By: Russ Kamp, CEO, Ryan ALM, Inc.

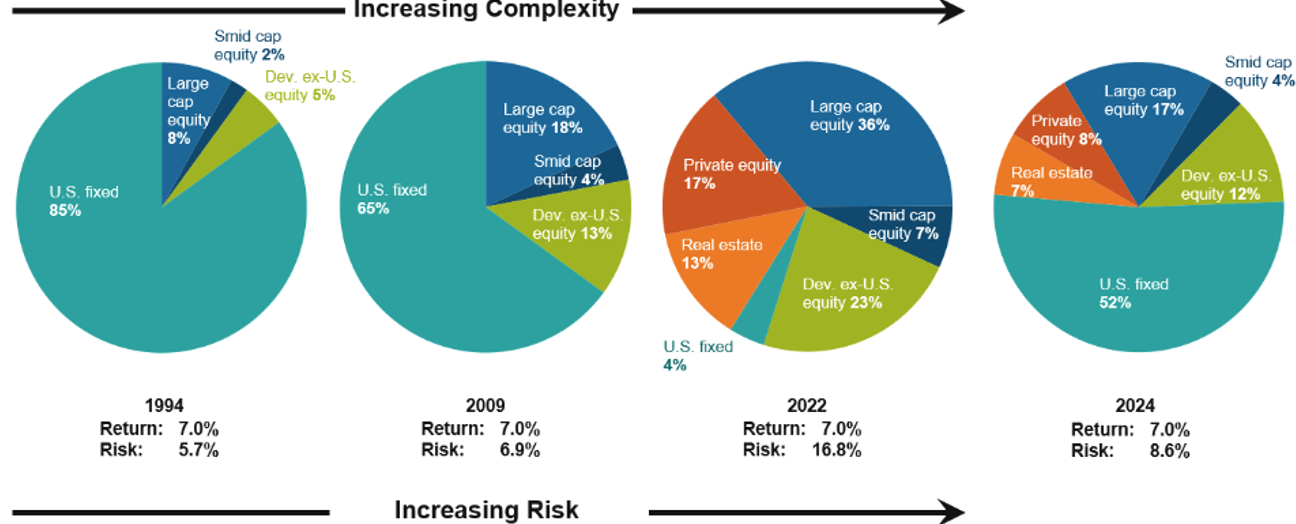

In October 2022, I wrote the following: “I believe that we have overcomplicated the management of DB pension plans. If the primary objective is to fund the promised benefits in a cost-efficient manner and with prudent risk, why do we continue to waste so much energy buying complicated products and strategies that often come with ridiculously high fees and little alpha?”

I still believe that our industry continues to build complicated asset allocation structures unnecessarily. In a recent P&I article, the following was reported: that a public pension system will adjust their asset allocation to reflect new targets including a 4% allocation to hedge funds and 3% to opportunistic credit, alongside increases in private equity to 13.5% from 8% and private debt to 8% from 6.5% — funded by reductions in domestic equities, international equities, and infrastructure.

This action is occurring after the investment consultant ABC recommended the changes following an asset-liability study, with the goal of enhancing protection against volatility and drawdowns while maintaining sufficient liquidity. Can you get more complicated? Are they really claiming that this structure will maintain sufficient liquidity? Sure, there may be a reduction in “volatility” because these strategies are not marked-to-market, as opposed to the public markets, but claiming that sufficient liquidity will be maintained is a joke!

I’ve been arguing for quite some time that the private markets are overbought. As assets continue to flow into these strategies, liquidity has dried up with little capital flowing back to the investor, which is why the secondary markets have flourished. Too many assets in any strategy deflate future returns, which we have witnessed. Regarding hedge funds, which are not aligned with the primary objective in managing a DB pension plan which is a relative objective (assets versus pension liabilities and NOT the ROA) they continue to be extremely expensive offerings that have produced subpar returns for the better part of the last two decades.

If the objective is to maintain sufficient liquidity look no further than cash flow matching (CFM) which will ensure that the necessary liquidity to meet benefits and expenses is available each month of the assignment as far out as the allocation goes without a need for a cash sweep of growth assets. Furthermore, one doesn’t have to pay hedge fund fees to get that “liquidity”. You can get a CFM strategy for 15 bps or less. While your liquidity needs are being met, the CFM portfolio will also extend the investing horizon for the remainder of the fund’s assets enhancing the probability that those less liquid, highly opaque offerings have time to produce the forecasted returns.

Afraid that you are going to give up “return” by using a CFM strategy? We recently completed an analysis for a large public pension system that believed they were <50% funded. We proved that we could fully fund and SECURE the NET liabilities (after contributions) of benefits and expenses (B&E) through 2059! Yes, a CFM portfolio with a YTM of 5.4% was able to fully fund the net B&E for 33-years. In addition, we were able to produce a surplus in excess of $4 billion, which can now just grow and grow and grow. In fact, investing that surplus in an S&P 500 index fund would grow those assets at a 6.5% annual return (the fund’s target ROA) to $35.3 billion by 2059. If the index produced an 8% nominal return for that period those surplus assets grow to >$75 billion that can be used to reduce future contributions, meet future liabilities, and perhaps enhance benefits.

Oh, wait, it gets even better. By investing in just the CFM strategy and the S&P 500 index fund, this plan can reduce annual investment fees from nearly $50 million per year to <$4 million, a reduction of 93%. Those fee savings add another $1.5 billion to the surplus before any return is generated on those savings. As Ripley would say, “BELIEVE IT OR NOT”!

Again, the management of a DB plan is not rocket science. Fund the annual required contributions, focus on the primary objective to SECURE the promised benefits at low cost and prudent risk, and you have a program that is neither complicated nor expensive to administer. When will we learn?