By: Russ Kamp, CEO, Ryan ALM, Inc.

I occasionally receive emails from Glen Eagle. In their most recent “mailing”, they cited a Capital Group report that highlighted that Americans are living longer than many anticipate. They pointed out that a healthy 65-year-old married couple has a 50% chance that one spouse will reach 94-years-old and a 25% chance that one reaches 98. However, 52% of older Americans do not factor longevity into retirement planning. Geez, I wonder why?

Could it be that they’ve been asked to fund a “retirement” program through a 401(k) – like vehicle, if they were fortunate to work for a company that offered one in the first place. Could it be also that we’ve placed financial burdens on American workers through ever increasing expenditures related to housing, education, healthcare, childcare, utilities, transportation, food, etc? Despite the fact that defined contribution plans have been around for multiple decades, the median account (according to Vanguard) was only $38k (2024), while the median account for someone aged 55-64-years old was only $95.6k. Again, those are median balances for folks that have actually saved for retirement. There are millions of Americans that have not been able to set aside any assets for their “golden years”.

With balances in that range, I would guess that the average American worker is wondering how they’ll afford to get to 75-years-old let alone 95 or older. Unfortunately, most American workers do not have access to a defined benefit plan that would solve the issue of longevity, as the promised monthly benefit spans the participant’s entire life, and perhaps their spouses, too. I’ve never been in a DB plan, but my Dad was fortunate to be in one. He didn’t receive a large monthly payment, but he and my Mom could count on a check each month for the 34-years that he lived in retirement. There was no guessing as to when he would pass or how much he could safely take from a DC balance each month. That certainty was incredibly comforting to them, as it would be to any plan participant.

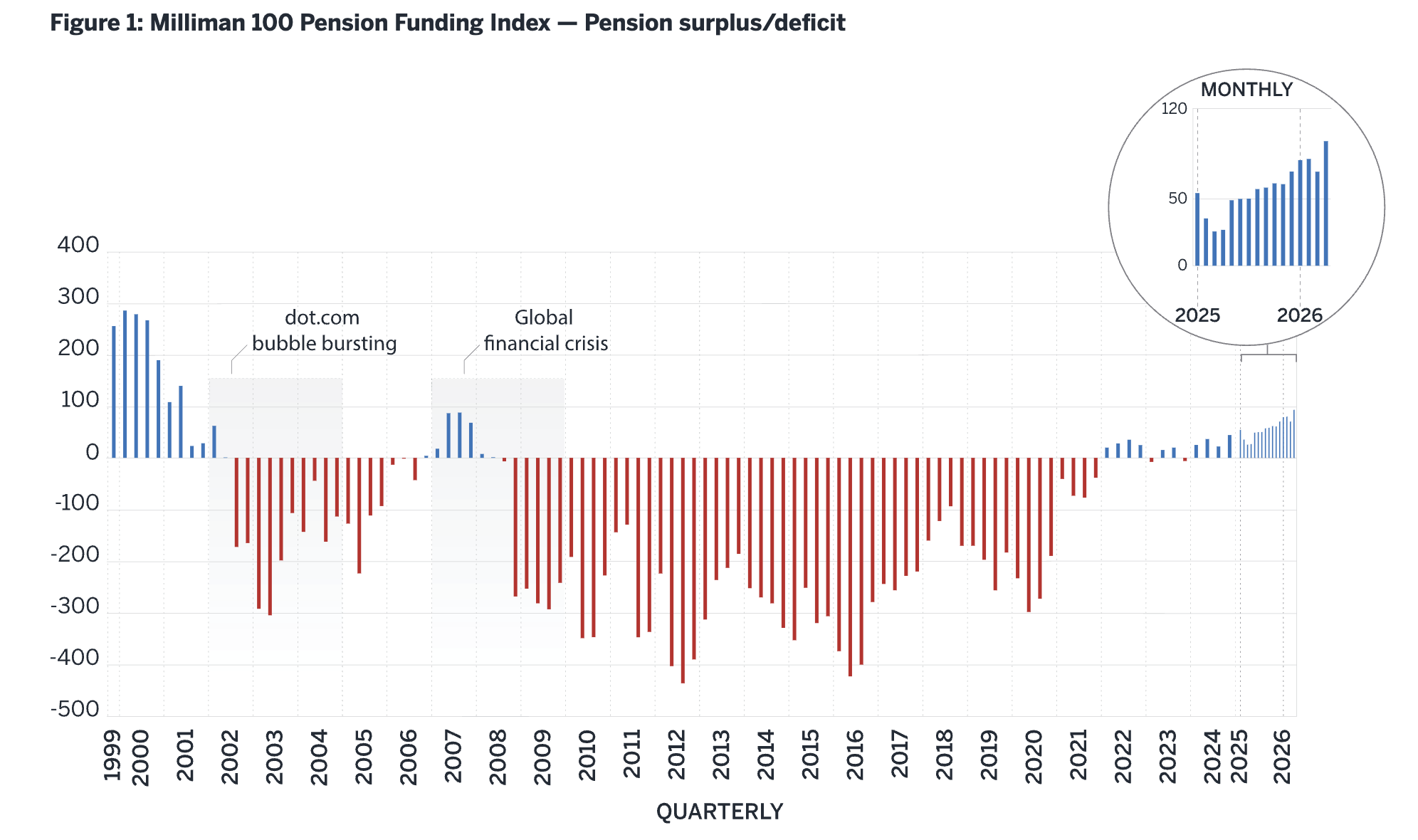

I reported this morning that Milliman’s monthly study of the top 100 corporate plans showed the highest average funded ratio since before the GFC. Pension earnings are being created because of these surplus assets. Now is the time for Corporate America to rethink their retirement offerings. DC plans were intended to be supplemental to DB funds. Asking the average American to fund, manage, and then disburse a benefit with little disposable income, no investment acumen, and no crystal ball to help with longevity is silly policy that is failing us.

Bring back the defined benefit plan for the masses. In the process, we bring back an element of financial security and a level of certainty not found through DC plans. Those that have worked 40+ years shouldn’t have to worry that they may outlive their financial resources, when they should be enjoying the fruits of their labor.