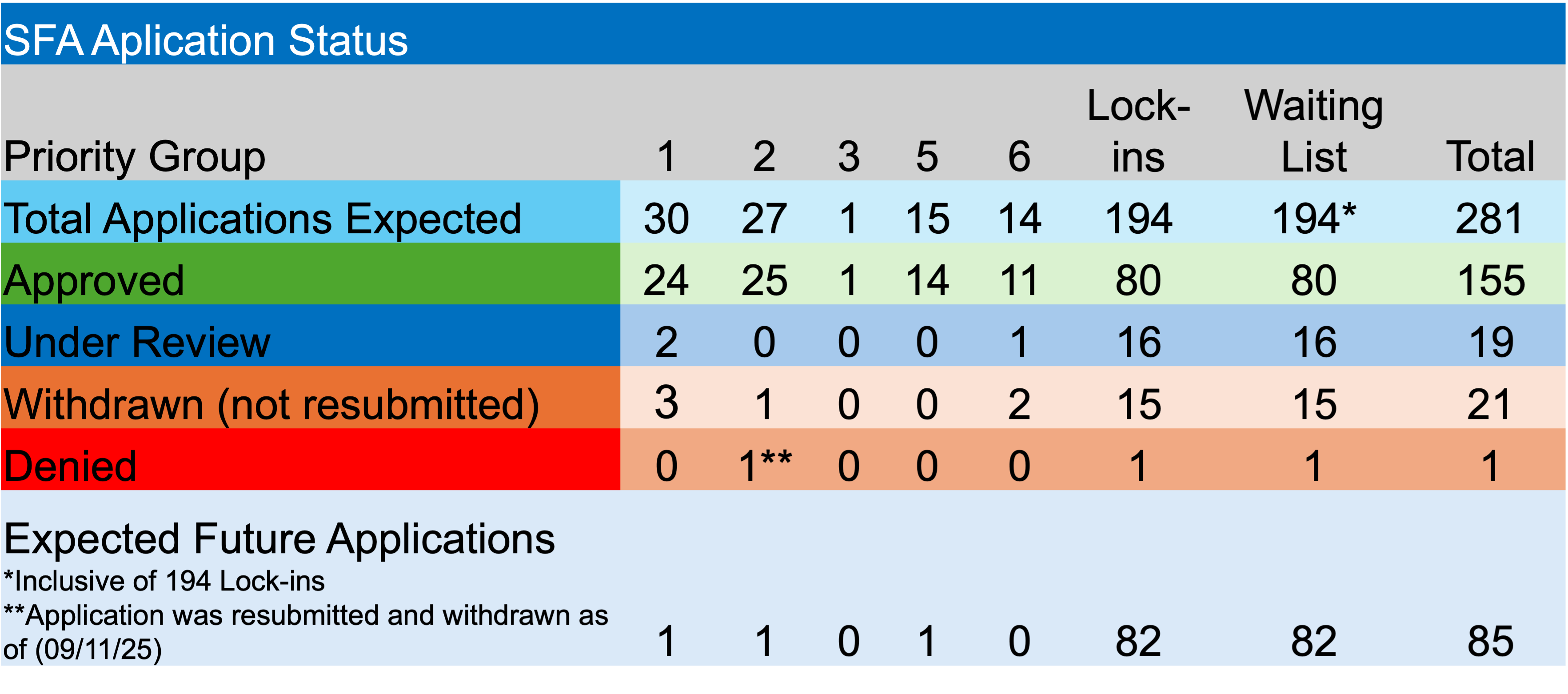

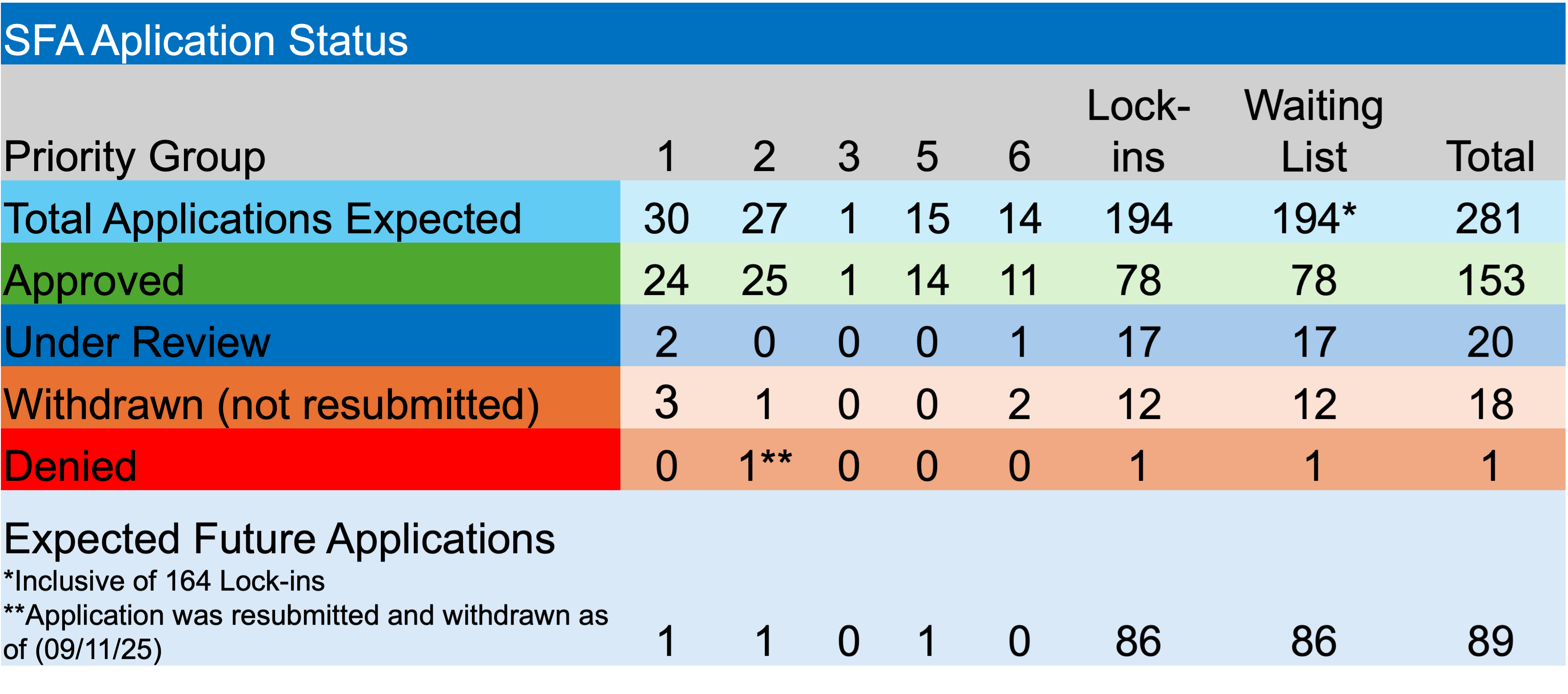

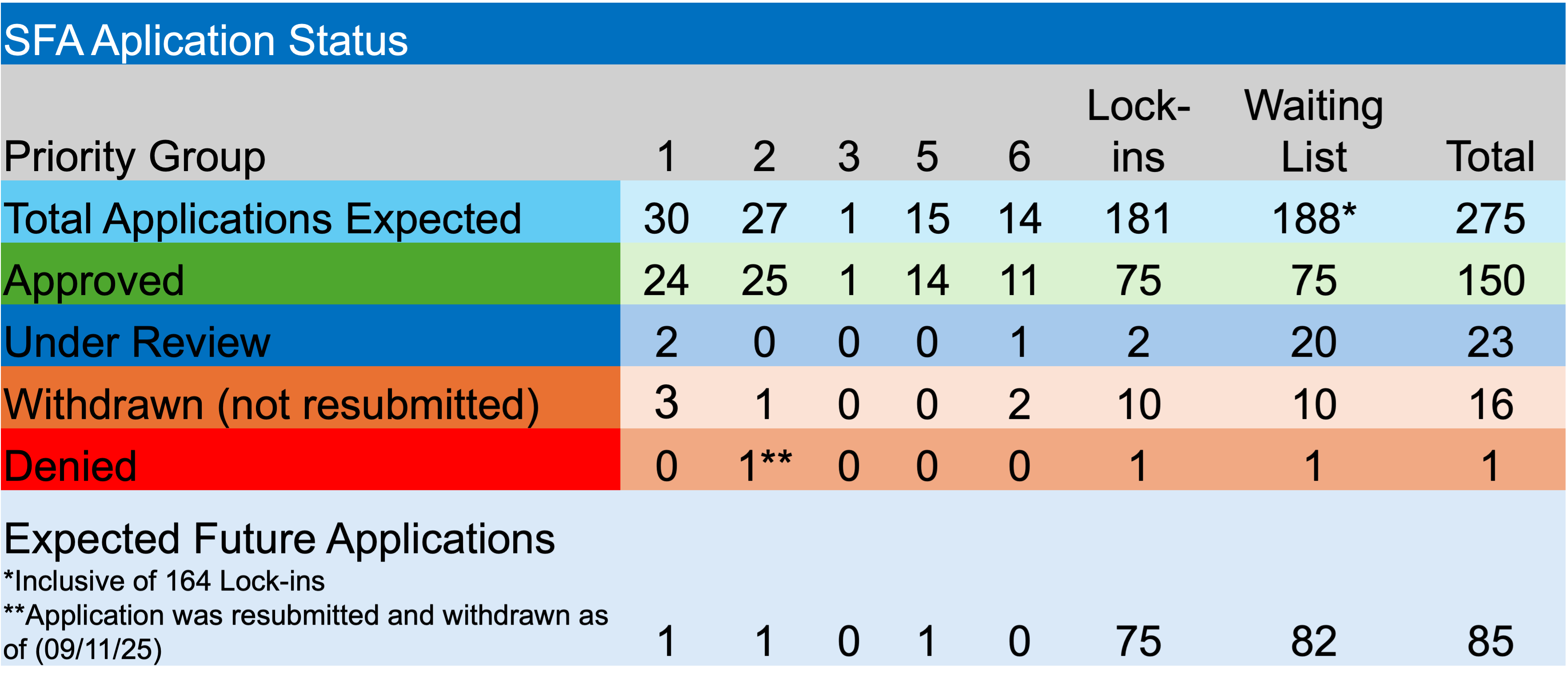

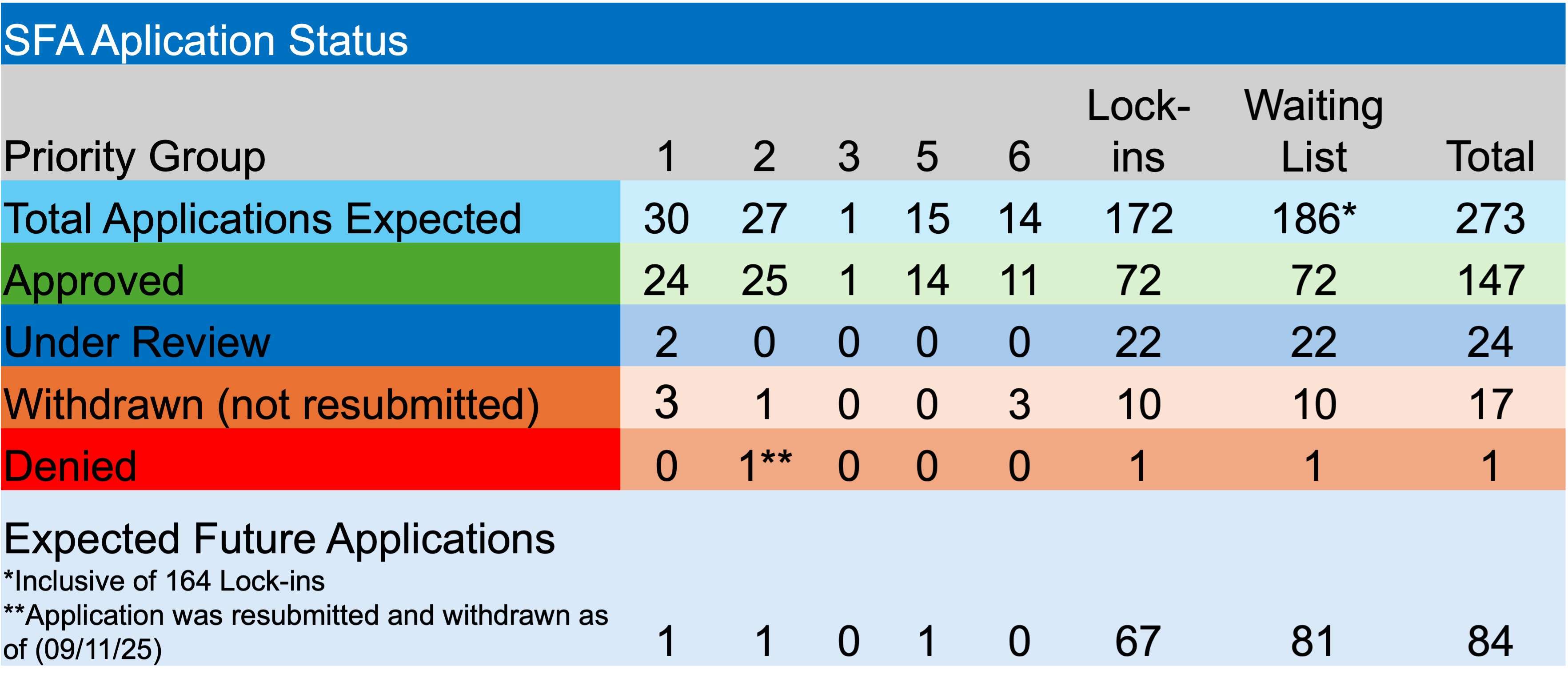

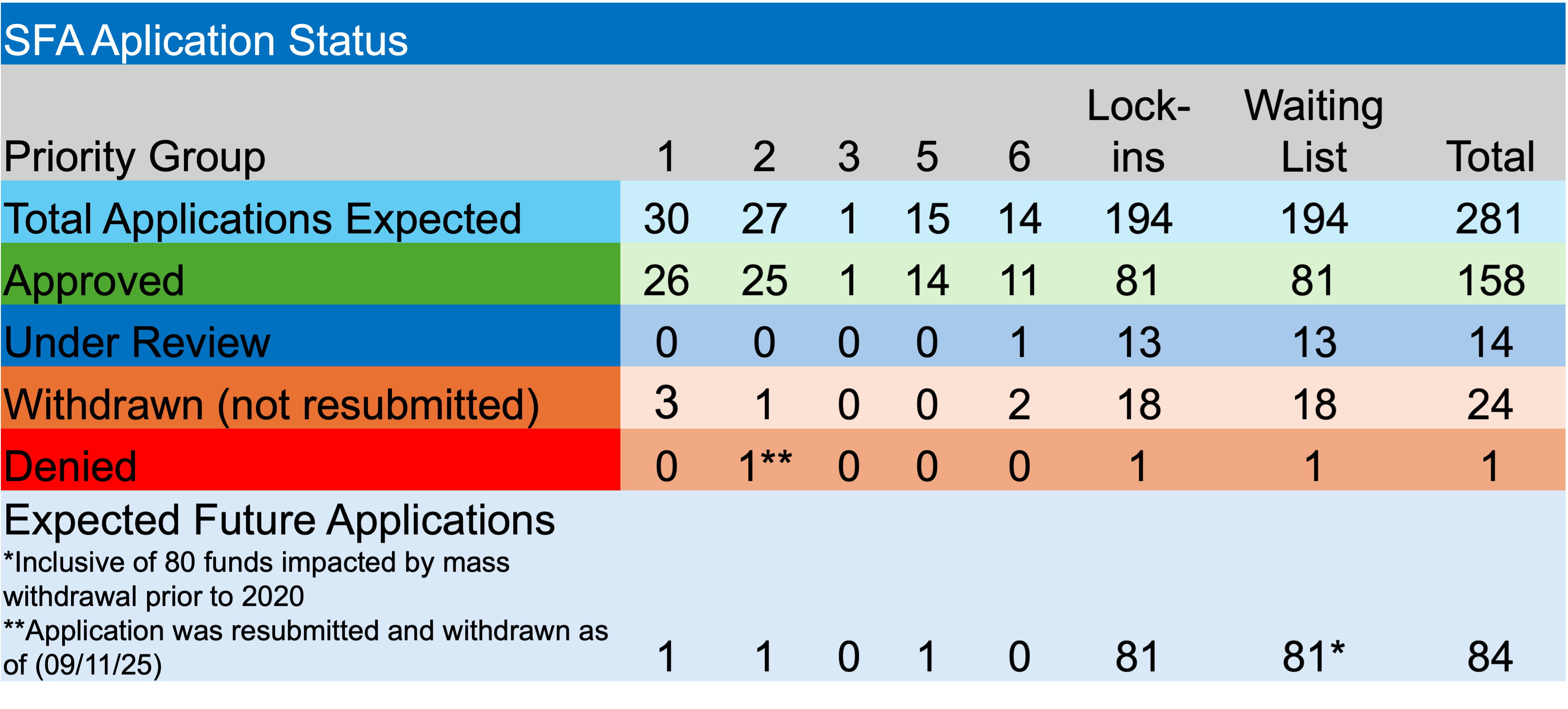

What about ARPA? As regular readers know, the PBGC has worked through a significant majority of non-mass withdrawal applicants. There remains just one fund – Plasterers Local 79 Pension Plan – that hasn’t gotten to submit an initial application form those on the waitlist. There are still a few pension funds from the original Priority Groups that haven’t filed an initial application seeking SFA.

During the prior week, Cumberland, Maryland Teamsters Construction and Miscellaneous Pension Plan received approval of its revised SFA application. They will receive $9.5 million for their 101 plan members. Congrats!

In other news, there is no other news, as there were no new applications submitted, as the PBGC’s eFiling portal remains temporarily closed. Also, there were no applicants denied, no plans were asked to repay a portion of the SFA, and no applications were withdrawn or added to the waitlist.

The treatment of the 80 plans (from potentially 131) currently on the waitlist that fall under the category of plans suffering mass withdrawal prior to 2020 is the last remaining significant issue that the PBGC must still work through.

U.S. Treasury yields have risen sharply since the beginning of the Iran conflict. As challenging as that development is on existing bond funds, the entry point for SFA recipients wanting to use CFM to secure the benefits and expenses is as good as it has been in more than 1-year. As a reminder, higher yields reduce the cost of those future promises.