By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Most of us seek to climb the “ladder to success”. We also use ladders for important everyday activities. I’ll soon be back on a ladder myself, as year-end approaches and the Christmas lights are placed on my home. Despite the usefulness of ladders, there is one place where they aren’t necessarily beneficial. I’m specifically addressing the use of ladders for bond management as a replacement for a defeasement strategy.

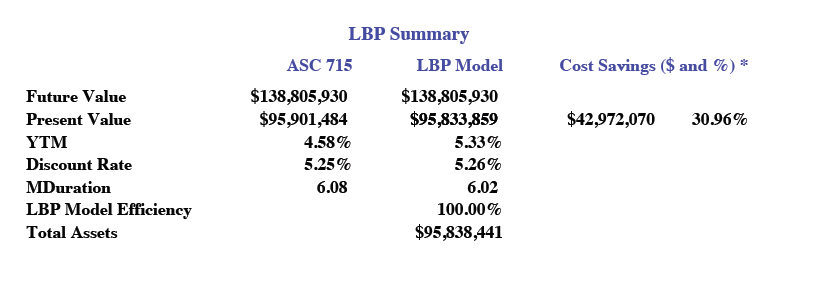

There are still so many misconceptions regarding Cash Flow Matching (CFM). Importantly, CFM is NOT a “laddered bond portfolio”, which would be quite inefficient and costly. It IS a highly sophisticated cost optimization process that maximizes cost savings by emphasizing longer maturity bonds (within the program’s parameters capped at the maximum year to be defeased) and higher yielding corporate bonds, such as A and BBB+.

Furthermore, it is not just a viable strategy for private pension plans, as it has been deployed successfully in public and multiemployer plans for decades, as well as E&Fs. It is also NOT an all or nothing strategy. The exposure to CFM is a function of several factors, including the plan’s funded status, current allocation to core fixed income, and the Retired Lives Liability, etc. Many of our clients have chosen to defease their pension liabilities from 5-30 years or beyond. When asked, we recommend a minimum of 10 years, but again that will be a function of each plan’s unique funding situation.

CFM strategies are NOT “buy and hold” programs. CFM implementations must be dynamic and responsive to changes in the actuary’s forecasts of benefits, expenses, and contributions. There are also continuous changes in the fixed income environment (I.e. yields, spreads, credits) that might provide additional cost savings that need to be monitored and managed. Plan sponsors may seek to extend the initial length (years) of the program as it matures which will often necessitate a restructuring or rebalancing of the original portfolio to maximize potential funding coverage and cost reductions.

CFM programs CANNOT be managed against a generic index, as no pension plan’s liabilities will look like the BB Aggregate or any other generic index. Importantly, no pension plan’s liabilities will look like another pension plan given the unique characteristics of that plan’s workforce and plan provisions. The appropriate management of CFM requires the construction of a Custom Liability Index (CLI) that maps the plan’s liabilities in multiple dimensions and creates the path forward for the successful implementation of the asset/liability match.

Importantly, CFM programs are NOT going to negatively impact the plan’s ability to achieve its desired ROA. In fact, a successful CFM program, such as the one we produce, will actually enhance the probability of achieving the return target. How? Your plan likely has an allocation to core fixed income. Our implementation will likely outyield that portfolio over time creating alpha as well as SECURING the promised benefits. Given the higher corporate bond interest rates, an allocation to this asset class can generate a significant percentage of the ROA target with risks substantially below those of other asset classes.

When done right, a successful CFM implementation achieves the following:

Provides liquidity to meet benefits and expenses

Secures benefits for the time horizon the CFM portfolio is funding (1-10 years +)

Buys time for the alpha assets to grow unencumbered

Out yields active bond management… enhances ROA

Reduces Volatility of Funded Ratio/Status

Reduces Volatility of Contribution costs

Reduces Funding costs (roughly 2% per year in this rate environment)

Mitigates Interest Rate Risk for that portion of the portfolio using CFM as benefits are future values that are not interest rate sensitive.

No laddered bond portfolio can provide the benefits listed above. Whether you are responsible for a DB pension, an endowment or foundation, a HNW individual, or any other pool of assets, you likely have liquidity needs regularly. CFM done right will greatly enhance this process. Call on us. We’ll gladly provide an initial analysis on what can be achieved, and we will do it for FREE.