By: Russ Kamp, CEO, Ryan ALM, Inc.

Equity markets are partying like it’s 1999! Valuations be damned! Are the improved funded ratios for defined benefit plans going to be secured through de-risking strategies or are they going to once again be subjected to the whims of the capital markets? For plan sponsors benchmarking your equity exposure to the S&P 500, are you prepared for the volatility potentially associated with the great technology concentration (now roughly 50% of the index)? For those invested in the Nasdaq indexes, are you prepared for SpaceX’s impact, which should happen soon?

Come on, folks. Let’s not repeat the mistakes of the past. Higher interest rates, higher inflation, crazy equity valuations, and geopolitical uncertainty have not seemed to tamp enthusiasm for U.S. stocks. What will? Will it take a stock like SpaceX – now valued at $2.75 trillion – to be the reason that stocks fall back to earth? SpaceX has been trading for three days. The action on the stock suggests that it is just another meme stock.

Can you believe that SpaceX has overtaken Amazon as America’s fifth-largest company? A closer examination of the fundamentals shows just how irrational our markets/investors have become. Let’s look at the current fundamentals of Amazon versus SpaceX.

Valuation

| Metric | SpaceX | Amazon |

|---|---|---|

| Revenue | $19.30B TTM | $716.9B in 2025 |

| Earnings | -$9.36B TTM | $77.7B net income in 2025 |

| P/S | 137.7x | about 3.5x |

| P/E | -284.2x | about 34x normalized |

SpaceX’s valuation is being priced as an extraordinarily high-growth story, despite being a money-losing company, which is why its P/S is dramatically higher than Amazon’s. Amazon, by contrast, already has large-scale revenue and meaningful profitability, so its valuation looks much more grounded in current fundamentals, despite it carrying a rich valuation at 34x normalized earnings.

Profitability

Amazon is clearly ahead on earnings quality: it generated $80.0B of operating income and $77.7B of net income in 2025. SpaceX, on the other hand, reported a $9.36B trailing-twelve-month loss and a negative net margin.

Growth profile

Clearly, SpaceX’s case is mostly about future optionality: investors are paying for expected expansion in launch, satellite, and adjacent businesses rather than present-day profits. Amazon’s case is more balanced because it combines growth with profitability, especially from AWS and advertising, which support its margins.

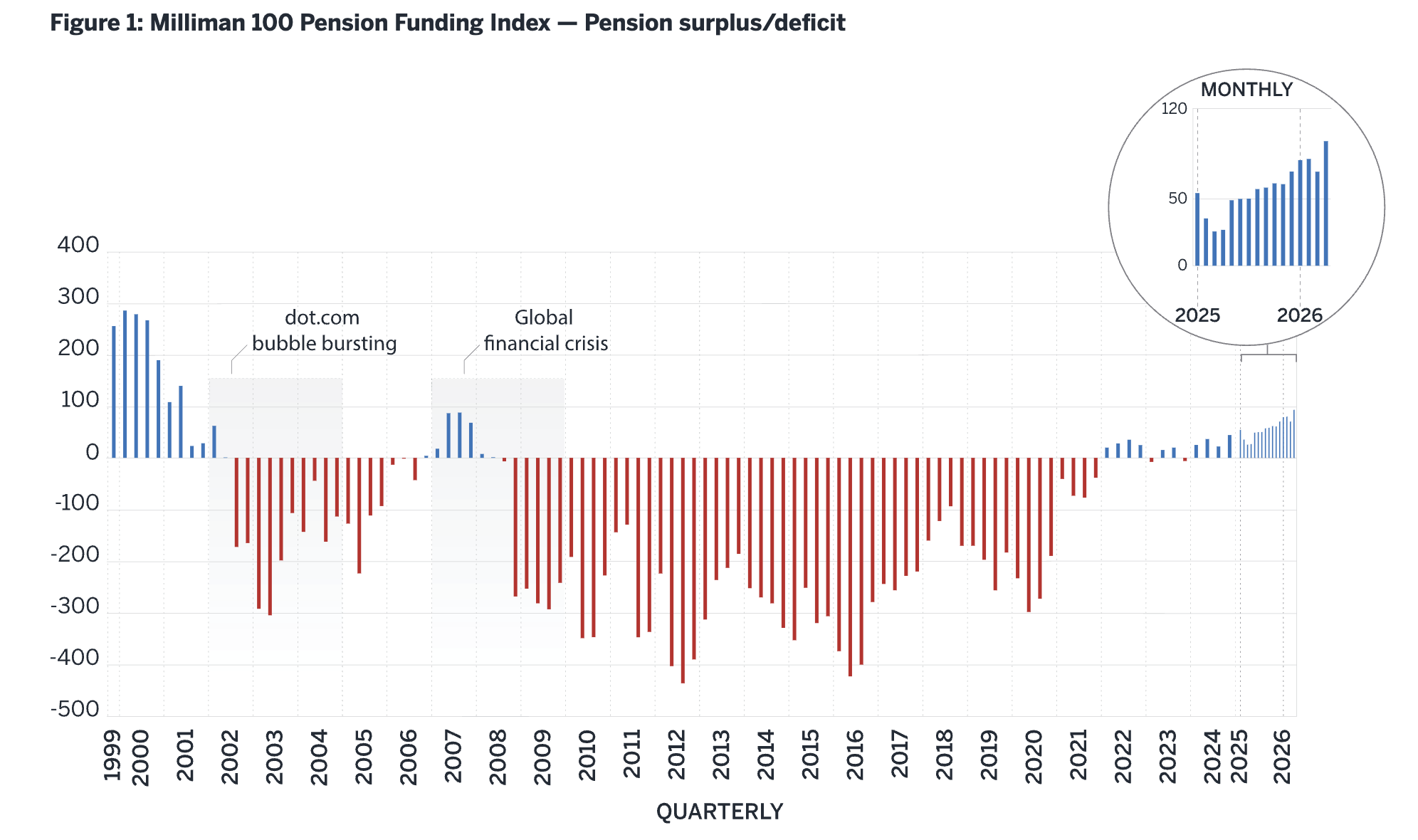

SpaceX will need to increase sales by roughly 37x to match Amazons P/S of 3.5x. Nothing grows to the heavens – even a rocket company. Risks to pension funding seem to be skewed to the downside. It is time to take some profits and secure the promises that have been given to your plan participants. Please don’t waste another golden opportunity to fortify your plan’s funding.