By: Russ Kamp, CEO, Ryan ALM, Inc.

It is often said that March comes in like a lion and goes out like a lamb. This phrase is typically associated with weather patterns, but it may just be appropriate in describing the PBGC’s effort last week. As you will soon find out, there was a little bit of nearly everything last week.

The good news, Southwestern Pennsylvania and Western Maryland Area Teamsters and Employers Pension Fund, a Priority Group 5 member, received approval for the revised application. They are expected to receive $131.1 million in SFA for their 2,759 members. There have now been 14 of 15 Group 5 members to receive approval. One application needs to be refiled after having been withdrawn some time ago.

In other news, the PBGC’s eFiling portal remained open long enough for U.F.C.W. District Union Local Two and Employers Pension Fund to submit a revised application seeking $125.5 million plus interest for 5,546. This plan had withdrawn its non-priority group application earlier on that day (3/5/25). The PBGC’s note indicates that this application’s review is being expedited, although they have still given themselves the 120-days to complete the review (7/3/25).

In addition to this filing, Local 584 Pension Trust Fund repaid a portion of the SFA as a result of census errors. They returned just over $1 million from the $225.8 million that they received or 0.46%. There have now been 43 plans, from 60 that potentially received excess funds, that have combined to repay $181.9 million from the total of $43.9 billion that was initially paid to these plans. That represents 0.41% of the SFA grants. Furthermore, it only represents 0.26% of the total SFA paid to date ($71.02 billion).

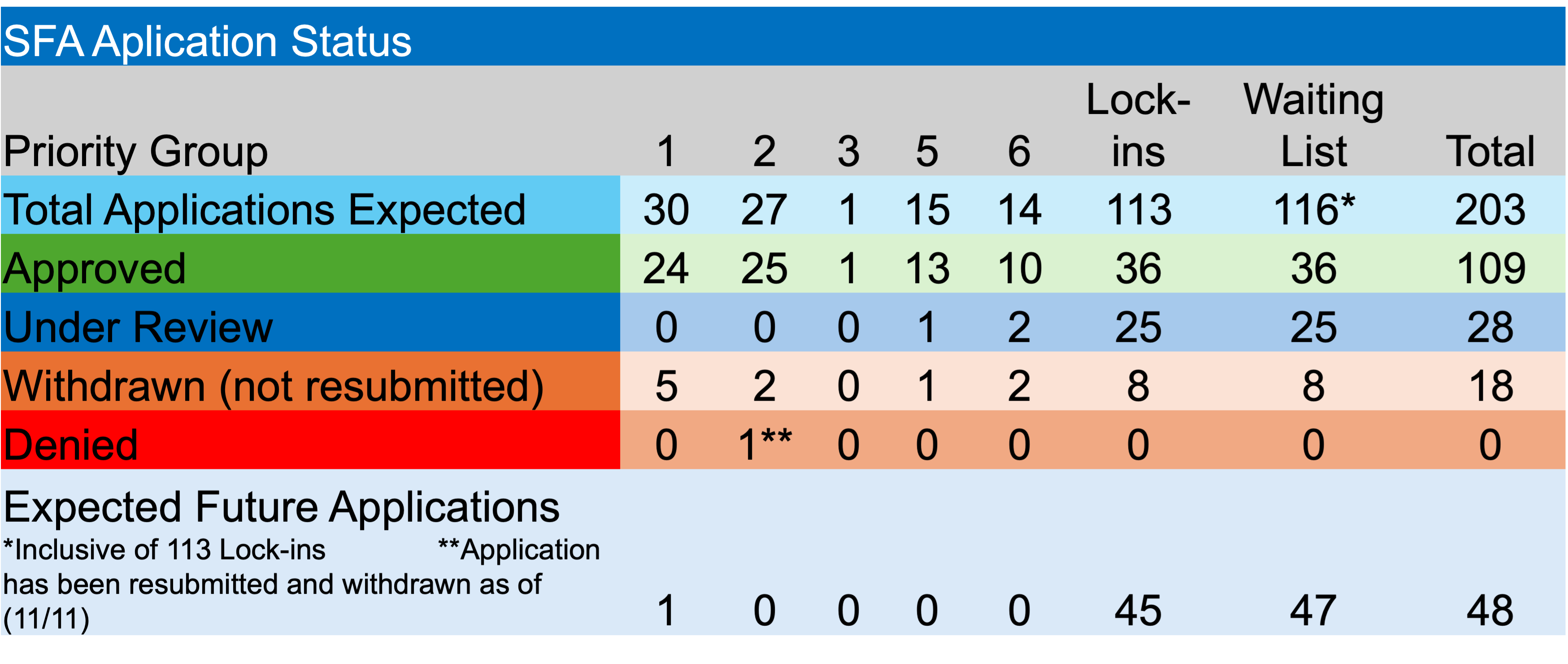

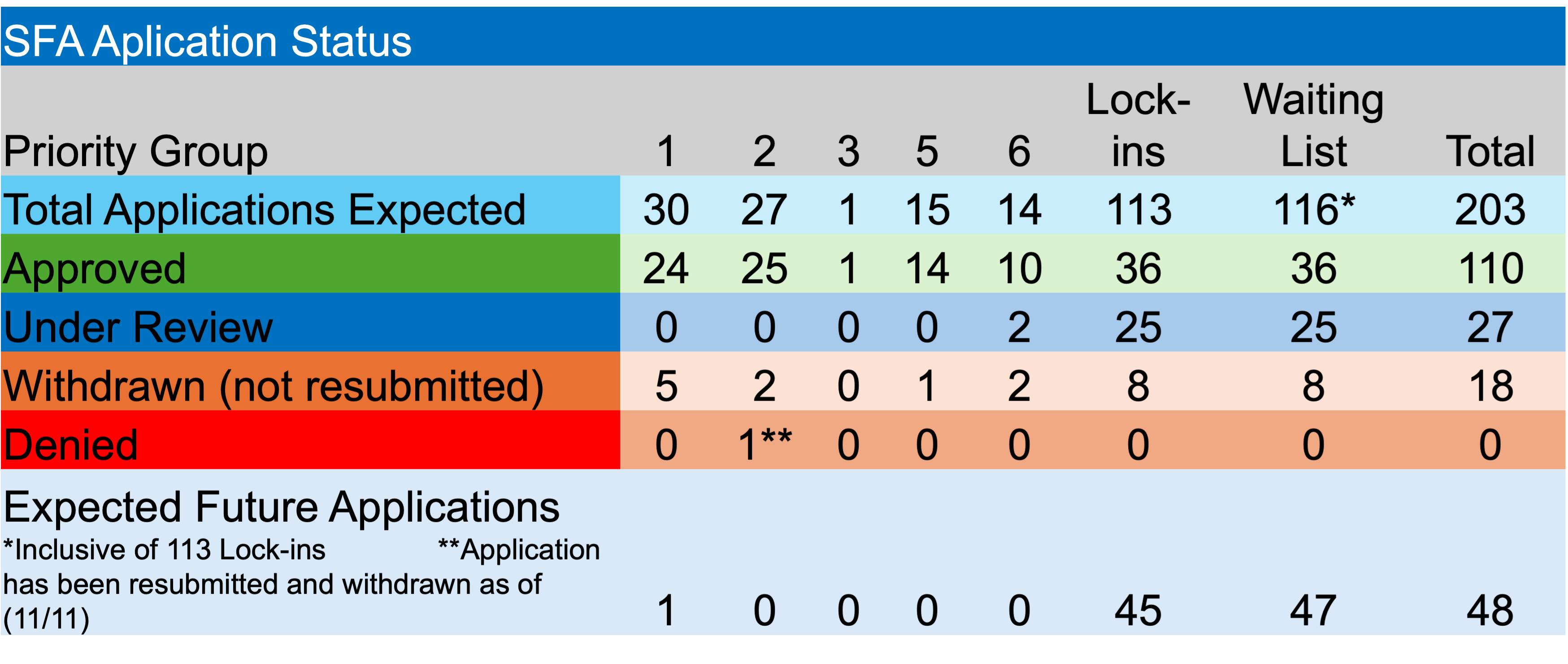

Despite the significant effort to date, the PBGC still has approximately 93 applications to get through, including 48 yet to be submitted. This process needs to be completed by the end of 2026.