I produced the initial “Like A Bridge Over Troubled Waters” post on October 1, 2021. In that post, I highlighted the fact that the decade of the ’00s witnessed two episodic market events that produced nearly -50% declines in each instance crushing pension funding in the process. Most of Pension America had entered the ’00s with well-funded plans, and in many cases, pension systems that enjoyed a surplus. It was truly unfortunate that the focus at that time continued to be on achieving the return on asset assumption (ROA) and not on securing the promised benefits. For if they had adjusted their focus funded status and contribution costs would have been stable. Regrettably, funded ratios plummeted, and in the process, contributions skyrocketed.

The bridge that was referred to in the previous post was an asset allocation framework (not new) that called for plan assets to be bifurcated into liquidity (beta) and growth (alpha) buckets and away from a single asset allocation strategy focused exclusively on the ROA. In this implementation, benefits and expenses would be secured through the investment in a cash flow matching bond strategy that effectively used the asset cash flows from the bonds to meet the liability cash flows. This strategy bought time for the alpha assets to recoup their losses while also allowing them to grow unencumbered, as they were no longer a source of liquidity.

The markets – both stocks and bonds- have enjoyed an incredible period of time since the Great Financial Crisis that ended in March 2009. This period of time has once again created complacency for the plan sponsor and their advisors. Everyone knows that stocks outperform bonds over time (roughly 82% of the time in 10-year periods) and equities generally provide a positive return, so why do anything else – let the good times roll! Well, the growth in contributions from 2000 has been extraordinary despite the “strong” market returns of the last 12 years or so. How is that possible? Think that your system and the fund’s sponsor(s) can continue to support these rapidly growing contributions? Think again!

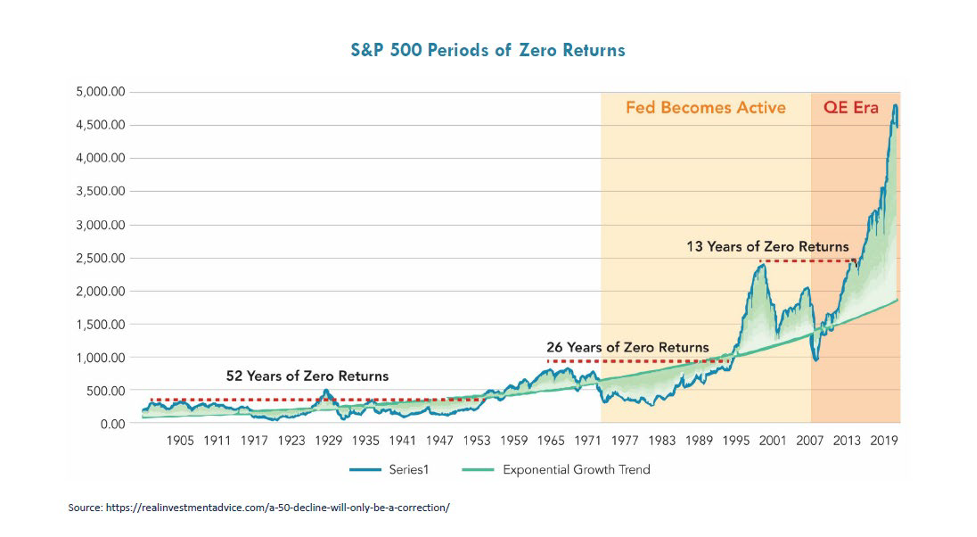

The chart above is mindblowing! I have realinvestmentadvice.com (who created the graph) and Chris Scibelli, for bringing this to my attention. In our previous post, we talked about a bridge that spanned roughly 12-13 years. Can you imagine being in the midst of a 52-year timeframe in which equities provide no return? How about that incredible stretch being followed by 26-year and 13-year episodes? Do you still think that equity markets (as defined by the S&P 500) always outperform or add value? Do you think that the trend of plowing more and more pension assets into equity and equity-like product makes sense? What if the 39-year bull market in bonds is dead? What if equities are about to produce another -50% decline as the risk-on trade ceases to exist because all the stimulus has dried up?

If these scenarios play out, do you think that Pension America’s DB systems survive? No way! I don’t care if public funds think that they are perpetual. Just because they may be perpetual doesn’t mean that they are sustainable! If you think that the significant increase in contribution expenses witnessed since the 2000 market correction is outrageous, just wait to see what happens when annual contributions become 30% or more of a municipality’s budget.

It is no secret that rates will rise as a result of significant inflation. Bondholders will not continue to buy bonds that have 5% or greater negative real returns. In a rising interest rate environment, both bonds and stocks will be hurt. In that scenario achieving the ROA will be incredibly problematic (impossible?). Most market participants haven’t lived through a bear market in bonds. It won’t be pleasant.

DB pension plans need to be protected and preserved. However, doing the same old, same old, is not the right strategy. Waiting for the markets to show their hand before doing something is like playing Russian Roulette. Now is the time to convert your traditional return-seeking fixed-income assets into a cash flow matching strategy that will use bonds for their intended purpose – cash flow! Bonds are the only asset with a known payout and terminal value. Use those knowns to construct a portfolio that will ensure that you have the assets needed to SECURE the promised benefits when the time comes due to make those payments. Trying to find liquidity in a rapidly deteriorating market environment is as difficult a task as exists.

By having your cash flow-driven investing program matched carefully with your plan’s liabilities, you not only improve liquidity, but you eliminate interest rate risk for that portion of the portfolio, as you will be defeasing a future value that isn’t interest-rate sensitive. Furthermore, you are extending the investing horizon for those alpha assets that need time to grow. They shouldn’t be a source of liquidity. It isn’t too late to adopt, but time to act might be getting short.

Pingback: It Doesn’t Have to be This Way – Ryan ALM Blog