By: Russ Kamp, CEO, Ryan ALM, Inc.

I was recently asked by a member of our investment/pension community if there was a common thread that linked my various roles during my 45-years in this business. After some thought, I said YES. For my nearly 20-years in consulting, or as the CEO for Invesco’s quant business or now at Ryan ALM, Inc. my roles have been highlighted by finding unique solutions to client or prospect challenges. I never believed that there existed an off-the-shelf-solution for my client’s unique requirements.

I continue to be motivated by this belief. I find it disconcerting that pension plans funded at quite different levels (60% vs. 90%) could have the same asset allocation. It makes no sense, yet we see that all the time. EVERY pension plan has a unique set of liabilities and asset allocation decisions should reflect those characteristics.

As an example, I attended a client’s quarterly meeting recently and listened to a consultant’s presentation regarding a new variable plan. We manage money for the legacy DB pension fund. The consultant explained that the new fund had a 5% annual return target. Yet they went on to say that the asset allocation was 60% equity, 35% fixed income, and 5% alternatives. WHY?

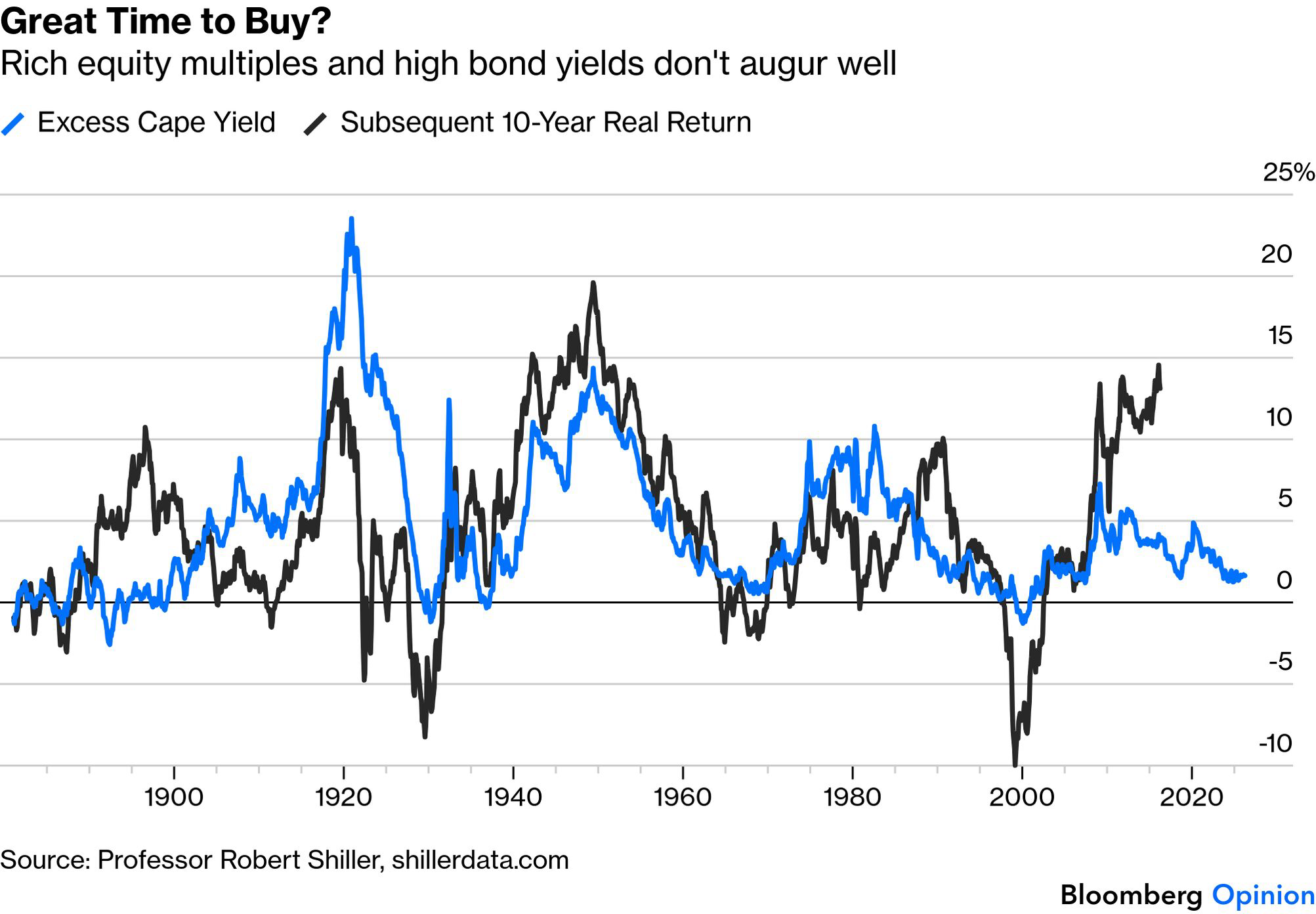

In today’s environment of much higher interest rates, investment grade corporate bonds of basically any maturity would provide a 5+% interest rate. Equities will likely get you more than 5% over time, but given the fund’s annual target and narrow corridor, why live with investments that come with far greater annual volatility, especially given today’s valuations, which are quite stretched by most measures?

Again, it appears to me that a 60%/35%/5% asset allocation is more of an off-the-shelf approach than one developed specifically for this client. For many plans today, the ability to meet the annual required contribution (ARC) is proving problematic. As we witnessed during the decade of the oughts, major market dislocations can have a profound impact on the sponsoring organization through ever increasing contributions. Furthermore, liquidity to meet ongoing monthly benefit payments, especially for negative cash flow plans, is proving to be difficult. These challenges need to be solved on an individual fund basis and not through a general approach.

We, at Ryan ALM, Inc., believe that the primary objective in managing a DB pension plan is to SECURE the promised benefits at a reasonable cost and with prudent risk. It is not a return objective. Since every plan has a unique set of liabilities, no generic index or “traditional” asset allocation could ever replicate those liabilities. Managing a pension plan needs to start with understanding the client’s objective.