By: Russ Kamp, CEO, Ryan ALM, Inc.

I continue to be surprised that more pension plans don’t embrace greater certainty in the management of their funds. The Iran War is leading to great uncertainty related to inflation, interest rates, and economic growth. Yes, U.S. equities have enjoyed a healthy recovery following the initial outbreak in the Middle East, but is that sustainable?

Callan does a good job of providing a regular review of what asset allocation would be necessary to achieve a 7% return and the risk (measured as standard deviation) to achieve that return objective. Callan indicated that it was very easy to achieve a 7% return all the way back in 1994 when U.S. interest rates were higher than they are today. In fact, an allocation of 85% to fixed income and small allocations to L.C. equity, SC equity, and int’l stocks would have produced a 7% return with only a 5.6% annual standard deviation.

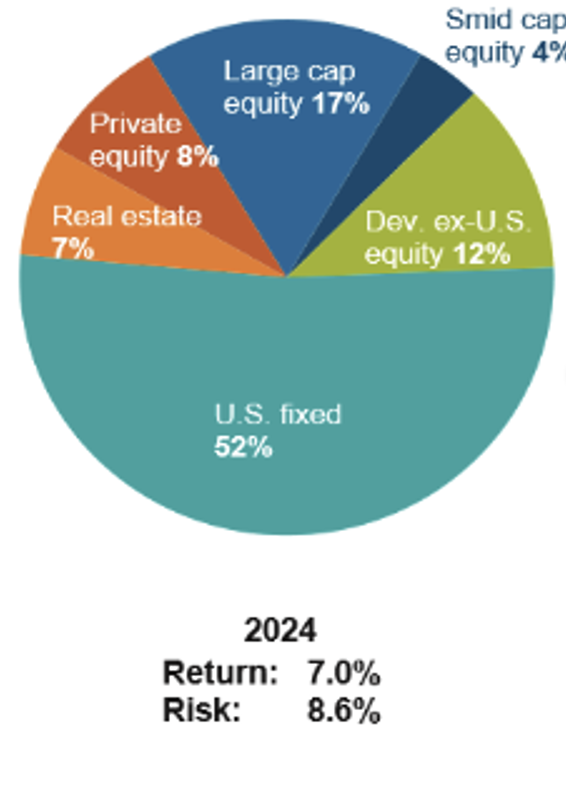

However, in the most recent update from 2024, Callan suggests the following asset allocation is necessary to achieve a 7% return:

This means that 68% of the time, a plan sponsor should expect an annual return of 7% +/- 8.6%. At two standard deviations (95% of the observations or 19/20 years), the annual return will fall between +/- 17.2% of the 7% target. Would you be comfortable knowing that your fund could generate an annual return of -10.2%? Think about the impact a return like that would have on contributions?

What if I said that cash flow matching (CFM) a portion of your pension fund would result in those assets having an annual SD of 0% barring a default which occurs at a rate of 0.18% annually among investment grade corporate bonds for the last 40-years. How’s that possible? When CFM is implemented, the plan’s asset cash flows and matched agains the plan’s liability cash flows (benefits and expenses). They mover in lockstep with each other no matter where rates go. Today’s U.S. interest environment is attractive and getting more attractive as I write this post, as the 30-year Treasury bond yield has topped 5% (5.02% at 11:47 am DST). Higher rates are great for CFM, as they lower the present value of those future promises.

Furthermore, the use of a CFM portfolio secures the pension promises, dramatically improves plan liquidity, eliminates interest rate risk for the portion of the plan, extends the investing horizon for the residual plan assets, and reduces the cost of those future pension promises. Again, why wouldn’t you embrace an element of certainty?

I’m not sure what the Callan team would identify as the proper allocation to achieve a 7% return today, but I suspect that the annual standard deviation is greater than the 8.6% from 2024. Every time a pension plan falls short of the annual ROA, contributions must increase to make up for the shortfall. Greater investment certainty, like that associated with using CFM, reduces the likelihood that the pension plan sponsor with suffer from a negative surprise associate from increased contributions.