By: Russ Kamp, CEO, Ryan ALM, Inc.

“The worst thing that can happen,” Andrew Junkin, CIO, Virginia Retirement System says, “is that you’re a forced seller in any market.”

That quote appeared in a Chief Investment Officer article from March 4, 2026. We couldn’t agree more with Mr. Junkin. Despite improved funding, public funds are being challenged to find adequate cash flow to meet the monthly benefits and expenses. Two factors are at play: 1) improved funding leads to lower annual contributions, and 2) much heavier allocations to alternatives have dried up liquidity, as expected capital distributions fail to materialize.

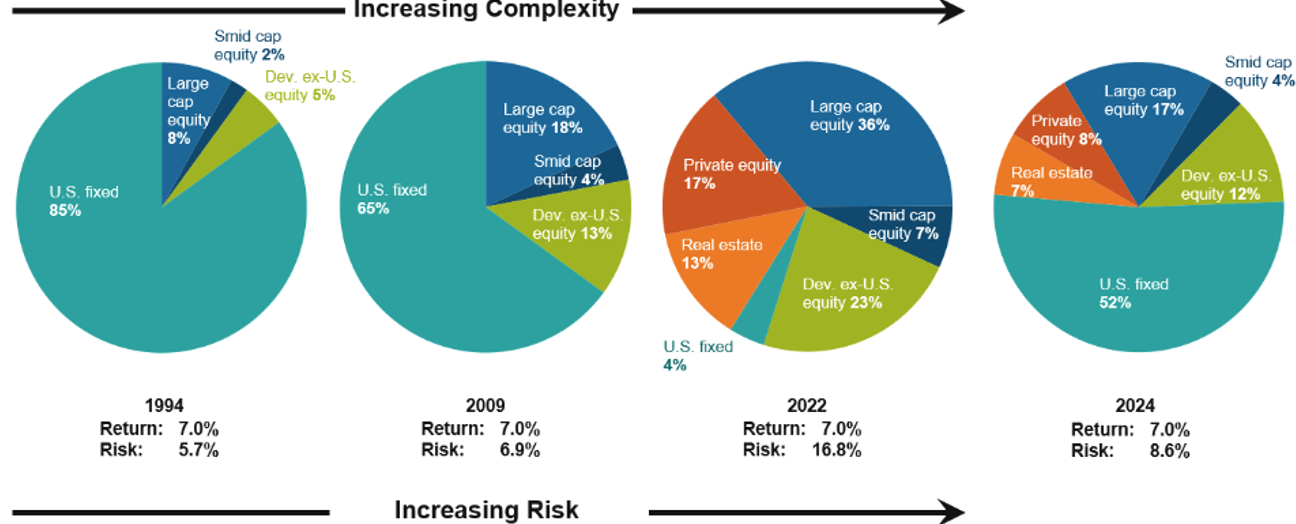

According to a report by NIRS, from 2001 to 2023, public pension plans shifted roughly 20% of public equity and fixed income into alternatives such as private equity, real estate, and private credit. These are illiquid investments. Despite the “wisdom” of the pension crowd, illiquidity is a RISK and not an alpha generator. As more assets shifted into these illiquid investments, the trades became ever more crowded reducing liquidity further. That is, unless one was willing to take a significant haircut through the secondary markets.

As a reminder, public pension funds are designed to become cash-flow negative over time. Contributions into these funds exceed benefits in earlier decades, building a corpus to be used to fund retirements down the road. They are designed to have the last $ pay the last promised benefit. There is no inheritance waiting for the last few beneficiaries.

You want to have adequate liquidity that isn’t forcing the sale of assets at inopportune times? Develop an asset allocation strategy that bifurcates your assets into two buckets – liquidity and growth – and stop the focus on the ROA as if it were the Holy Grail. It isn’t! Use a cash flow matching (CFM) investment strategy to ensure that abundant liquidity is available from next month as far into the future as your allocation goes. The remainder of the assets go into the growth bucket. If you still want to maintain a heavy allocation to alternatives, they can now grow unencumbered as they are no longer a source of liquidity.

The allocation should be driven by the pension plan’s funded ratio and ability to contribute. We recently provided a large fund with an analysis that showed a plan with <50% funding could still secure the promised NET benefits for the next 33-years, while creating a substantial surplus that could now be managed as aggressively as members of that Board could withstand. Not only are the promised benefits secure, but so are the participants who can now sleep well at night knowing that myriad risks won’t sabotage their golden years.