By: Russ Kamp, CEO, Ryan ALM, Inc.

Most everyone who lived through the ’80s will remember the slogan “Just Say No”. The slogan was created and championed by Nancy Reagan during her husband’s presidency. As you’ll recall, the slogan was part of the U.S.-led war on drugs.

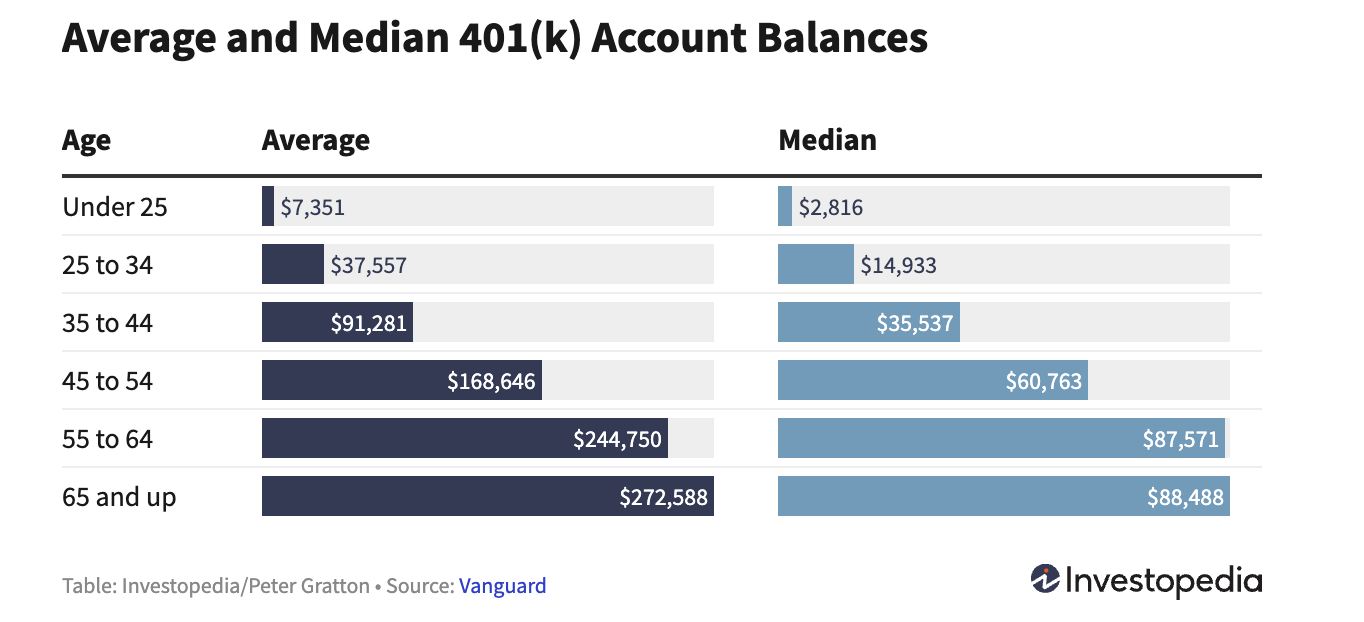

I’d like to reuse the slogan of JUST SAY NO as it relates to using alternatives, especially private equity and credit in defined contribution (DC) plans. DC plans are proving to be a failed model for the vast majority of participants given the anemic median balances, as asking untrained individuals to fund, manage, and then disburse a “retirement” benefit with little to no disposable income, investment acumen, or a crystal ball to help with longevity is just silly policy. Trying to push alternatives onto these folks is maddening! They don’t need more offerings providing complicated structures, little transparency, high fees, and poor liquidity.

Importantly, what happened to being a “qualified or accredited” investor? As you may recall, private investments are restricted in most cases to individuals who meet certain financial thresholds that have been established by regulatory authorities. These considerations included minimum income levels (>$200k for some period of time and sustainable), net worth considerations at >$1 million not including your primary residence, and finally, investment knowledge, in which individuals need to demonstrate sufficient knowledge and experience in financial and business matters to evaluate the risks and merits of a prospective investment. Do you honestly think that the average 401(k) participant qualifies under any of these considerations?

The alternative suite of product offerings is proving to be challenging for many institutional investors/boards, often requiring the retention of a specialist consultant to support the plan’s generalist advisor. Given that reality, does it really make sense that an untrained individual will truly understand the potential risk and reward characteristics? Furthermore, these investments are NOT the magic elixir that they are made out to be. Performance results range far and wide and liquidity (capital distributions) is proving illusive. Do providers of these products really believe that more assets are needed at this time given how difficult it is to invest the current dry powder?

I put a similar comment to this post on LinkedIn.com earlier today. Somebody commented that a simple NO without exploration perhaps would violate my fiduciary responsibility. My answer: Someone needs to be the grown up in the room trying to keep our industry’s greedy hands off DC plans. I believe that I am acting very much in a fiduciary capacity.

I could apply the “Just Say No” slogan to so many practices within our pension industry, but for now I’ll restrict it to this one area of concern. This one rant!