By: Russ Kamp, CEO, Ryan ALM, Inc.

Despite the chaotic nature of our markets and geopolitics, it is comforting that I can report weekly on the progress being made by the PBGC implementing the critical ARPA legislation. That is not to say, that the 2nd Circuit’s recent ruling isn’t creating a bit of chaos, too.

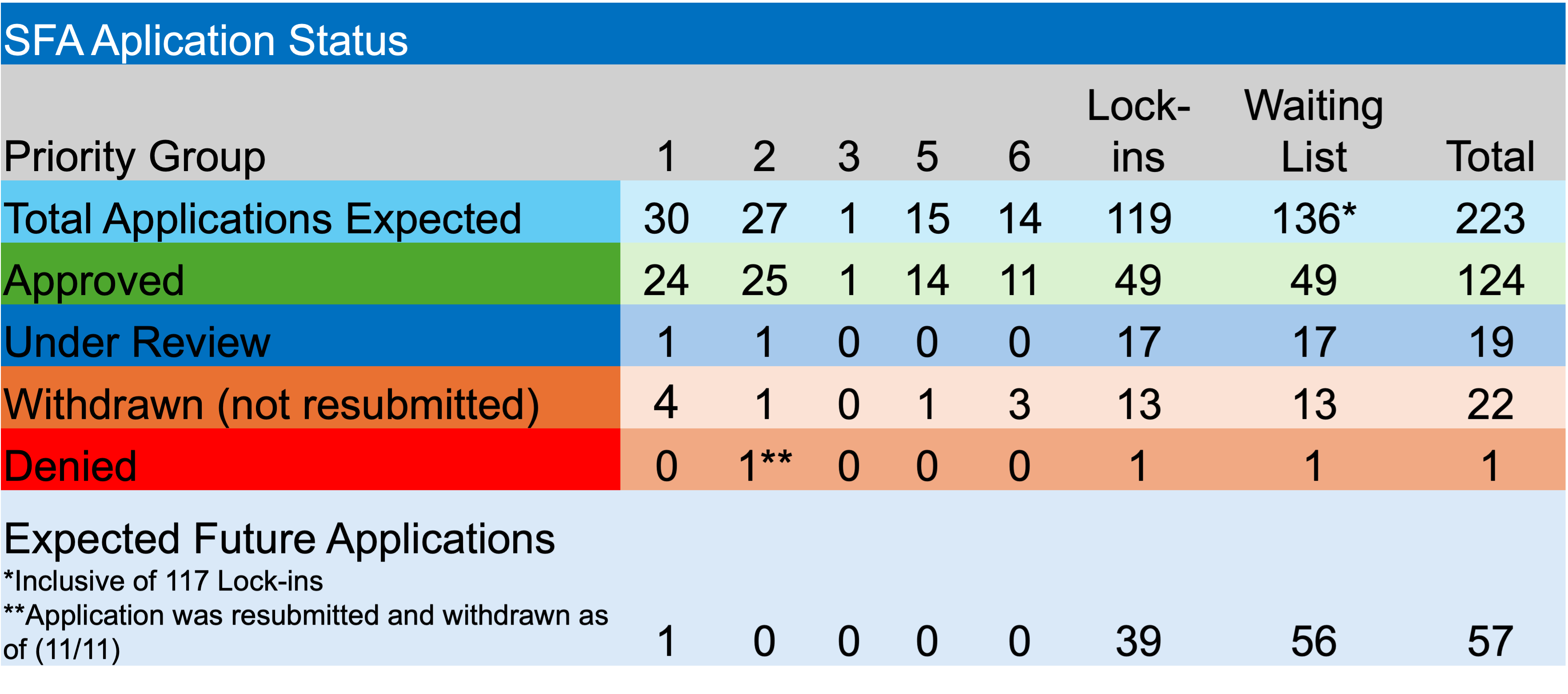

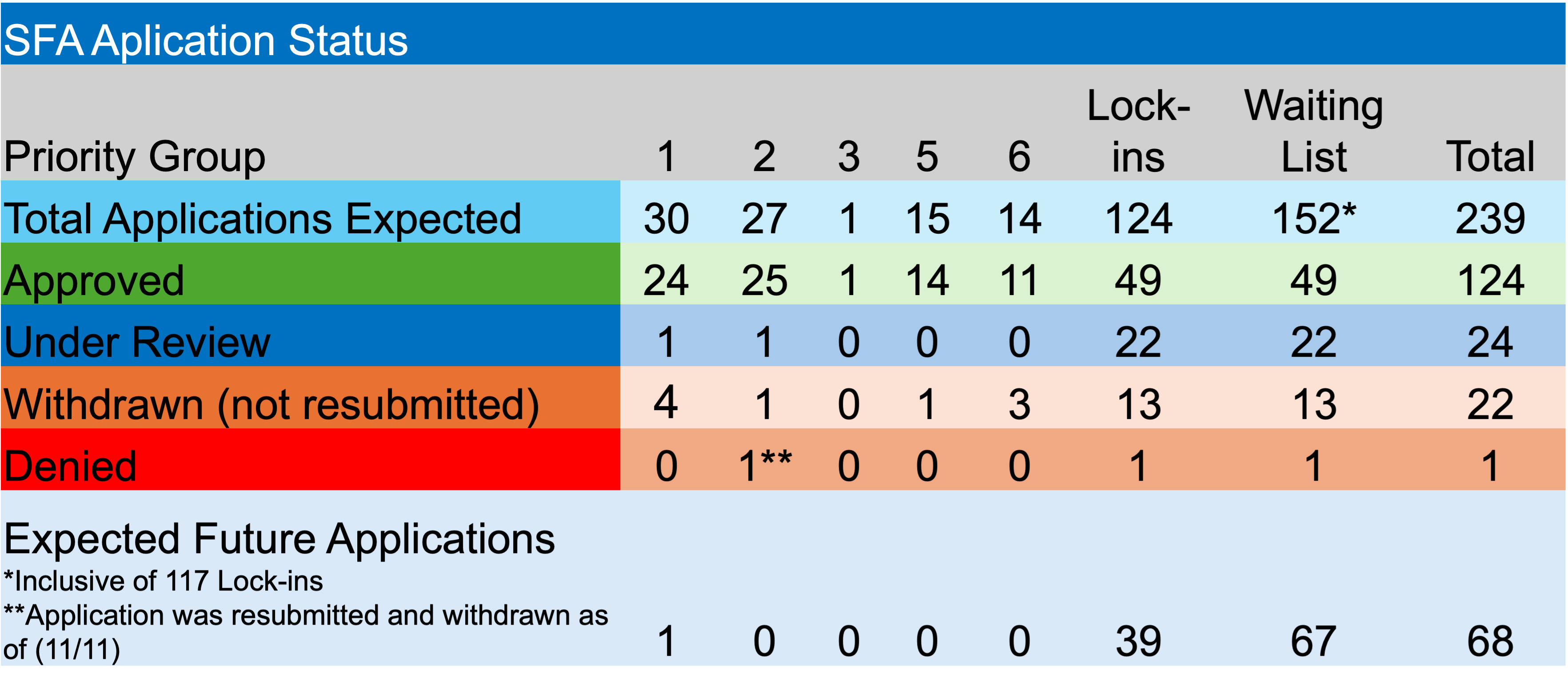

Regarding last week’s activity, the PBGC’s efiling portal must have been wide open, as they accepted initial applications from 5 pension plans residing on the waitlist. The PBGC will now have 120-days to act on these submissions.

There were no applications approved, denied, or withdrawn last week, but that isn’t to say that the PBGC rested on its laurels. There were two more plans that repaid a portion of the SFA received, as census errors were corrected. International Association of Machinists Motor City Pension Plan and Western States Office and Professional Employees Pension Fund repaid 1.61% and 1.08% of the SFA, respectively. In total, 57 plans have “settled” with the PBGC, including four funds that had no census errors. To date, $219 million was repaid from grants exceeding $48 billion or 0.45% of the grant.

In other ARPA news, another 16 funds have been added to the waitlist resulting from the 2nd Circuit’s determination that previously terminated plans can seek SFA. We do believe that it will prove beneficial for these plans, but it will stress the resources of the PBGC to meet ARPA imposed deadlines.

Given the highly unpredictable nature of war and tariffs on inflation and U.S interest rates, it isn’t surprising that the U.S. Federal Reserve held the Fed Funds Rate steady last week. We encourage those plans receiving SFA grants to secure the promised benefits through a cash flow matching strategy. Who knows how markets will impact bonds and stocks for the remainder of the year.