By: Russ Kamp, CEO, Ryan ALM, Inc.

Milliman is out with the year-end report on corporate pension funding and it tells a beautiful story. The Milliman 100 Pension Funding Index (PFI), is reporting an average 105% funded ratio at the end of 2024 compared to 99.5% at the end of 2023. But wait, assets for the top 100 plans only grew by 4.2%, which must have been below the stated ROA. Furthermore, total assets declined by $26 billion after accounting for benefits and expenses. How is that possible? Oh, I get it, the growth in liabilities matters.

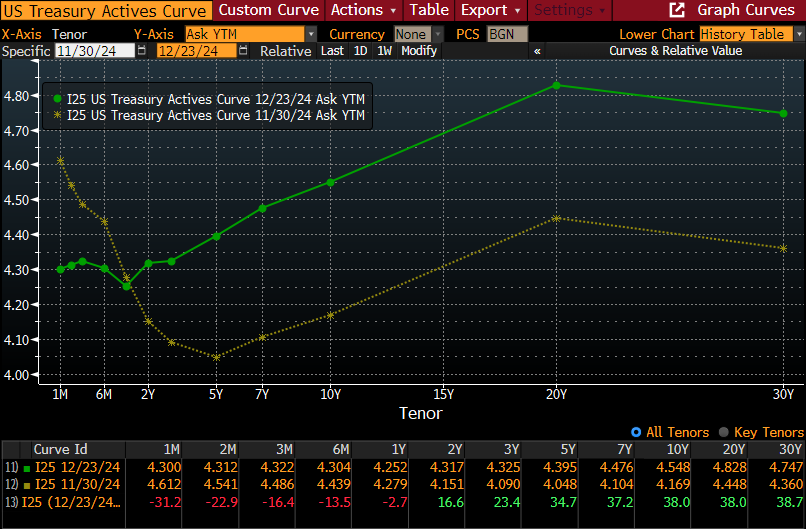

Milliman is reporting that the discount rate used to value corporate pension liabilities increased 59 bps during the year from 5.0% at 12/31/23 to 5.59% as of year-end 2024. That significant move up in rates drove the present value of those pesky liabilities down by -$94 billion creating a $68 billion improvement in the asset/liability relationship and a significantly improved funded ratio! Congrats corporate America and the participants that you serve!

I was recently asked by an industry reporter if the “underperformance” of corporate plans versus other sponsoring groups – public and multiemployer – should be a concern. I, of course said NO, that managing a DB plan is all about the relationship of assets to liabilities. Both could have negative or positive growth rates, but if asset growth exceeds liability growth the plan wins! It is really a simple concept.

Now, I would suggest that corporate America get even more conservative at this time, as we live in an environment of stretched valuations, stubborn inflation, the prospect of higher rates, etc. Congrats on your collective victory. Secure those promises through a cash flow matching (CFM) strategy that will not only provide you with the security that the benefits are protected, but the enhanced liquidity and lengthened investing horizon for any residual growth assets will also be realized.

As always, thanks to Zorast Wadia and the Milliman organization for taking the time to produce this important analysis. Without good data, it is difficult to know how to play the game – assets versus liabilities is the name of the pension game!