By: Russ Kamp, CEO, Ryan ALM, Inc.

Jack Webb, who portrayed Joe Friday in the 1950s crime drama “Dragnet”, was famous for saying in season two “all we want are the facts, ma’am.” The catchphrase eventually morphed into a shorter phrase with the help of comedian, Stan Freberg, who released his parody “St. George and the Dragonet” in which he stated, “just the facts, Ma’am”. That phrase has been carried forward in Dragnet remakes. But, I digress.

Today, I present to you a Joe Friday moment. Here are the facts: Oil prices have risen by 27% since July 6th. U.S. Treasury yields are rising across the yield curve, and the 30-year Treasury yield is within 6 bps of this cycle’s high of 5.2%. The 10-year Treasury yield is currently 4.66% as of 10:24 am on 7/22/26. Investment grade corporate bond spreads have finally started to widen although slowly. According to Morgan Stanley, the “average” yield on a BBB+ corporate is 6.23% or roughly 1.1% higher than the yield on the comparable 30-year Treasury bond. Inflation, which moderated in June, is likely to spike higher given the current direction of activity in the Middle East and its impact on shipping lanes.

These are the facts. They suggest to me, and hopefully you, that the current U.S. interest rate environment is ripe for de-risking activities through cash flow matching (CFM). Why continue to live with the uncertainty surrounding oil, inflation, rates, etc., when you can SECURE your fund’s promises in the near-term?

I wish that I had a crystal ball to help me forecast the future but alas I don’t, and I suspect that you don’t either. Given the lack of clarity related to future events, I suggest that we live in the moment. We have an environment in which the cost of those future promises (benefit payments) can be cut dramatically. An environment that brings an element of certainty to a very uncertain process. An environment in which U.S. interest rates are providing plan sponsors with a significant portion of the annual return on investment target.

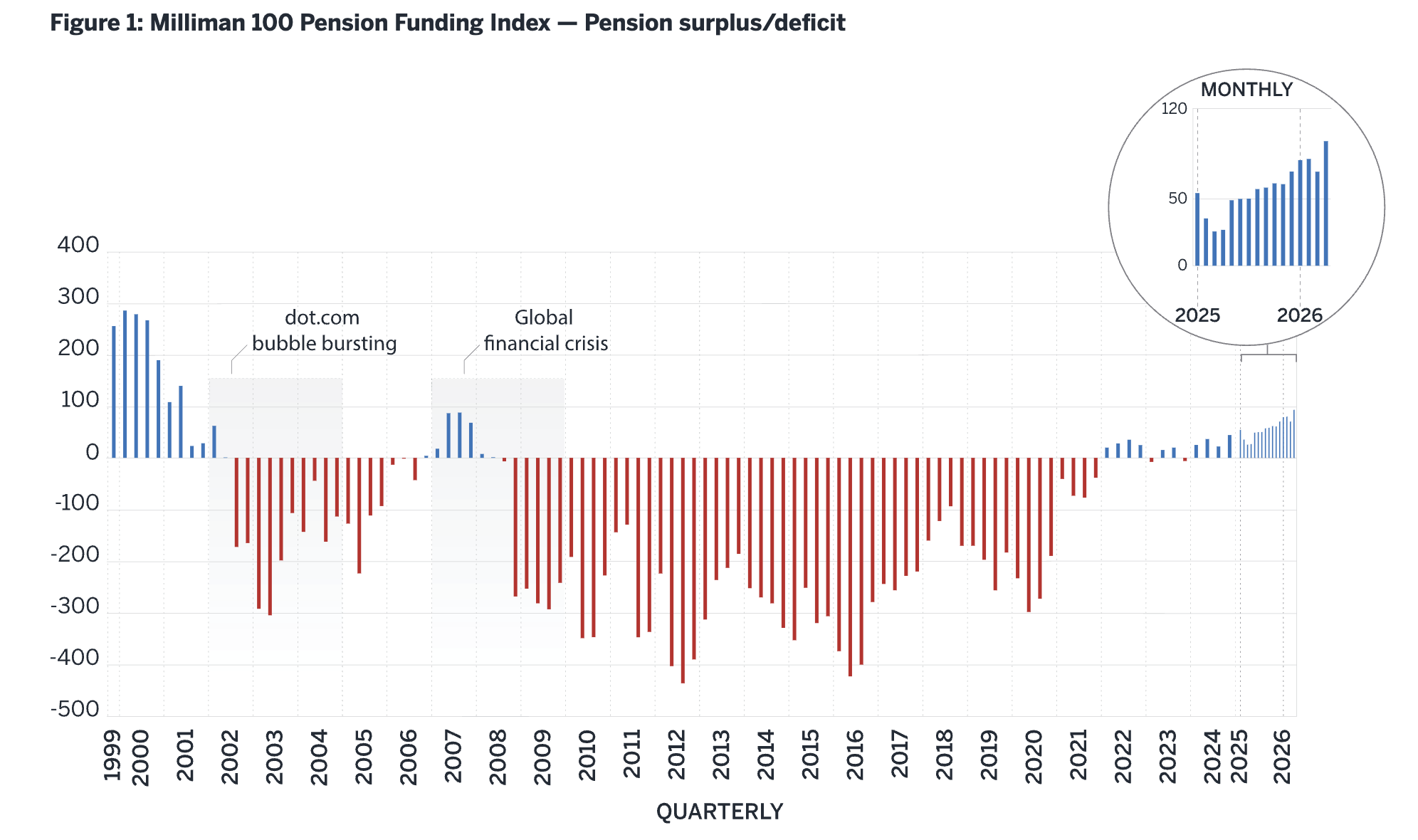

We’ve seen this scenario before. At the start of the 2000s, we had pension plans extremely well-funded and contribution expenses well-controlled. That opportunity went unheeded. The result of that inaction proved to be disastrous as we saw DB pension funding get pounded by two major equity market corrections. Are you confident that another major correction isn’t around the corner?

Like Joe Friday, I rely on the facts, which I’ve now presented to you. Ignore them at your peril.