By: Russ Kamp, CEO, Ryan ALM, Inc.

Milliman has released the latest monthly report on the Milliman 100 Pension Funding Index (PFI). As a reminder, this index analyzes the 100 largest U.S. corporate pension plans.

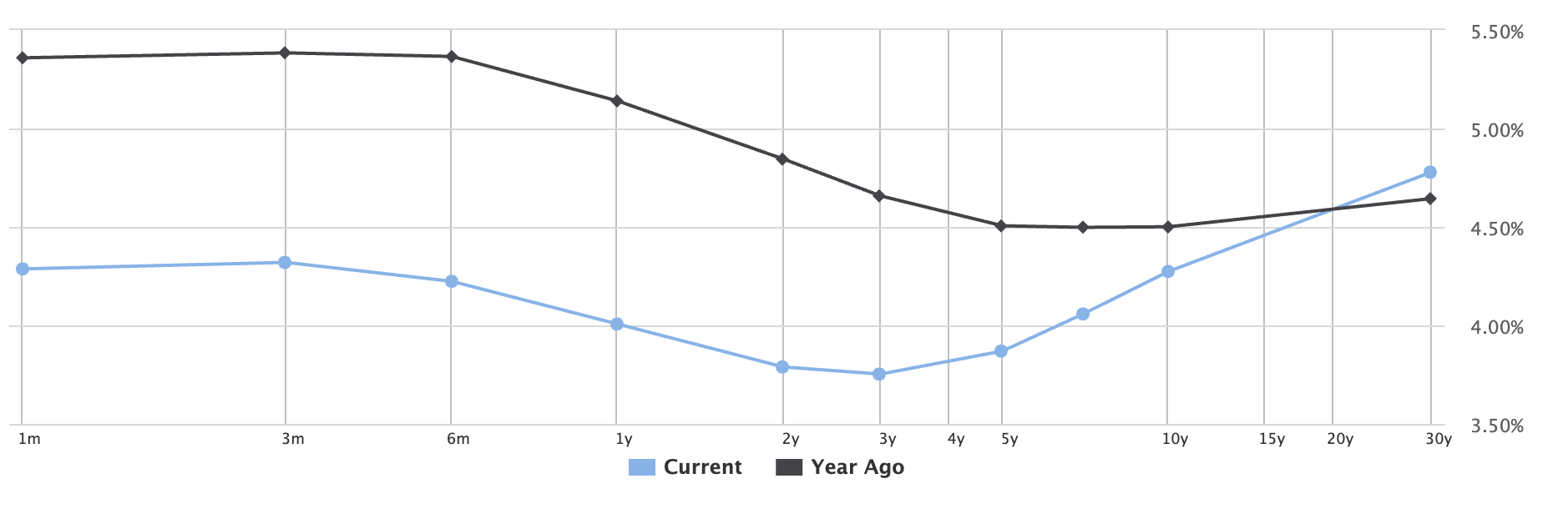

For February, the PFI funded ratio rose from 109.1% as of January 31, to 109.4% as of February 28, marking the highest collective funded ratio since the 109.9% mark observed in July 2001. However, the funding improvement was solely a result of asset performance, as declining discount rates of 14 basis points reduced the discount rate to 5.33% and raised the PFI projected benefit obligation (liabilities) to $1.235 trillion. Fortunately, monthly returns of 2.15% offset the impact of falling U.S. interest rates leading to growth in the market value of plan assets by $22 billion, to $1.351 trillion.

“February’s investment performance drove the month’s $5 billion gain in funding levels,” said Zorast Wadia, author of the Milliman PFI. He went on to say that “while this marks 11 straight months of funding improvements, further declines in interest rates may occur, and ongoing market volatility makes it vital for plan sponsors to undertake surplus-management strategies focused on both sides of the balance sheet.” We continue to support Zorast in recommending that managing assets to liabilities is critical for DB pension plans in all market environments, but especially given the significant uncertainty under which markets are currently operating. As a reminder, the primary objective in managing a DB pension is to SECURE the promised benefits at a reasonable cost and with prudent risk. It is NOT a return objective.

We, at Ryan ALM, do not forecast interest rates, but the impact of rising oil prices (WTI currently up 30.7% as of 9:13 am EST since Friday) will likely have an impact on inflation and interest rates. It will be interesting to see if a potential fall in the value of liabilities proves greater than the potential impact that rising rates might have on equity markets and other assets. Will we see the 12th consecutive month of improved funding levels?

Please click on the link below for a look at the complete Milliman corporate pension funding report.