We are pleased to share with you a recent white paper produced by Ron Ryan, Ryan ALM’s CEO. In this excellent piece, Ron reminds us of the fallacy that achieving the ROA as an underfunded DB pension system will make everything good – it won’t! As he correctly points out, the funded ratio may remain the same, but the funded status will continue to deteriorate. If the pension plan is 60% funded, at a market value of $100, that system has a funded status deficit of $40. If that 60% funded plan achieves the 7% ROA, assets will grow by $4.20. However, liabilities at that same discount rate will grow at $7. After 5 years, the funded status will have deteriorated by >40% and the deficit will now be >$56.

DB Pension systems that are poorly funded need to work extra hard to keep pace with the growth in the promised benefits or contribute significantly more to close the funding gap. There aren’t many plan sponsors in a position to contribute whatever is necessary to keep the plan in good funded status. Ron also discusses the need for plan sponsors to produce an Asset Exhaustion Test (AET), which is a requirement under GASB 67/68. It is a test of solvency. Ryan ALM modifies the AET to accurately determine the required ROA to fully fund the liability cash flows. Has your actuary produced the AET for your plan? If not, would you like Ryan ALM to calculate the ROA needed to fully fund your plan?

Please don’t hesitate to reach out to us with any questions that you might have regarding this white paper. Also, don’t hesitate to go to RyanALM.com for all the research that we’ve produced throughout the years. We look forward to being a resource for you.

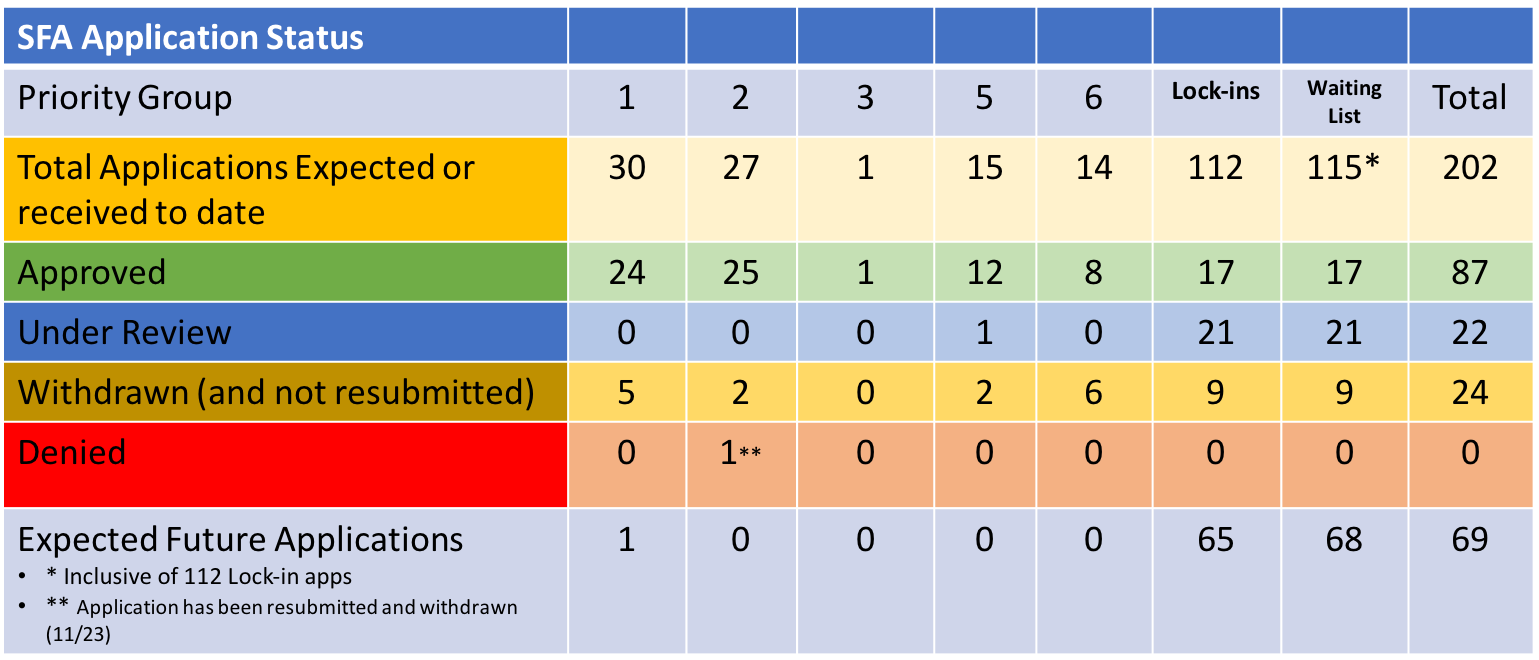

The “dog days” of summer don’t seem to be impacting the activity level at the PBGC, as we had a plethora of activity last week. As mentioned on the PBGC website, the e-filing website is open, but limited. “The e-Filing Portal is open only to plans at the top of the waiting list that have been notified by PBGC that they may submit their applications. Applications from any other plans will not be accepted at this time.” That’s interesting, as there are still 16 pension plans in Priority Groups 1-6 that have potential applications that are not currently being reviewed. Are they excluded, too?

During the week, three funds that had been on the waitlist submitted applications, including, Local 810 Affiliated Pension Plan, the Upstate New York Engineers Pension Fund, and the Alaska Plumbing and Pipefitting Industry Pension Plan. They are seeking a total of $282.1 million for the 9,620 plan participants. This is each plan’s initial submission. As always, the PBGC has 120 from the filing date to conclude the review.

In other news, two plans received approval of their applications, including the Pension Plan of the Moving Picture Machine Operators Union Local 306, a Priority Group 5 member, and the New England Teamsters Pension Plan, that was a Priority Group 6 member. The Moving Picture machinists will receive $20.7 million to support its 542 members, while the NE Teamsters get a whopping $5.7 billion for just over 72k participants. With these latest approvals, the PBGC has now granted through ARPA $67.7 billion in Special Financial Assistance (SFA) that will support the financial futures of 1.34 million American retirees.

On July 23, the Production Workers Pension Plan was added to the waitlist, becoming the 115th member on that list, with 47 having seen some activity (approved, under review, or withdrawn) regarding their applications. In other news, there were no applications denied or withdrawn. Furthermore, none of the previous SFA recipients were asked to repay a portion of the grant due to overpayment. Have a great week, and don’t hesitate to reach out to us if we can provide any assistance to you as you think through your investment strategy as it relates to the SFA grant.

We hope that you enjoyed a wonderful Father’s Day. I’m blessed to still have my Dad with us (95 years young). In addition, I have two sons and two sons-in-law who are wonderful fathers. It was a terrific day!

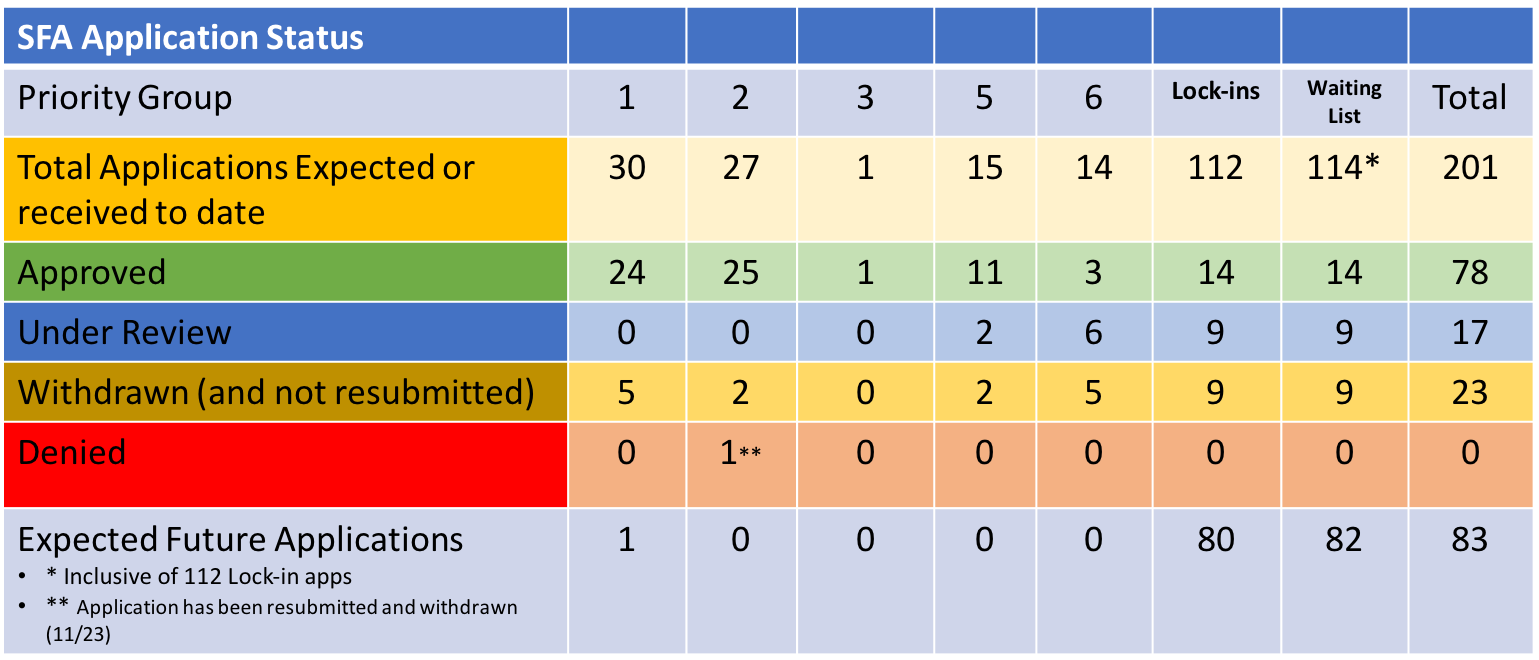

Regarding ARPA and the PBGC’s implementation of that critical pension legislation, there was some activity during the previous week. However, the filing portal remains temporarily closed for those plans still seeking relief through the SFA grants. That said, there are still 17 applications that are currently being reviewed with 6 of those nearing the 120 deadline for action. Those six plans are seeking nearly $5.5 billion in SFA. As a result, the rest of June is going to be busy for the PBGC.

The Pension Plan for the Arizona Bricklayers’ Pension Trust Fund received approval for its application. They will receive $10.7 million to protect the pensions for the 666 members of the plan. This non-priority plan received approval on their initial application. In other news, there were no applications either denied or withdrawn. However, the Graphic Communications Conference of the International Brotherhood of Teamsters National Pension Fund joined Central States as the only other plan to repay excess SFA as a result of a death audit. In this case, they are repaying just over $8 million.

Have a great week. Don’t hesitate to reach out to us if you like to learn more about cash flow matching and how it can be used to extend and protect the SFA grant assets so vital to ensuring that the pension promises are met for your participants.

P&I has produced an article highlighting the fact that money managers recaptured nearly half of the institutional assets lost (-$9 trillion) in 2022’s market correction. They mention that this was accomplished despite “lingering economic and political uncertainties that kept a lot of money sidelined, including a record $6 trillion parked in money market funds alone.”

According to Pensions & Investments’ 2023 survey of the largest money managers, institutional assets for 411 managers around the globe rose 9.7%, or $4.89 trillion, to $55.23 trillion as of Dec. 31, 2023 for a recovery rate of 52.5%. This recapture of assets was primarily driven by equities, both US (+26%) and global X US (+18%), while bonds were up 5.6% domestically and abroad.

Obviously, it was great to see the “rally” despite wide-spread uncertainty related to the economy, inflation, interest rates, and the labor market. Issues that are still impacting perceptions today. But the real question one should ask has to do with the cyclical nature of markets and what plan sponsors and their advisors can do to mitigate the peaks and valleys. As I reported earlier this week, since 2000, public pension plans have seen a tripling (or more) in contribution expenses as a % of pay, while the funded status of Piscataqua research’s universe of 127 state and local plans has fallen by 25%.

Isn’t it time to get off the asset allocation rollercoaster? The nearly singular focus on return (ROA) by pension plan sponsors has placed pension funding on a ride that does little to guarantee success, but has certainly exacerbated volatility. In the process, contributions into these critically important retirement systems have skyrocketed. Let’s stop thinking that the only way to fund pensions is through outsized market returns. Today’s interest rate environment is providing plan sponsors with a wonderful opportunity to SECURE a portion of their future promises by carefully constructing a defeased bond portfolio that matches and funds asset cash flows of principal and interest with liability cash flows of benefits and expenses.

By doing so, you eliminate the impact of drawdowns, as the assets and liabilities will now move in tandem. How refreshing! Because you are defeasing a future benefit, you are also eliminating interest rate risk, as future values are not interest rate sensitive. Furthermore, you have now created a liquidity profile that is enhanced, as the bond portfolio now pays all of the benefits and expenses chronologically as far into the future as the allocation to the cash flow matching program lasts. Lastly, the growth or alpha assets can now grow unencumbered, as they are no longer a source of funding. The need for a cash sweep has been replaced by cash flow matching with bonds.

Let’s stop having to celebrate recovery rates of roughly 50%, when we can institute investment programs that eliminate these massive and harmful drawdowns. They aren’t helpful to the sustainability of DB pension plans, which we so desperately need if we are to provide a dignified retirement to the American worker. Let’s get back to the fundamentals, as the true objective of a pension is to fund benefits in a cost-efficient manner with prudent risk. It isn’t a performance arms race!

The following was a headline for a MarketWatch.com article, “The 401(k)’s success has been overlooked and will help even more Americans”, which I saw on a LinkedIn.com post earlier today. Sure, some American workers have benefited from their ability to fund a DC account, but the vast majority of Americans are struggling.

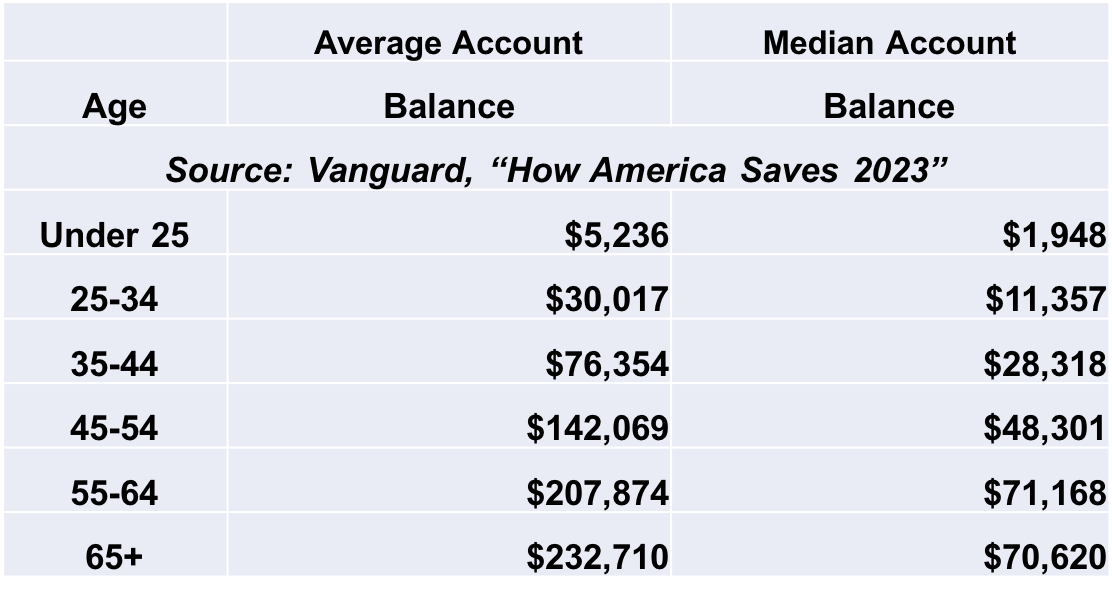

Does This look like success?

Perhaps the level of savings would be okay if DC plans were actually supplemental retirement vehicles, but since they have morphed into the primary retirement program for most workers, this is a disaster. I’m tired of the fact that we only ever see “average” balances reported. Of course, a few well-funded balances will drive the average up. Let’s focus on the MEDIAN account balances. Does a $70,620 account balance for a 65+ year-old participant look like a successful outcome? How much would that balance provide on a monthly basis for a roughly 20-year retirement?

If I were fortunate to have a defined benefit plan that provided $2,000/month (which isn’t a lot) for 20-years, I would receive $480K in retirement which is 6.8Xs what the 65+ year-old with the median account balance has today. It is a far cry when compared to the view that $1.4 million is the balance needed to have a dignified retirement today. It is silly to believe that the average American has the disposable income, investment acumen, and predictive ability to gauge how long they will live in order to allocate this meager balance to ensure that the recipient doesn’t outlive their savings.

The investment industry can celebrate all they want as it relates to the total accumulated wealth in defined contribution plans, but for the “median” American, it just isn’t close to being enough. Defined benefit plans should be the backbone of our retirement system, while DC plans occupy the supplemental role for which they were designed. As someone in that LinkedIn.com post stated, “the numbers don’t lie”. I would certainly agree, but that doesn’t mean that the #s are revealing success!

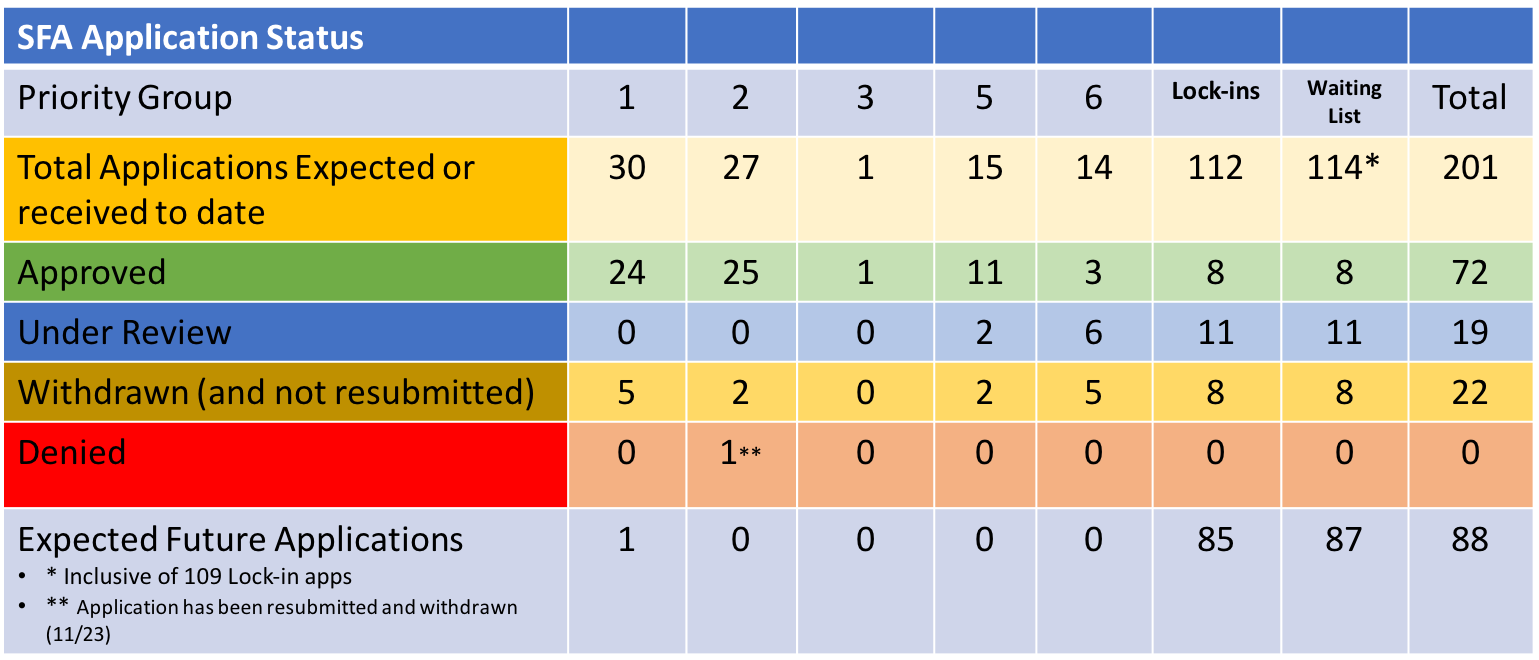

Another Monday brings the weekly update on the PBGC’s effort to implement the pension rescue under ARPA. As noted previously, activity has definitely slowed in recent weeks, and the week ending May 10, 2024 is no exception. I can report that the only activity on the PBGC’s ARPA spreadsheet is a withdrawal of a previously revised application. Employers’ – Warehousemen’s Pension Plan, a non-priority plan out of Los Angeles, was seeking $40 million in Special Financial Assistance (SFA) for just over 1,800 plan participants. The latest version of the application had been filed on March 4, 2024.

Unfortunately, there were no additional applications submitted or approved. At the same time, there were no additional applications withdrawn or denied. Lastly, no plans that might have received excess SFA have returned those excess assets at this tie outside of Central States. There remain 129 plans to still have their applications for SFA reviewed and approved.

Glen Eagle Trading reported the following in a recent email, that In 2023, a survey found that 78% of Americans live paycheck-to-paycheck, up six percentage points from the previous year. Unfortunately, in yet another survey 29% of Americans don’t earn enough to cover basic living costs. The ability to fund a retirement is getting to be more challenging than ever, which is why DB pension systems need to be be protected and preserved. The ARPA pension legislation is going a long way to securing pensions for millions of American workers who were on the verge of losing most, if not everything, that they had earned and counted on for their “golden years”.

P&I produced an article yesterday titled, “Corporate Pension Funds Are Fully Funded, Healthier Than Ever. Now What?” According to Milliman, corporate pension plans are averaging roughly a funded ratio of 106%. This represents a healthy funded status, but it is by no means the healthiest ever. One may recall that corporate plans were funded in excess of 120% as recently as 2000. In what might be more shocking news, public pension plans were too when using a market discount rate (ASC 715 discount rate). Today, those public pension plans have a funded status of roughly 80% according to Milliman’s latest public fund report.

The question, “Now what”? is absolutely the right question to be asking. Many corporate plans have already begun de-risking, as the average exposure to fixed income is >45% according to P&I’s asset allocation survey through November 2023. Unfortunately, public pension systems still sit with only about 18% exposure to US fixed income, preferring a “let it ride” mentality as equities and alternatives account for more than 75% of the average plan’s asset allocation. Is this the right move? No. The move into alternatives has dried up liquidity, increased fees, and reduced transparency. Furthermore, just because a public plan believes that its sponsor is perpetual, does that make the system sustainable? You may want to be reminded about Jacksonville Police and Fire. There are other examples, too.

Whether the pension plan is corporate, multiemployer, or public, the asset allocation should reflect the funded status. There is no reason that a 60% funded plan should have the same asset allocation as one that is 90% or better funded. All plans should have both liquidity and growth buckets. The liquidity bucket will be a bond allocation (investment grade corporates in our case) that matches asset cash flows to liability cash flows of benefits and expenses. That bucket will provide all of the necessary liquidity as far into the future as the pension system can afford. The remaining assets will be focused on outperforming future liability growth. These assets will be non-bonds that now have the benefit of an extended investing horizon to grow unencumbered. Forcing liquidity in environments in which natural liquidity has been compromised only serves to exacerbate the downward spiral.

Pension America has the opportunity to stabilize the funded status and contribution expenses. They also have the chance to SECURE a portion of the promises. How comforting! We saw this movie a little more than 20 years ago. Are we going to treat this opportunity as a Ground Hog Day event and do nothing or are we going to be thoughtful in taking appropriate measures to reduce risk before the markets bludgeon the funded status? The time to act is now. Not after the fact.

Milliman recently released results for its Public Pension Funding Index (PPFI), which covers the nation’s 100 largest public defined benefit plans.

Positive equity market performance in March increased the Milliman 100 PPFI funded ratio from 78.6% at the end of February to 79.7% as of March 31, representing the highest level since March 31, 2022, prior to the Fed’s aggressive rate increases. The previous high-water mark stood at 82.7%. The improved funding for Milliman’s PPFI plans was driven by an estimated 1.7% aggregate return for March 2024. Total fund performance for these 100 public plans ranged from an estimated 0.9% to 2.6% for the month. As a result of the relatively strong performance, PPFI plans gained approximately $85 billion in MV in March. The asset growth was offset by negative cash flow amounting to about $9 billion. It is estimated that the current asset shortfall relative to accrued liabilities is about $1.271 trillion as of March 31.

In addition, it was reported that an additional 4 of the PPFI members had achieved a 90% or better funded status, while regrettably, 15 of the constituents remain at <60%. Given that changing US interest rates do not impact the calculation for pension liabilities under GASB accounting, the improvement in March’s collective funded status may be underreported, as US rates continued the upward trajectory begun as the calendar turned to 2024.

Managing a pension plan should be all about securing the promised benefits at a reasonable cost and with prudent risk. I believe that most plan sponsors would agree, yet that is not how plans are managed, especially public and multiemployer plans that continue to pursue the return on asset assumption (ROA) as if it were the Holy Grail. I’ve written quite a bit on this subject, including discussing asset consulting reports that should have the relationship of plan assets to plan liabilities on page one of the quarterly performance reports.

We know that pension liabilities are like snowflakes, as there are no two pension liability streams that are the same given the unique characteristics of each labor force. Furthermore, most pension actuaries only produce an annual update making more frequent (monthly/quarterly) updates more challenging. Would plan sponsors want a more frequent view of the liabilities if they were available? I think that they would. Again, if securing the promised benefits are the primary objective when it comes to managing a pension plan, then plan sponsors need a more frequent view of the relationship between assets and liabilities.

Why is this important? First and foremost, the capital markets are constantly moving, and the changes impact the value of the plan’s assets all the time. But it isn’t just the asset-side that is being impacted, as liabilities are bond-like in nature and they change as interest rates change. We’ve highlighted this activity in both the Ryan ALM Pension Monitor and the Ryan ALM Quarterly Newsletter. However, accounting rules for both multiemployer and public plans allow a static discount rate equivalent to the plan’s ROA to be used that hides the impact of those changing interest rates on the value of a plan’s liabilities and funded status.

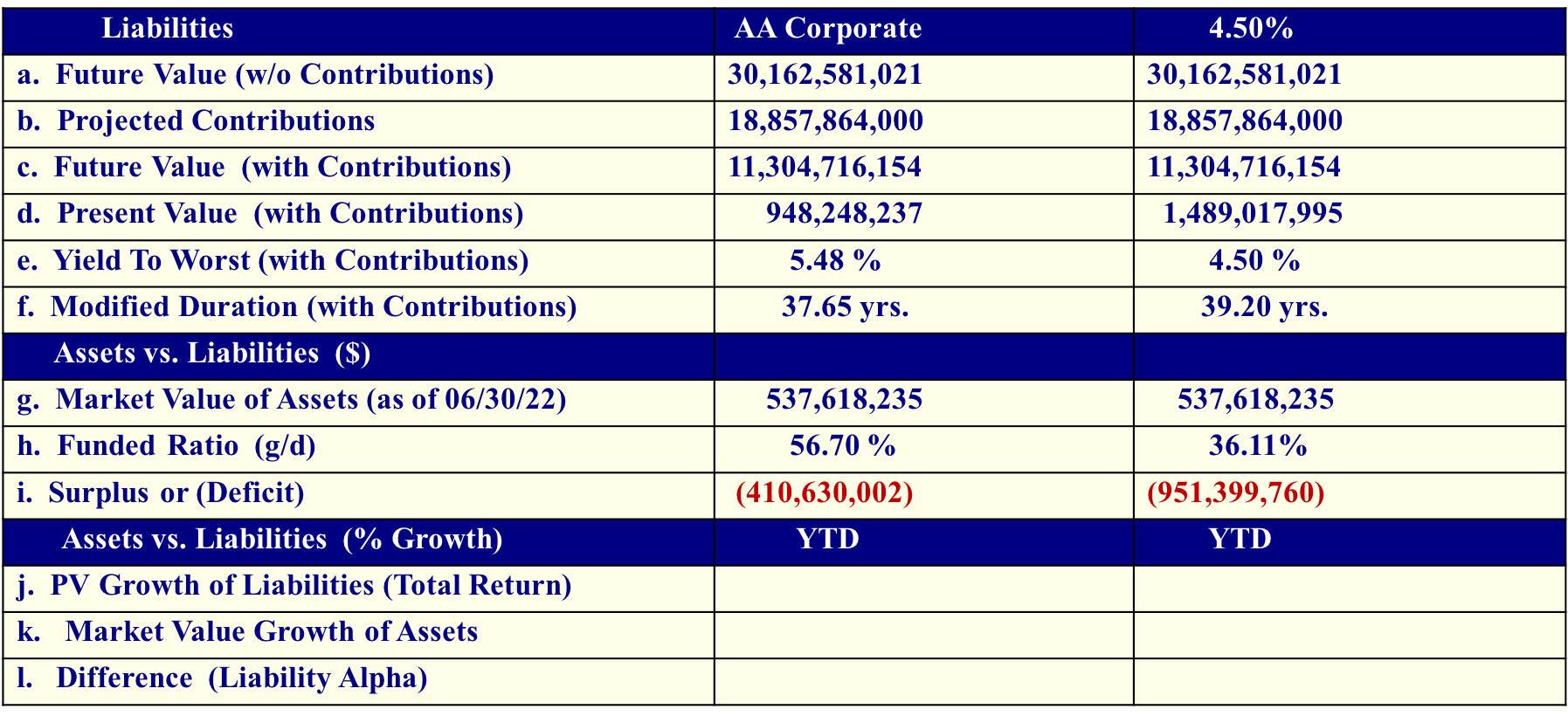

What if a more frequent analysis was available at a modest cost. Would plan sponsors want to see how the funded status was behaving? Would they want that comparison available to help with asset allocation changes, especially if it meant reducing risk as funding improved? I suspect that they would. Well, there is good news. Ryan ALM, Inc. created a Custom Liability Index (CLI) in 1991. The CLI is designed to be the proper benchmark for liability driven objectives. The CLI calculates the present value of liabilities based on numerous discount rates (ASC 715 (FAS 158), PPA – MAP 21, PPA – Spot Rates, GASB 67, Treasury STRIPS and the ROA). The CLI calculates the growth rate, summary statistics, and interest rate sensitivity as a series of monthly or quarterly reports depending on the client’s desired frequency.

The above information is for an actual client, who we’ve been providing a CLI for 15+ years. This client has elected to receive quarterly reviews. They’ve also chosen to see the impact on liabilities for multiple discount rates, including a constant 4.5% ROA, which could easily be a pension plan’s ROA of say 7%. As you will note, the present value (PV) of those future value (FV) liabilities are different, and they could be dramatic, depending on the interest rate used. In this case, the AA Corporate rate (5.48% YTW) produces a funded ratio of 56.7%, while the flat 4.5% rate increases the PV liabilities thus reducing the funded status by more than 20%.

Using Treasury STRIPS as the discount rate produces the lowest funded ratio of 33.7% or 23% lower than using the AA Corporate discount rate.

With this information, plan sponsors and their advisors (consultants and actuaries) can make informed decisions related to contributions and asset allocation. Most plan sponsors are currently blind to these facts. As a result, decisions may be taken without having all of the necessary facts. Pension plans need to be protected and preserved (Ryan ALM’s mission). Having a complete understanding of what those future promises look like is essential.

You’ve made a promise: measure it – monitor it – manage it – and SECURE it…

Get off the pension funding rollercoaster – sleep well!

Milliman released the results of its latest Milliman 100 Pension Funding Index (PFI), which analyzes the 100 largest U.S. corporate pension plans. Pension funding improved for the third consecutive month to start the year, which now stands at 105.6% from 105.3% at the end of February. March was a bit different, however, as the discount rate declined 11 basis points increasing the collective liabilities by $14 billion to $1.299 trillion at the end of the quarter. Despite the increase in liabilities, investment performance was once again strong leading to a gain of $19 billion. Total assets now stand at $1.373 trillion.

Zorast Wadia, author of the PFI, stated, “the funded status gains may dissipate unless plan sponsors adhere to liability-matching investment strategies. Zorast’s observation is outstanding. Should rates fall from these levels, the cost to defease pension liabilities will grow. Now is the time to take risk off the table. Create certainty by getting off the asset allocation rollercoaster. Engaging in Cash Flow Matching (CFM) does not necessitate being an all or nothing strategy. Start your cash flow matching mandate and extend it as the funded status improves.

Return-seeking bond strategies will lose in an environment of rising rates. However, once a plan engages in CFM, the relationship between plan assets and liabilities is locked. Done correctly, assets and liabilities will move in tandem. It doesn’t matter what interest rates do, as benefit payments are future values that are not interest rate sensitive.

Act now to create some certainty! You’ll appreciate the great night’s sleep that you’ll start to have.