We are happy to share with you the latest thinking from Ron Ryan. Ron has written a very interesting article on the “smartest beta“. There is beta, a term coined by Bill Sharpe. Smart beta, which is the optimization of the risk/reward behavior of a market index usually by changing the weights of the index’s constituents. Then there is the smartest beta. The “smartest beta” portfolio, as described by Ron, is the portfolio that best matches and achieves the true client objective of funding liabilities with the least amount of risk and cost.

Risk is best measured as the “uncertainty of achieving the objective”. Cost is the amount required to fund the objective. The true objective of most institutions and even individuals is some type of liability (annuities, banks, insurance, lotteries, NDT, pensions, OPEB, etc.). The absolute level of volatility of returns is not risk given a liability objective.

Please don’t hesitate to reach out to us if you’d like to explore the concept of the “smartest beta” in greater detail. We’d welcome that opportunity.

Congratulations to Ron Ryan, a true visionary, and the Ryan ALM, Inc. team as they (we) celebrate the 20th anniversary of the firm. Ryan ALM was incorporated in Delaware on June 15, 2004. Ronald J, Ryan, founder, says that “we created our company to be dedicated to asset liability management (ALM) as our name suggests. We are quite proud of our progress and achievements in ALM. We have built a turnkey system of products that are quite unique in the ALM industry”.

We strive every day to protect and preserve defined benefit plans for the American worker. We continue to believe that the primary objective in managing a pension is to SECURE the promised benefits at low cost and with prudent risk. We thank all of our clients and their advisors who have provided us with the opportunity to support their efforts on a daily basis. Please don’t hesitate to reach out to us. We’ll work with you to find a unique solution to your specific issue(s).

Milliman is reporting improvement in the funded status for the largest corporate plans. According to the Milliman 100 Pension Funding Index (PFI), corporate funding improved from 103.1% to 103.4% during May, marking the fifth consecutive monthly improvement to start 2024. Milliman attributed the improved funding to asset gains driven by the year’s best month at 2.29% driving the indexes assets up by $22 billion to $1.3 trillion. With the decline in the discount rate of 15 bps, pension liabilities grew by $18 billion and now stand at $1.25 trillion. According to Zorast Wadia, the discount rate used by Milliman is the FTSE Pension Liability Index, which is similar to ASC 715 rates. As a reminder, Ryan ALM, Inc. has produced ASC 715 rates since 2007. The $4 billion difference between pension assets and plan liabilities produced the 0.3% funding improvement.

Milliman’s monthly reporting also includes scenario testing. In the latest work, Milliman forecasts 2024 and 2025 interest rates and asset returns. In the optimistic case they forecast the discount rate at 5.88% at the end of 2024 and 6.48% at the end of 2025, while assets grow at 10.4% per annum during that time. If achieved, the funded status for the Pension Funding Index would ratchet up to 110% at the end of 2024 and 123% by 2025’s conclusion. These levels would rival what we had at the end of 1999, when Pension America should have defeased the liabilities.

A pessimistic forecast has the discount rate falling to 5.18% by the end of 2024 and 4.58% by December 31, 2025. Assets under this scenario produce only a 2.4% annualized return. If this forecast were to become reality, the PFI funded status would be 98% by the end of 2024 and 89% by the end of 2025. Since most of us have no clue where rates are going in the next couple of years, why play the game. Defease your plan’s liabilities at the current level of rates. We’ve seen too often greed creep into the equation instead of sound risk management. Use this opportunity to substantially reduce risk by matching and funding benefits and expenses with asset cash flows of interest and principal.

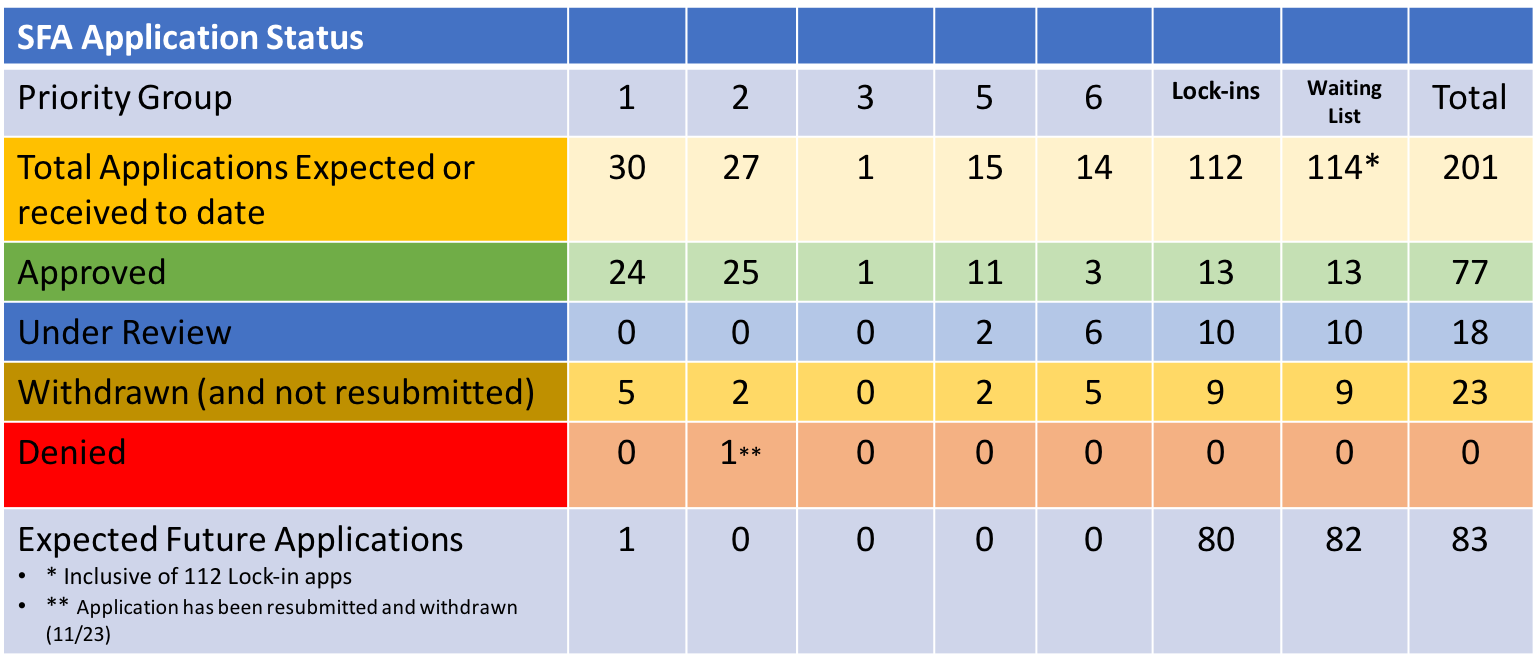

We are pleased to provide you with another ARPA update. The PBGC approved the applications for two New Jersey funds seeking Special Financial Assistance (SFA). CWA/ITU Negotiated Pension Plan and the Pension Plan of Local 102, both non-priority funds, will receive $545.6 million and $12.5 million, respectively, in order to ensure that their 24,796 participants will receive the promised benefits.

Unfortunately, there isn’t much else to report, as there were no new applications submitted, and the queue remains at 18. There were no applications rejected or withdrawn and no pension systems were added to the waitlist, with 32 of 114 having had some activity (submissions, withdrawals, and approvals) to date. Central States remains the only plan to pay back excess SFA proceeds.

The 18 plans that are currently under review carry some heft, as they are collectively seeking >$13 billion in SFA for nearly 370K participants. Seven of those plans have application “deadlines” in June. As a reminder, the PBGC has 120 days to act on an application once it has been submitted. Fortunately, US interest rates remain elevated providing plan sponsors with the opportunity to use cash flow matching to secure the SFA assets and significantly reduce the risk associated with a traditional asset allocation. Sponsors would be wise to use the legacy assets to assume a more traditional asset allocation since those assets now have the benefit of an extended investing horizon.

P&I has produced an article highlighting the fact that money managers recaptured nearly half of the institutional assets lost (-$9 trillion) in 2022’s market correction. They mention that this was accomplished despite “lingering economic and political uncertainties that kept a lot of money sidelined, including a record $6 trillion parked in money market funds alone.”

According to Pensions & Investments’ 2023 survey of the largest money managers, institutional assets for 411 managers around the globe rose 9.7%, or $4.89 trillion, to $55.23 trillion as of Dec. 31, 2023 for a recovery rate of 52.5%. This recapture of assets was primarily driven by equities, both US (+26%) and global X US (+18%), while bonds were up 5.6% domestically and abroad.

Obviously, it was great to see the “rally” despite wide-spread uncertainty related to the economy, inflation, interest rates, and the labor market. Issues that are still impacting perceptions today. But the real question one should ask has to do with the cyclical nature of markets and what plan sponsors and their advisors can do to mitigate the peaks and valleys. As I reported earlier this week, since 2000, public pension plans have seen a tripling (or more) in contribution expenses as a % of pay, while the funded status of Piscataqua research’s universe of 127 state and local plans has fallen by 25%.

Isn’t it time to get off the asset allocation rollercoaster? The nearly singular focus on return (ROA) by pension plan sponsors has placed pension funding on a ride that does little to guarantee success, but has certainly exacerbated volatility. In the process, contributions into these critically important retirement systems have skyrocketed. Let’s stop thinking that the only way to fund pensions is through outsized market returns. Today’s interest rate environment is providing plan sponsors with a wonderful opportunity to SECURE a portion of their future promises by carefully constructing a defeased bond portfolio that matches and funds asset cash flows of principal and interest with liability cash flows of benefits and expenses.

By doing so, you eliminate the impact of drawdowns, as the assets and liabilities will now move in tandem. How refreshing! Because you are defeasing a future benefit, you are also eliminating interest rate risk, as future values are not interest rate sensitive. Furthermore, you have now created a liquidity profile that is enhanced, as the bond portfolio now pays all of the benefits and expenses chronologically as far into the future as the allocation to the cash flow matching program lasts. Lastly, the growth or alpha assets can now grow unencumbered, as they are no longer a source of funding. The need for a cash sweep has been replaced by cash flow matching with bonds.

Let’s stop having to celebrate recovery rates of roughly 50%, when we can institute investment programs that eliminate these massive and harmful drawdowns. They aren’t helpful to the sustainability of DB pension plans, which we so desperately need if we are to provide a dignified retirement to the American worker. Let’s get back to the fundamentals, as the true objective of a pension is to fund benefits in a cost-efficient manner with prudent risk. It isn’t a performance arms race!

Anyone who has read just a handful of the >1,400 blog posts that I’ve produced knows that I am a huge fan of defined benefit (DB) plans. That I’ve come to loathe the fact that DB plans were/are viewed as dinosaurs, and as a result have been mostly replaced by ineffective defined contribution plans. As a result, the American worker is less well-off given the greater uncertainty of their funding outcome. A dignified retirement is getting further out of reach for a majority of today’s workers.

That said, just because I desire to see DB plans maintained as the primary retirement vehicle, doesn’t mean that I appreciate how many of them have been managed. The pension plan asset allocations remain focused on the wrong objective, which continues to be the ROA and NOT the plan’s liabilities. It is this mismatch in the primary objective that has exacerbated the volatility of the funded ratio/status and contribution expenses. As I’ve stated many times, it is time to get off the asset allocation rollercoaster. We need to bring an element of certainty to the investment structure despite the fact that outcomes within the capital markets are highly uncertain.

How bad have things been? According to a recently produced analysis by Piscataqua Research, Inc., which regularly reviews the performance of both assets and liabilities for 127 state and local retirement systems, since 2000 contributions as a % of pay have tripled, while funded status has declined by more than 25%. Again, I’m not here to bash public funds. On the contrary, I am here to offer a potential solution to the volatility exhibited. I wrote a piece many years (1/17) ago titled, “Perpetual Doesn’t Mean Sustainable” in which I discussed the need to bring stability to these critically important retirement plans because at some point there might just be a revolt from the taxpayers that are lacking defined benefit participation themselves. We can’t afford to have tens of millions of American public fund workers added to the federal social safety net God forbid their retirement plans are terminated and benefits frozen prematurely.

There is only one asset class – bonds – in which the future performance is known on the day that the bond is acquired. You can’t tell me what Amazon or Tesla will be worth in 10 years or the value of a building or private equity portfolio, but I can tell you how much interest and principal you will have earned on the day that the bond matures, whether that be 3-, 5-, 10- or 30-years from now. That information is incredibly valuable and can be used to match and SECURE the pension plan’s liabilities. That portion of the plan’s assets will now provide stability and certainty reducing the ups and downs exhibited through normal market behavior. Why continue to embrace an asset allocation that has NO certainty? An asset allocation that can create the explosion in contribution expenses that we’ve witnessed.

DB plans need to be protected and preserved! Ryan ALM’s focus is solely on achieving that lofty goal. It should be your goal, too. Let us help you get off the asset allocation rollercoaster before markets reach their peak and we once again ride those market down creating a funding deficit that will take years and major contributions to overcome.

Kudos to Ed McCarthy who wrote a terrific article for PlanSponsor that addressed alternative strategies to Pension Risk Transfers (PRTs) that have been so prevalent in recent years. The article featured comments from Zorast Wadia, Principal and Consulting Actuary, Milliman, the Center for Retirement Research at Boston College, and me. Not surprisingly, I address asset/liability management (ALM) strategies, with a particular focus on Cash Flow Matching (CFM). The hope is that DB plan sponsors will seek alternatives to the PRT trend that will protect and preserve these critically important retirement vehicles for the American worker.

Please don’t hesitate to reach out to me if I can be of any assistance or respond to any questions that you might have regarding ALM in general or CFM specifically.

Welcome to June and the latest update on the PBGC’s effort to implement the ARPA pension legislation. There isn’t much to report, but I’m happy to mention that two plans received approval of the SFA applications.

Maryland Race Track Employees Pension Plan and the Radio, Television and Recording Arts Pension Plan were granted approval for SFA totaling $89.6 million. Both plans were categorized as non-priority funds. In the case of the Maryland Race Trace Employees, they are galloping toward receiving $26.7 million for the 1,407 plan participants, while the Radio, Television and Recording Arts will no longer have to perform for their benefits as they will get $62.8 million for the plan’s 516 participants or roughly $121 K per participant.

The only other reported activity had the Carpenters Pension Trust Fund – Detroit & Vicinity pulling its application that was seeking $595.5 for more than 22,000 members of the plan. This non-priority plan from Troy, MI, pulled its initial application. There were no new applications filed or rejected. No plans were added to the waitlist and no pension funds returned excess SFA assets.

June looks to be shaping up as a busy month for the PBGC, as there are nine funds that have approval dates this month, including the Bakery and Confectionery Union and Industry International Pension Fund, that is seeking nearly $3.2 billion in SFA. In total, the nine funds are hoping to gather more than $6 billion in grants for 233,845 participants. Six of the nine funds are waiting to get approval from the PBGC on revised applications. Good luck.

We are pleased to share with you the latest research from Ron Ryan, who provides a unique perspective on asset allocation and the important role that Cash Flow Matching (CFM) can play in helping plan sponsors achieve the elusive ROA. How would you like another 50 bps with little risk? Using CFM to defease pension liabilities through a corporate bond exposure (primarily A/BBB+) could enhance the fixed income return versus the Aggregate Index that is heavily skewed to lower yielding government securities. In addition to the enhanced return, the CFM strategy provides the necessary liquidity to meet ongoing benefits and expenses.

We are acknowledged experts in Cash Flow Matching. We regularly provide a free analysis on what a CFM strategy could do for you and your plan as it relates to the critically important management of assets/liabilities. Don’t hesitate to reach out to us. We look forward to being a resource for you.

I continue to be surprised by the constant droning that US interest rates are too high and financial conditions are too tight. Compared to what? If the reference point is Covid-19 induced levels then you are probably right, but if the comparison is to almost any other timeframe then those proclaiming that the sky is about to fall should refer to one of the greatest decades for equities in my lifetime – the 1990s. I think most investors would agree that the 1990s provided a nearly unprecedented investing environment. One in which the S&P 500 produced an 18.02% annualized performance.

Was the economic environment of the 1990s so much better than today’s? Heck no, but let’s take a closer look. The average 10-year Treasury note yield was 6.52% ranging from a peak of 8.06% at the end of 1990 to a low of 4.65% in 1998. Given that the current yield for the US 10-year Treasury note is 4.56%, I’d suggest that the present environment isn’t too constraining. Furthermore, let’s look at the employment picture from the ’90s. If US rates aren’t high by 1990 standards, unemployment must have been very low. You’d be wrong if that was your guess. In fact, unemployment in the US ranged from 7.5% at the end of 1992 to a low of 4.2% in 1999. For the decade, we had to deal with an average of 5.75% unemployment. Today, we sit with a 3.9% unemployment rate. That level doesn’t seem too constraining, and initial unemployment claims remain quite modest.

So, current US interest rates and unemployment look attractive versus what we experienced during the ’90s. It must be that economic growth was incredibly robust to support such strong equity markets. Well, again you’d be wrong. Sure economic growth averaged 3.2% during the decade, but the Atlanta Fed’s GDPNow model is forecasting a 3.5% growth rate currently for Q2’24. This comes on the heels of a rather surprising 2023 growth rate. What else could have contributed to the 1990’s successful equity market performance that isn’t evident today? How about fiscal deficits? Perhaps the US annual deficit during the ’90s contributed significant stimulus which would have led to enhanced demand for goods and services?

I don’t think that was the case either, as the cumulative US fiscal deficit of $1.336 trillion during the 1990s, including surpluses in 1998 and 1999, is roughly $400 billion less than that which occurred in fiscal 2023 and what is predicted for 2024. Oh, my. The largest fiscal deficit during the 1990s was only $290 billion. That’s equivalent to about 2 months-worth today.

I’m confused, the 1990s produced an incredible equity market despite higher rates, higher unemployment, lower GDP growth, and little to no fiscal stimulus provided by deficit spending, yet today’s environment is constraining? Come, on. Inflation remains sticky. The American worker is enjoying (finally) some real wage growth and is gainfully employed. Rates are not too high by almost any reasonable comparison. US GDP growth is forecasted to be >3%. Where is the recession? Fiscal stimulus continues to be in direct conflict with the Fed’s monetary policy. Something that those investing during the 1990s didn’t need to worry about. Taken all together, is 2024’s environment something to be concerned about, especially relative to what transpired in the 1990s? Should the Fed be looking to reduce rates? I’ll be quite surprised if they come to that conclusion anytime soon.