Ron has produced an interesting piece of research that might just enlighten, if not confuse, some pension folks. I suspect that most folks would believe that a plan’s funded status remains consistent if the desired return on asset (ROA) assumption is achieved annually. However, that is definitely not the case for a plan that is in a deficit position (assets less than the plan’s liabilities).

In fact, a plan with a 70% funded ratio (a 30% deficit to plan liabilities) striving for a 7% ROA can achieve that target each of the next 5-years and the funded status deficit will have grown by 42.3%, while maintaining that 70% funded ratio. A 50% funded plan striving for the 7% return target actually needs to achieve a 14% return just to maintain the funded status. Despite maintaining a level Funded Ratio, contributions into the plan will need to rise in order to keep the funded status from continually growing.

When we see reports that public pension funds have an “average” funded ratio of 83%, understand that the collective funded status is likely getting worse unless a significant outperformance occurs relative to the ROA objective, given the 17% funded status deficit. As a result, contributions into these pension plans will be rising.

Milliman’s Public Pension Funding Index (PPFI) has been released for July 2025. As a reminder, the PPFI compiles and analyzes data from the nation’s 100 largest public DB plans.

For the fourth consecutive month, investment gains have led to improved funded ratios for America’s largest public DB funds. July’s investment gain produced a $5 billion increase in the PPFI funded status, and saw the funded ratio improve from 82.9% as of June 30, to 83.0% as of July 31. The indexes constituents produced an estimated market gain of 0.5% during the month, with individual plans’ returns ranging from -0.2% to 1.2%. As a result, total assets for the members of the index are now $5.477 trillion as of July 31. A $20 million increase from the prior month.

Given the static accounting for public fund liabilities, the deficit between plan assets and liabilities shrank with the growth in assets decreasing from $1.127 trillion at the end of June to $1.122 trillion at the end of July. Importantly, there are now 38 plans that are more than 90% funded at month-end. Unfortunately, 11 plans remain at less than 60% funded.

According to Becky Sielman, co-author of the Milliman PPFI, there are 14 plans with a funding “surplus”, which sounds great, but the plan’s ROA is the discount rate permitted under GASB accounting, which is likely substantially higher than the discount rate for corporate DB plan liabilities that utilize a AA corporate blended rate. As a result, pension liabilities are understated. One can only hope that U.S. interest rates remain stable or rise from their current levels, as a declining rate environment would put additional funding pressure on liabilities, which are bond-like in nature. Please click on the link below to view the entire report.

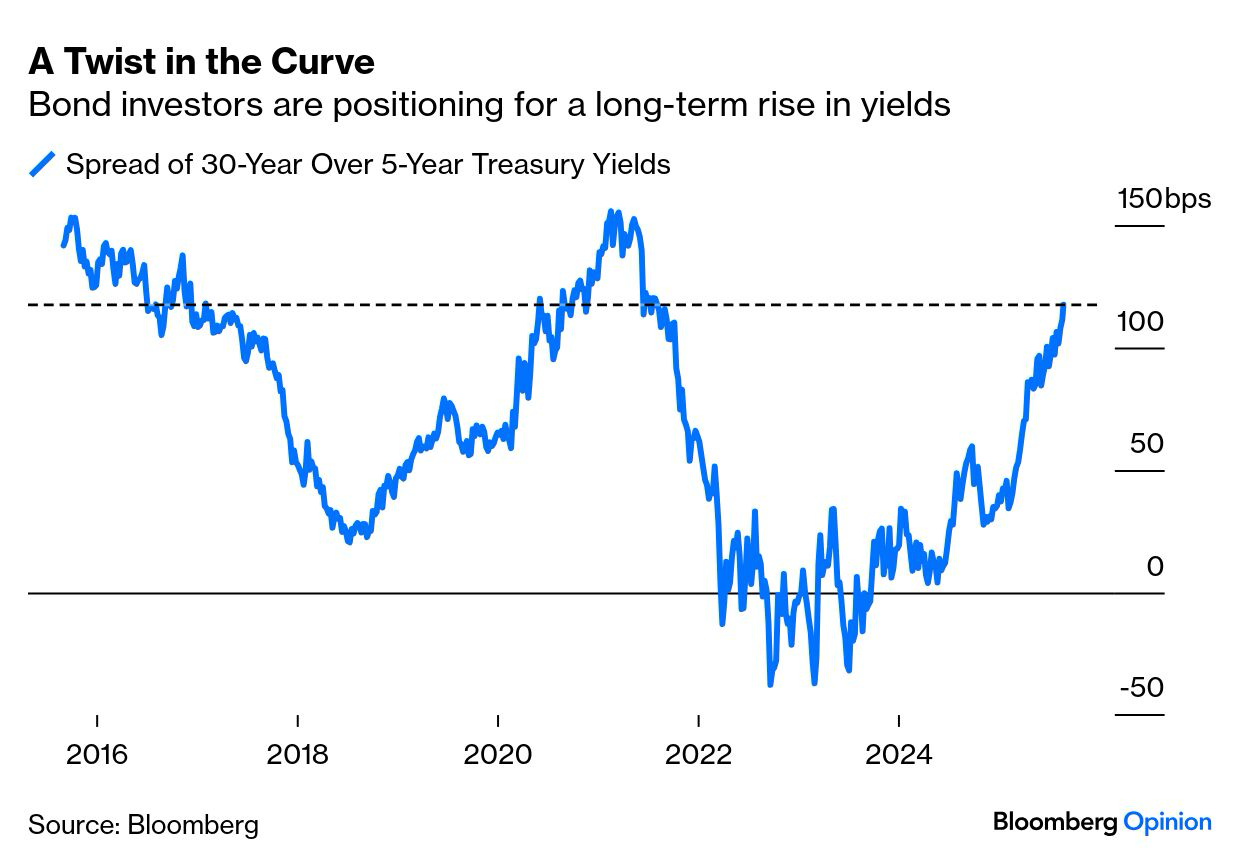

In addition to publishing my thoughts through this blog, I frequently put sound bites out through LinkedIn.com. The following is an example of such a comment: Given Powell’s statement about “balancing dual mandates”, it seems premature to assume that the Fed’s next move on rates is downward. Tariffs have only recently kicked in and their presence could create a very challenging situation for the Fed should inflation continue on its path upward. Market reaction seems overblown. September’s CPI/PPI numbers could be very interesting.

As a follow-up to that comment, here is a graph from Bloomberg highlighting the recent widening in the spread between 5-year and 30-year Treasuries, which is at its widest point in the last 4 years. This steeping of the yield curve would suggest that inflation is being more heavily anticipated on the long end.

As I mentioned above, the reaction to Powell’s comments from Wyoming last Friday seemed overblown given the rethinking about “dual mandates”. Inflation has recently reversed the downward trajectory and with the impact of tariffs yet to be truly felt, it is doubtful that we’ll see inflation fall to levels that would provide comfort to the U.S. Federal Reserve policy makers. Yes, there may be a small (25 bps) cut in September, but should inflation continue to be a concern the spread in Treasury yields referenced above could continue to widen. President Trump’s goal of jumpstarting the housing market through lower mortgage rates would not likely occur.

From a pension perspective, higher rates reduce the present value of those future promised benefits. They also provide implementers of cash flow matching (CFM) strategies, such as Ryan ALM Advisers, LLC, the opportunity to defease those pension liabilities at a lower cost (greater cost savings). Bond math is very straight forward. The higher the yield and the longer the maturity, the greater the cost savings. Although higher rates might not be good for U.S. equities, especially given their current valuations, the ability to reduce risk at this time through a CFM strategy should be comforting.

Bifurcate your asset allocation into two buckets – liquidity and growth. The liquidity bucket will house the CFM strategy, providing all the necessary liquidity to meet ongoing monthly obligations as far into the future as the allocation will cover. The remaining assets (all non-core bonds) in the growth or alpha portfolio will now have more time to just grow unencumbered, as they are no longer a source of liquidity. Time is a critical investment tenet, and with more time, the probability of meeting the expected return is enhanced.

There is tremendous uncertainty in our markets and economy currently. One can bring an element of certainty to the management of pensions, live with great uncertainty.

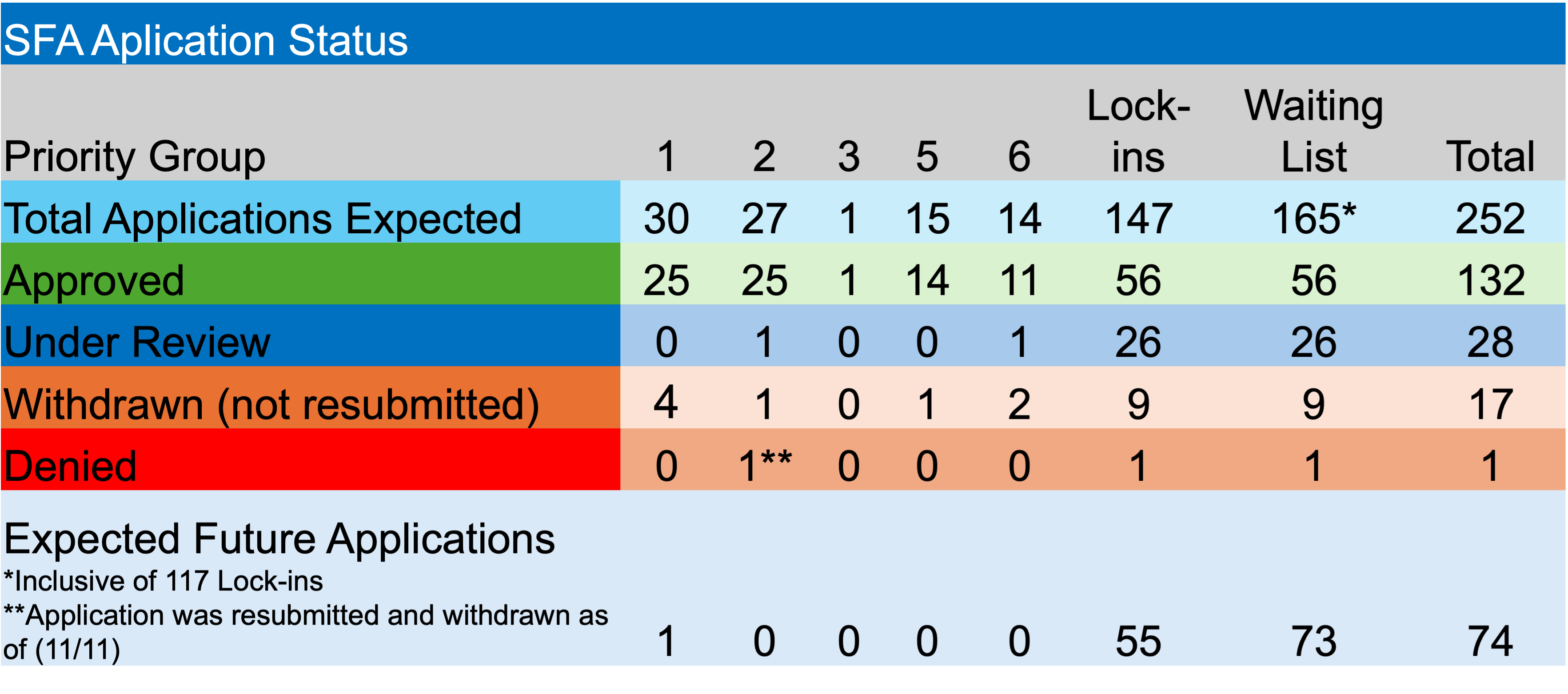

Welcome to the last week of “summer”. I don’t know about you, but I can believe that Labor Day is next weekend. I suspect that the PBGC is feeling the same way as they continue to work their way through an imposing list of applicants with a December 31, 2025, deadline for initial applications to be reviewed. As the chart below highlights, they have their work cut out for them.

Regarding last week’s activity, the PBGC did not accept any new applications as the e-Filing portal remains temporarily closed. However, they did approve the revised applications for two funds. Laborers’ Local No. 91 Pension Plan (Niagra Falls) and the Pension Plan of the Asbestos Workers Philadelphia Pension Fund have been awarded a total of $96.2 million in SFA and interest that will support 2,057. This brings the total of approved applications to 132 and total SFA to $73.5 billion – wow!

In other ARPA news, I’m pleased to announce that there were no applications denied or withdrawn during the previous week, but there were two more funds that were asked to repay a portion of the SFA received due to census errors. Sixty-four funds have been reviewed for potential census errors, with 60 having to rebate a small portion of their grants, while four funds did not have any issues. In total, $251.7 million has been repaid from a pool of $52.3 billion in SFA received or 0.48% of the grants awarded. The $251.7 relative to the $73.5 billion in total SFA grants would be only 0.34% of the total awards.

Lastly, three more funds have been added to the waitlist. There have been 165 non-Priority Group members on the waitlist including 56 that have received SFA awards, while another 26 are currently being reviewed. That means that 82 funds must still file an application reviewed and approved in a short period of time.

As stated above, pension funds sitting on the waitlist must have the initial application reviewed by the PBGC by 12/31/25. Any fund residing on the waitlist after that date loses the ability to seek SFA support. Applications that have been reviewed prior to 12/31/25 may still get approval from the PBGC provided the approval arrives before 12/31/26. I don’t see them getting through the remaining 74 waitlist funds by the end of 2025.

There recently appeared in my inbox an article from an investment advisory firm discussing Cash Flow Driven Investing (CDI). Given that CDI, or as we call it Cash Flow Matching (CFM), is our only investment strategy, I absorb as much info from “competitors” as I can.

The initial point in the article’s summary read “There is no one-size-fits-all approach for cashflow driven investment strategies.” We concur, as each client’s liabilities are unique to them. Like snowflakes, there are no two pension plan liability streams that are the same. As such, each CDI/CFM portfolio needs to reflect those unique cash flows.

The second point in their summary of key points is where we would depart in our approach. They stated: “While most will have a core allocation to investment grade credit, the broader design can vary greatly to reflect individual requirements.” This is where I believe that the purpose in using CFM is confused and unnecessarily complicated. CFM should be used to defease a plan’s net outflows with certainty. At Ryan ALM, Inc. we use 100% of the bond assets to accurately match the liability cash flows most often through the use of investment-grade corporate bonds. Furthermore, It is a strategy that will reduce risk, while stabilizing the plan’s funded status and contribution expenses associated with the portion of the liability cash flows that is defeased. It is not an alpha generator, although the use of corporate bonds will provide an excess yield relative to Treasuries and STRIPS, providing some alpha.

As we’ve discussed many times in this blog, traditional asset allocation approaches having all of the plan’s assets focused on a return objective is inappropriate for the pension objective to secure and fully fund benefits in a cost-efficient manner despite overwhelming use. We continue to espouse the bifurcation of the assets into liquidity and growth buckets. The liquidity bucket should be an investment-grade corporate bond portfolio that cash flow matches the liability cash flows chronologically from the next month as far out as the allocation will cover. The remaining assets are the growth or alpha assets that now have time to grow unencumbered.

Why take risk in the CFM portfolio by adding emerging markets debt, high yield, and especially illiquid assets, when the purpose of the portfolio is to create certainty and liquidity to meet ongoing benefits and expenses? If the use of those other assets is deemed appropriate, include them in the alpha bucket. As a reminder, CFM has been used successfully for many decades. Plan sponsors live with great uncertainty every day, as markets are constantly moving. Why not embrace a strategy that gives you a level of certainty not available in other strategies? Use riskier strategies when they have time to wade through potentially choppy markets. CFM provides such a bridge. If you give most investment strategies a 10-year time horizon without the need to provide liquidity, you dramatically enhance the probability of achieving the desired or expected outcome.

Unfortunately, we have a tendency in our industry to over-complicate the management of pensions. Using a CFM strategy focused on the plan’s liabilities, and not the ROA, brings the management of pensions back to its roots. Take risks when you have the necessary time. Focusing the assets on the ROA creates a situation in which one or more assets may have to be traded (sold) in order to meet the required outflows. Those trades might have to be done in environments in which natural liquidity does not exist.

We hope that you are enjoying a wonderful summer season. Thanks for taking the time to visit our blog, where we’ve now produced >1,650 mostly pension-related posts.

I wanted to share the following email exchange from earlier this week. I received an email at 6:40 pm on Monday from a senior member of the actuarial community who is familiar with our work. He said that he had a client meeting on Wednesday and he was wondering if we could model some potential outcomes should the plan decide to take some risk off the table by engaging a cash flow matching strategy (CFM).

The actuary gave us the “net” liabilities (after contributions) for the next 10-years and then asked two questions. How far out into the future would $200 million in AUM cover? If the client preferred to defease the next 10-years of net liabilities, how much would that cost? We were happy to get this inquiry because we are always willing to be a resource for members of our industry, including plan sponsors, consultants, and actuaries.

We produced two CFM portfolios, which we call the Liability Beta Portfolio™ or LBP, in response to the two questions that had been posed. In the first case, the $200 million in AUM would provide the client with coverage of $225.8 million in future value (FV) liabilities through March 31, 2031 for a total cost of $196.3 million. Trying to defease the next 10-years of liabilities would cost the plan $334.8 million in AUM to defease $430 million in net liabilities.

$200 million in AUM

10-year coverage

End Date

3/31/31

7/01/35

FV

$225,750,000

$430,000,000

PV

$196,315,548

$334,807,166

YTM

4.52%

4.75%

MDur

2.73 years

4.45 years

Cost Savings$

-$29,424,452

-$95,192,834

Cost Savings%

13.04%

22.14%

Excess CF

$230,375

$679,563

Rating

BBB+

A-

As we’ve mentioned on many occasions, the annual cost savings to defease liabilities averages roughly 2%/year, but as the maturity of the program lengthens that cost savings becomes greater. We believe that providing the necessary liquidity with certainty is comforting for all involved. Not only is the liquidity available when needed, but the remaining assets not engaged in the CFM program can now grow unencumbered.

If you’d like to see how a CFM program could improve your plan’s liquidity with certainty, just provide us with the forecasted contributions, benefits, and expenses, and we’ll do the rest. Oh, and by the way, we got the analysis completed and to the actuary by 12:30 pm on Tuesday in plenty of time to allow him to prepare for his Wednesday meeting. Don’t be shy. We don’t charge for this review.

Happy to share with you a recent research piece by Ron Ryan discussing the problem with YTM as a return calculator. His 50+ years as an industry-leading fixed income researcher/portfolio manager provide him with a unique understanding of misleading yield calculations.

As Ron points out, Yield to Maturity (YTM) assumes you will reinvest every six months at the purchase YTM until maturity of the bond. How could this happen? Yields are changing every day, if not continuously. Furthermore, will you reinvest exactly every six months into the same maturity and same YTM? Sounds like Mission Impossible! In fact, the reinvestment rate on any bond is based on the total return of what you reinvested into. How many folks truly appreciate that fact?

As always, you can find this research note along with years of additional research insights at RyanALM.com. We hope that you find our insights meaningful.

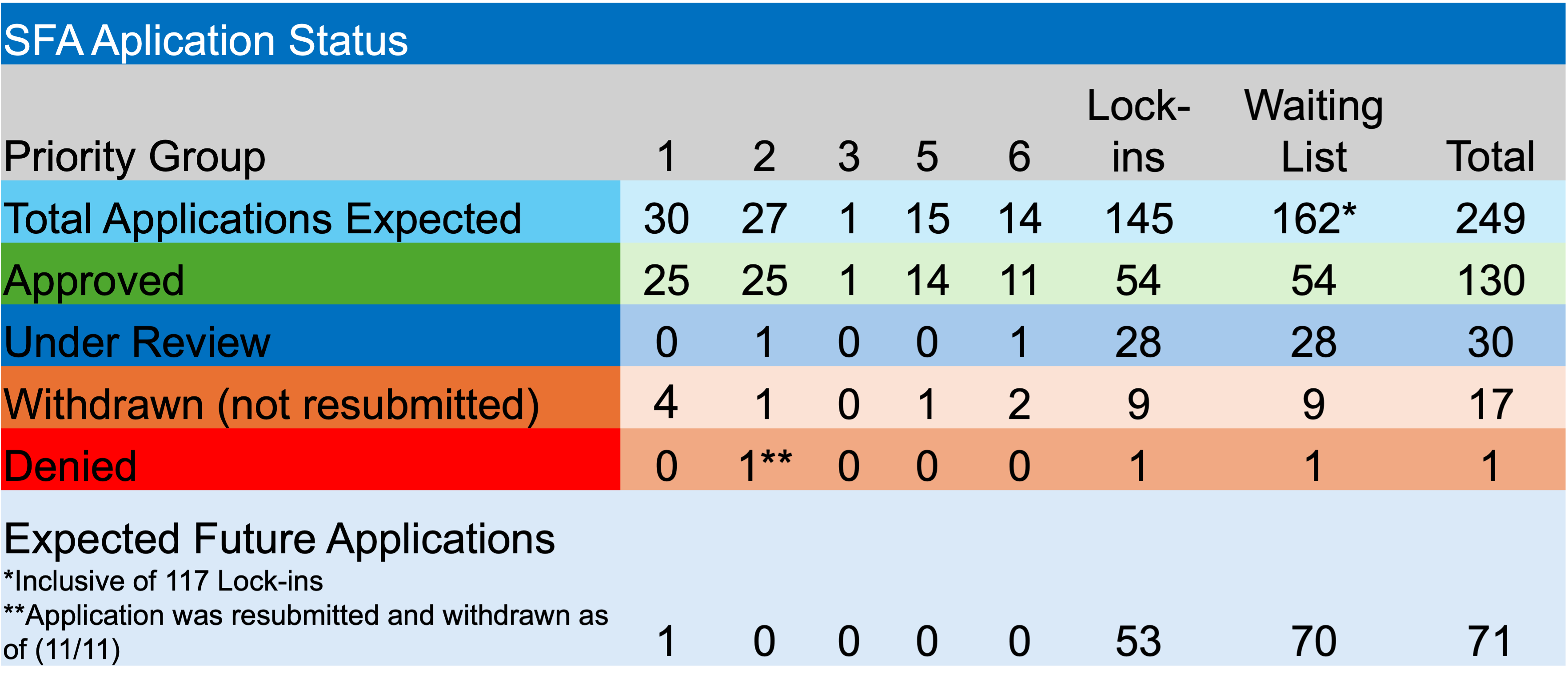

Hard to believe that we are nearly 2/3rds of the way through 2025. I suspect that the PBGC is having a hard time with that reality given the workload that remains with 119 multiemployer plans still seeking a successful review of their SFA application. Seventy-one applications have yet to be submitted through the PBGC’s e-Filing portal.

As for last week, there were no applications approved and none have been since July 29, when Laborers’ Local No. 130 Pension Fund received $33.3 million in SFA to support its 641 plan participants. However, there were 3 applications submitted for review. These applications were from none-priority group members submitting revised applications. There are currently 30 applications before the PBGC, which has 120-days to act on each or they are automatically approved.

I’m pleased to report that no applications were denied or withdrawn during the previous week. There were also no pension funds required to repay a portion of the SFA deemed excessive due to census errors. It has been since August 1, 2025, that we’ve had a fund repay a portion of the SFA. There was one new fund added to the waitlist, which now stands at 162 members. Chicago Foundry Workers Pension Plan added its name to the list on August 11th. As reported above, there are still 71 multiemployer plans that have not submitted applications at this time.

As you may recall, when the Butch Lewis Act was first contemplated, the folks at Cheiron initially defined the potential universe of SFA recipients as 114 funds. Today there are 249 funds seeking SFA support, of which 130 have already been approved. As a reminder, eligible plans must apply for SFA by December 31, 2025. Those filing revised applications have until December 31, 2026. Any distribution of SFA must be completed by September 30, 2030, due to legislative sunset rules.

The PBGC is averaging about 6-7 submissions per month. Based on that pace, it doesn’t seem possible that many of the 71 members on the waitlist that haven’t submitted applications will be able to meet that 2025 deadline. More to come.

With the demise of the defined benefit plan for many workers in the US private sector, Social Security benefit payments become ever more important for a greater percentage of the American retirees and those with disabilities. There have been several stories recently about Social Security and what the “average” recipient might receive in 2026 and worse, what their benefit reduction might be should the forecast of a “lockbox” shortfall in 2033 come to pass. We’ll get the official word on the 2026 COLA sometime in October, but early estimates are forecasting a 2.5% increase for next year. This potential increase barely matches headline CPI and it falls short of the current Core and Sticky inflation #s.

Social Security’s average monthly benefit among all retired workers is $2,006 in 2025, according to a recent AARP article. If the 2.5% increase turns out to be correct, checks will increase $50 / month. If my math is correct, that equates to an average monthly check of $2,056. The maximum Social Security benefit for a worker retiring at full retirement age is $4,018 in 2025. A 2.5% COLA will bring that figure to $4,118 in 2026. For those retiring at 62-years-old the maximum benefit in 2025 is $2,831, while the maximum benefit for a worker retiring at age 70 is $5,108 in 2025. Those numbers will be adjusted accordingly.

As we celebrate Social Security’s 90th anniversary, we need to understand that the on-going rhetoric about SS running out of money is a fallacy. There DOES NOT exist an “operational constraint on the government’s ability to meet all Social Security payments in a timely manner. It doesn’t matter what the numbers are in the Social Security Trust Fund account, because the trust fund is nothing more than record-keeping, as are all accounts at the Fed.” (Warren Mosler, “Seven Deadly Innocent Frauds of Economic Policy”) He continues, “When it comes time to make Social Security payments, all the government has to do is change numbers up in the beneficiary’s accounts, and then change numbers down in the trust fund accounts to keep track of what it did. If the trust fund number goes negative, so be it. That just reflects the numbers that are changed up as payments to beneficiaries are made.”

What we should fear is that Congress does not understand this concept and acts rashly to address the impending “crisis” that doesn’t exist. Recent estimates target a possible reduction in “benefits” at 23% to 24% in 2033. Try telling the nearly 70 million Americans, many relying on SS for most of their retirement assets, that they will see a dramatic reduction in a promised benefit that they themselves helped to fund. With 50% of retirees using SS for more than 50% of their retirement income and another 25% in which SS makes up 90% or more of their retirement income, the economic impact from these potential benefit cuts would be cruel and absolutely unnecessary.

As we’ve discussed in this blog on many occasions, the U.S. interest rate decline from 1982 to 2022 fueled risk assets well beyond their fundamentals. During the rate decline, investors became accustomed to the US Federal Reserve stepping in when markets and the economy looked dicey. There seems to be a massive expectation that the “Fed” will once again support those same risk assets by initiating another rally through a rate decline perhaps as soon as September. Is that action justified? I think not!

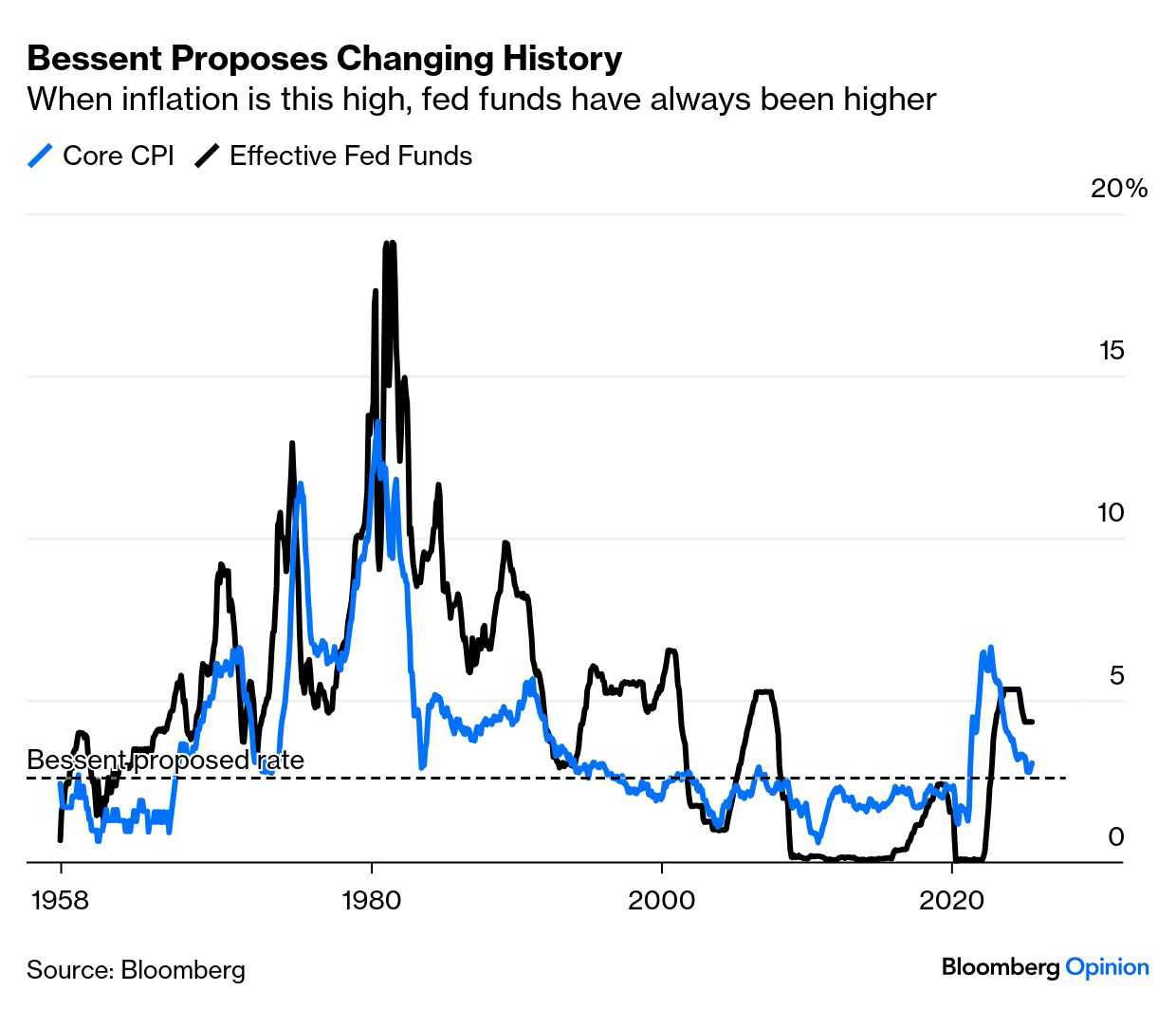

Recent inflation data, including today’s PPI that came in at 0.9% vs. 0.2% expected, should give pause to the crowd screaming for lower rates. Yes, employment #s published last week were very weak, and they got weaker when Erika McEntarfer, the commissioner of the Bureau of Labor Statistics, was fired after releasing a jobs report that angered President Donald Trump. In addition, we have Secretary of the Treasury, Scott Bessent, demanding rates be cut by as much as 150-175 bps, claiming that all forecasting “models” suggest the same direction for rates. Is that true? Again, I think not.

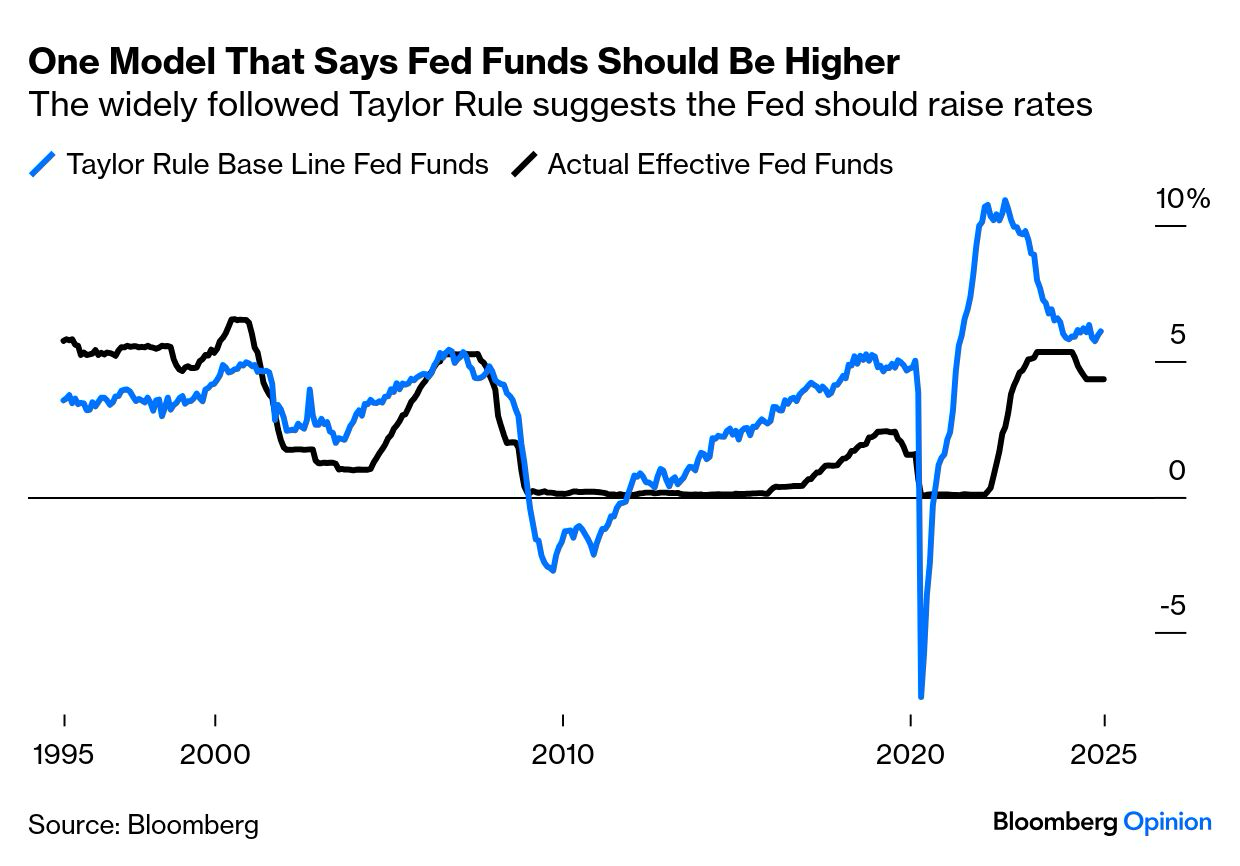

You may recall that I published a blog post on July 10, 2025 titled “Taylor-Made”, in which I wrote that the Taylor Rule is an economic formula that provides guidance on how central banks, such as the Federal Reserve, should set interest rates in response to changes in inflation and economic output. The rule is designed to help stabilize an economy by systematically adjusting the central bank’s key policy rate based on current economic conditions. It is designed to take the “guess work” out of establishing interest rate policy.

In John Authers (Bloomberg) blog post today, he shared the following chart:

Calling for a roughly 2.6% Fed Funds rate in an environment of 3% or more core and sticky inflation is not prudent, and it is not supported by history. Furthermore, the potential impact from tariffs will only begin to be felt as most went into effect as of August 1, 2025.

Getting back to the Taylor Rule, Authers also provided an updated graph suggesting that the Fed Funds rate should be higher today. In fact, it should be at a level about 100 bps above the current 4.3% and more than 270 bps above the level that Bessent desires.

Investors would be wise to exit the lower interest rate train before it fuels a significant increase in U.S. rates as inflation once again rises. The impact of higher rates will negatively impact all risk assets. Given that a Cash Flow Matching (CFM) strategy eliminates interest rate risk through the defeasement of benefits and expenses that are future values and thus not interest rate sensitive, one could bring an element of certainty to this very uncertain economic environment before investors get their comeuppance! Don’t wait for the greater inflation to appear, as it might just be too late at that point to get off the lower interest rate train before it plummets into a ravine.