By: Russ Kamp, Managing Director, Ryan ALM, Inc.

In a recent article in Nakedcapitalism.com, titled “Private Equity Becomes Roach Motel as Public Pension Funds and Other Investors Borrow as Funds Remain Tied Up”, posted by Yves Smith, there was a reference to the Stone Ages. Smith wrote, “pension funds in particular have actuarially-estimated payout schedules to meet. In the stone ages, they used to buy bonds and match the maturity to expected obligations”.

In the stone ages that strategy of matching maturities was likely used (a laddered bond portfolio). Today, we have highly structured optimization models that can do a far more effective job of ensuring that the cash flow to meet benefit payments is available when needed (monthly) at low-cost and with prudent risk.

Given the elevated yields available to bond investors, why wouldn’t we want to once again explore a strategy that actually supports the primary objective in managing a DB pension which is to SECURE the promised benefits at low cost and with prudent risk? It doesn’t seem like the current approach is working any better. It seems as if the “norm” in asset allocation results in less transparency, higher costs, and little liquidity. That doesn’t seem like a winning formula, but what do I know?

The Heavyweight Fight May Be Tilting Toward Fiscal Policy

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

You may recall that on March 22, 2024, I produced a post titled, “Are We Witnessing A Heavyweight Fight?”. The gist of the blog post was the conflict between the Fed’s desire to drive down rates through monetary policy and the Federal government’s ongoing deficit spending. At the time of publication, the OMB was forecasting a $1.6 trillion deficit for fiscal year 2024. As I noted in a post on Linkedin.com this morning, the budget office has revised its forecast that now has 2024’s fiscal deficit at $2.0 trillion.

This additional $400 billion in deficit spending will likely create additional demand for goods and services leading to a continuing struggle for the Fed and the FOMC, as they struggle to contain inflation. I also reported yesterday that rental expenses had risen 5.4% on an annual basis through May 31, 2024. Given the 32% weight of rents on the Consumer Price Index (CPI), I find it hard to believe that the Fed will be successful anytime soon in driving down inflation to their 2% target.

As a result, we believe that US interest rates are likely to remain at elevated levels to where they’ve been for the past couple of decades. These higher levels provide pension plan sponsors the opportunity to use bonds to de-risk their pension plans by securing the promised benefit payments through a defeasement strategy (cash flow matching). Furthermore, higher rates provide an opportunity for savers to finally realize some income from their fixed income investments. So, higher rates aren’t all bad! I would suggest (argue) that rates have yet to achieve a level that is constraining economic activity. Just look at the Atlanta Fed’s GDPNow model and its 3.0% annualized Real GDP forecast for Q2’24. Does that suggest a recessionary environment to you?

For those investors that have only lived through protracted periods of falling rates and/or an accommodative Federal Reserve, this time may be very different. Forecasts of Fed easing considerably throughout 2024 have proven to be quite premature. As I stated this morning, “investors” should seriously consider a different outcome for the remainder of 2024 then they went into this year expecting.

ARPA Update as of June 21, 2024

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

I suspect (can only hope) that you woke up yesterday morning just itching to see what news I was going to share as it related to ARPA and the PBGC’s implementation of that critical legislation. Sorry to have disappointed you. Like most everyone else, my day just got away from me.

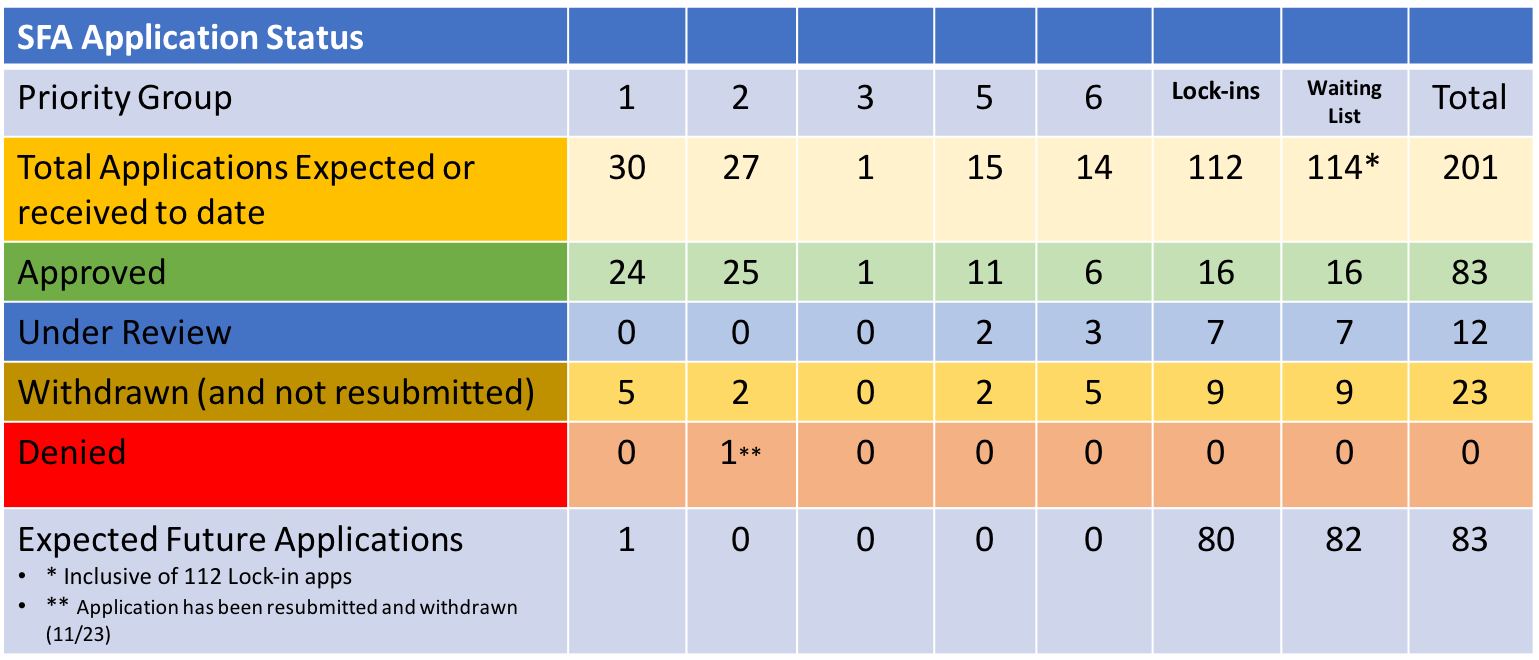

However, I do have some exciting news to share which might just make up for the disappointment of having to wait one day to get the weekly update. As we’ve been writing, the PBGC was running up against many application review and determination deadlines this month. As a result, they have announced that five funds had their applications approved for Special Financial Assistance (SFA). Terrific!

The five funds are the Retail, Wholesale and Department Store International Union and Industry Pension Plan, the Bakery and Confectionery Union and Industry International Pension Fund, United Food and Commercial Workers Unions and Employers Midwest Pension Plan, GCIU-Employer Retirement Benefit Plan, and the Pacific Coast Shipyards Pension Plan. These funds represent three Priority Group 6 members and two that came through the non-priority waitlist. In total, they will receive nearly $5.8 billion in SFA for just over 200k in plan participants. The Kansas Construction Trades Open End Pension Trust Fund is the last application that needs action in June. There are four that have July deadlines.

There were no new applications submitted to the PBGC, as the portal remains temporarily closed, no applications denied or withdrawn, and none of the plans that have received SFA were forced to return a portion of the proceeds as a result of overpayment identified through a death audit of the plan’s population.

Fortunately, the US interest rate environment and current economic conditions remain favorable for those potential SFA recipients to SECURE promised benefits far into the future without subjecting the grant proceeds to unnecessary risk associated with a non-cash flow matching assignment. Remember that the sequencing of returns is a critical variable when contemplating an asset allocation framework. If your SFA portfolio suffers significant losses in the early years, you negatively impact the coverage period. We’ll be happy to model your plan’s liabilities for free. Don’t hesitate to reach out to us if we can be a resource for you.

Good Ideas Are Often Overwhelmed!

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

We have a tendency in our industry to overwhelm good ideas with much too much money. Asset flows can be evil as they drive valuations up as too much money pursues to few good ideas. The “winner” in the bidding competition frequently (eventually) becomes the loser in the long run. I recently wrote about this phenomenon as it related to private credit. Well, we have a similar, if not more egregious example as it pertains to private equity. With more than $3.2 trillion tied up in aging, closely held companies at the end of 2023, according to Preqin data.

I recently read a refreshingly honest post on LinkedIn.com about the current state of private equity. The comments referred to a discussion given by a “leading” voice within the industry who mentioned that the “types of PE returns it (our industry) enjoyed for many years, you know, up to 2022, you’re not going to see that until the pig moves through the python. And that is just the reality of where we are.” That is quite the image. It speaks to my point about too much money chasing too few good ideas. Pension America has pursued a return objective in lieu of one that stresses the securing of the pension promise. Striving for return has forced most participants to load up on gimmicky alternatives, including real estate, private credit, private equity and worst of all, hedge funds.

For the early adopters, returns above those produced by the public markets were achievable, but again, once someone has a decent idea we tend to jump on that bandwagon until the horse can’t pull the cart any longer. What happens next is usually not pretty. This leading voice also mentioned that “fewer realizations and lower returns” were on the horizon until the proverbial pig was digested. Unfortunately, PE firms are holding onto these aging companies and they will need to be refinanced at much higher interest rates which will further reduce expected returns.

In other news, Heather Gillers, WSJ, reported that the honeymoon may be over between pension America and private equity managers. The promise of high returns may not be realized after all. According to Ms. Gillers, payouts from these expensive offerings have all but dried up. As a result, many pension funds are unloading their investments at significant discounts through secondary markets. According to this article, large public pension systems have migrated roughly 14% of the plan’s AUM into PE. What once looked like an investment that could produce a premium return is struggling to match returns of the S&P 500.

Worse, about 50% of the private equity investors have assets tied up in “Zombie funds”, which hadn’t paid out on the expected timeframe. Needing liquidity (should have invested in a cash flow matching strategy), these pension funds are getting an average of about 85% of the value of assets that were assigned just three to six months prior. According to Jefferies Financial Group about $60 billion was transacted in secondhand sales by PE investors last year.

Despite the lack of liquidity and the idea that too much money has been chasing too few good ideas, the “honest’ assessment by our industry “leading voice” stopped at their doorstep. You see, his firm believes that by 2026 (beginning or end of year???) their alternative assets under management will rocket from $651 billion to $1 trillion. Wow! Now how will that pig pass through the python? Are we to believe that growth of that magnitude will not negatively impact that firm or our industry? I guess that the news to date hasn’t been sufficiently ugly to stop this rampage into PE. I’ve seen this movie before. Spoiler alert – the train barrels forward until it goes over a cliff where the tracks used to be. I’d suggest getting off the next stop.

ARPA Update as of June 14, 2024

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

We hope that you enjoyed a wonderful Father’s Day. I’m blessed to still have my Dad with us (95 years young). In addition, I have two sons and two sons-in-law who are wonderful fathers. It was a terrific day!

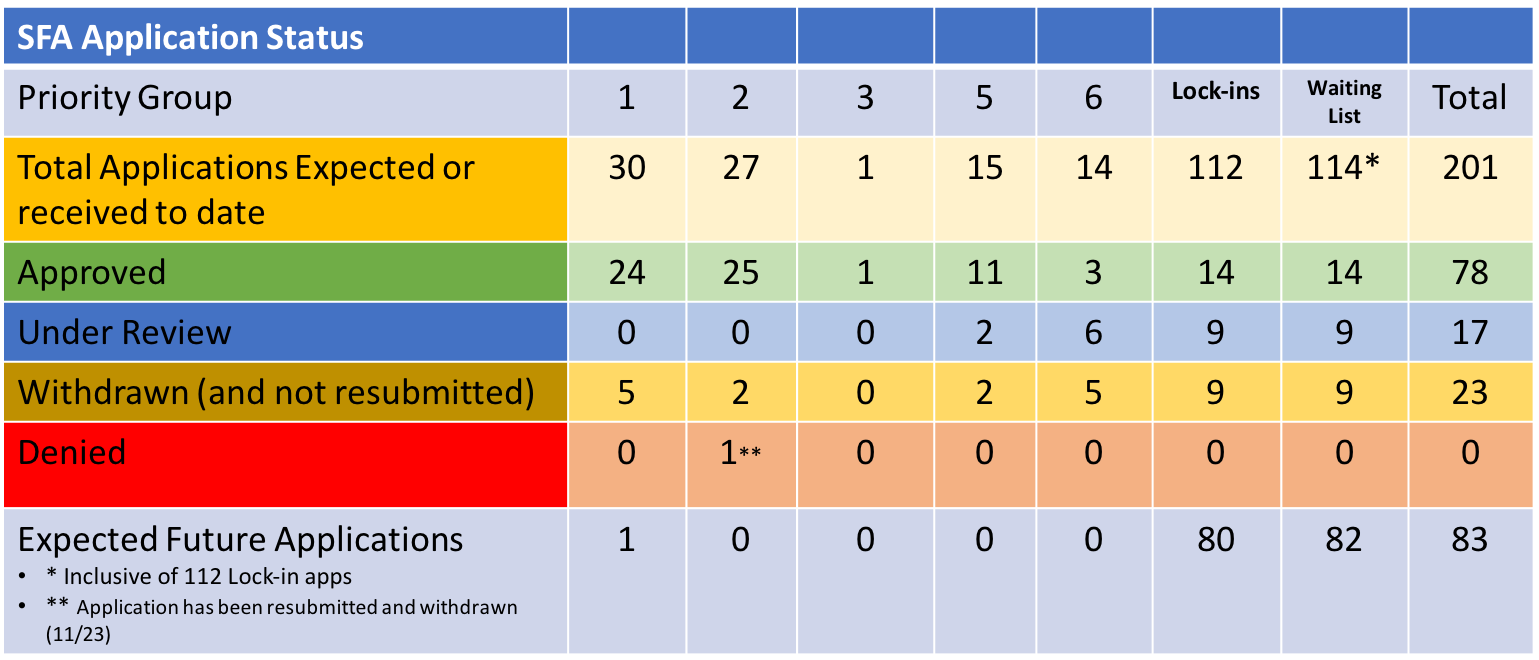

Regarding ARPA and the PBGC’s implementation of that critical pension legislation, there was some activity during the previous week. However, the filing portal remains temporarily closed for those plans still seeking relief through the SFA grants. That said, there are still 17 applications that are currently being reviewed with 6 of those nearing the 120 deadline for action. Those six plans are seeking nearly $5.5 billion in SFA. As a result, the rest of June is going to be busy for the PBGC.

The Pension Plan for the Arizona Bricklayers’ Pension Trust Fund received approval for its application. They will receive $10.7 million to protect the pensions for the 666 members of the plan. This non-priority plan received approval on their initial application. In other news, there were no applications either denied or withdrawn. However, the Graphic Communications Conference of the International Brotherhood of Teamsters National Pension Fund joined Central States as the only other plan to repay excess SFA as a result of a death audit. In this case, they are repaying just over $8 million.

Have a great week. Don’t hesitate to reach out to us if you like to learn more about cash flow matching and how it can be used to extend and protect the SFA grant assets so vital to ensuring that the pension promises are met for your participants.

The Smartest Beta

By: Ronald J. Ryan, CEO, Ryan ALM, Inc.

We are happy to share with you the latest thinking from Ron Ryan. Ron has written a very interesting article on the “smartest beta“. There is beta, a term coined by Bill Sharpe. Smart beta, which is the optimization of the risk/reward behavior of a market index usually by changing the weights of the index’s constituents. Then there is the smartest beta. The “smartest beta” portfolio, as described by Ron, is the portfolio that best matches and achieves the true client objective of funding liabilities with the least amount of risk and cost.

Risk is best measured as the “uncertainty of achieving the objective”. Cost is the amount required to fund the objective. The true objective of most institutions and even individuals is some type of liability (annuities, banks, insurance, lotteries, NDT, pensions, OPEB, etc.). The absolute level of volatility of returns is not risk given a liability objective.

Please don’t hesitate to reach out to us if you’d like to explore the concept of the “smartest beta” in greater detail. We’d welcome that opportunity.

Ryan ALM, Inc. Celebrates 20th Anniversary!

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Congratulations to Ron Ryan, a true visionary, and the Ryan ALM, Inc. team as they (we) celebrate the 20th anniversary of the firm. Ryan ALM was incorporated in Delaware on June 15, 2004. Ronald J, Ryan, founder, says that “we created our company to be dedicated to asset liability management (ALM) as our name suggests. We are quite proud of our progress and achievements in ALM. We have built a turnkey system of products that are quite unique in the ALM industry”.

We strive every day to protect and preserve defined benefit plans for the American worker. We continue to believe that the primary objective in managing a pension is to SECURE the promised benefits at low cost and with prudent risk. We thank all of our clients and their advisors who have provided us with the opportunity to support their efforts on a daily basis. Please don’t hesitate to reach out to us. We’ll work with you to find a unique solution to your specific issue(s).

Here’s to the next 20!

Corporate Pension Funding Improves Once More – Milliman

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Milliman is reporting improvement in the funded status for the largest corporate plans. According to the Milliman 100 Pension Funding Index (PFI), corporate funding improved from 103.1% to 103.4% during May, marking the fifth consecutive monthly improvement to start 2024. Milliman attributed the improved funding to asset gains driven by the year’s best month at 2.29% driving the indexes assets up by $22 billion to $1.3 trillion. With the decline in the discount rate of 15 bps, pension liabilities grew by $18 billion and now stand at $1.25 trillion. According to Zorast Wadia, the discount rate used by Milliman is the FTSE Pension Liability Index, which is similar to ASC 715 rates. As a reminder, Ryan ALM, Inc. has produced ASC 715 rates since 2007. The $4 billion difference between pension assets and plan liabilities produced the 0.3% funding improvement.

Milliman’s monthly reporting also includes scenario testing. In the latest work, Milliman forecasts 2024 and 2025 interest rates and asset returns. In the optimistic case they forecast the discount rate at 5.88% at the end of 2024 and 6.48% at the end of 2025, while assets grow at 10.4% per annum during that time. If achieved, the funded status for the Pension Funding Index would ratchet up to 110% at the end of 2024 and 123% by 2025’s conclusion. These levels would rival what we had at the end of 1999, when Pension America should have defeased the liabilities.

A pessimistic forecast has the discount rate falling to 5.18% by the end of 2024 and 4.58% by December 31, 2025. Assets under this scenario produce only a 2.4% annualized return. If this forecast were to become reality, the PFI funded status would be 98% by the end of 2024 and 89% by the end of 2025. Since most of us have no clue where rates are going in the next couple of years, why play the game. Defease your plan’s liabilities at the current level of rates. We’ve seen too often greed creep into the equation instead of sound risk management. Use this opportunity to substantially reduce risk by matching and funding benefits and expenses with asset cash flows of interest and principal.

ARPA Update as of June 7, 2024

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

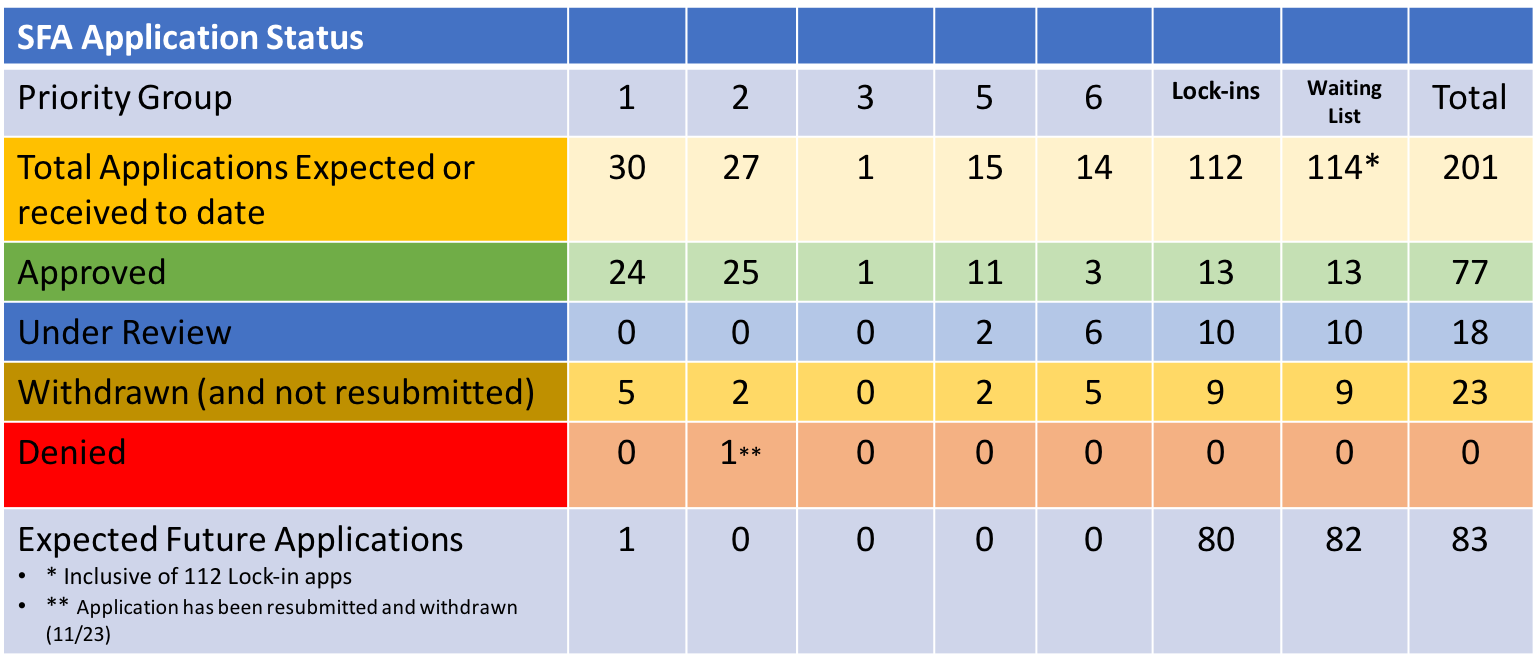

We are pleased to provide you with another ARPA update. The PBGC approved the applications for two New Jersey funds seeking Special Financial Assistance (SFA). CWA/ITU Negotiated Pension Plan and the Pension Plan of Local 102, both non-priority funds, will receive $545.6 million and $12.5 million, respectively, in order to ensure that their 24,796 participants will receive the promised benefits.

Unfortunately, there isn’t much else to report, as there were no new applications submitted, and the queue remains at 18. There were no applications rejected or withdrawn and no pension systems were added to the waitlist, with 32 of 114 having had some activity (submissions, withdrawals, and approvals) to date. Central States remains the only plan to pay back excess SFA proceeds.

The 18 plans that are currently under review carry some heft, as they are collectively seeking >$13 billion in SFA for nearly 370K participants. Seven of those plans have application “deadlines” in June. As a reminder, the PBGC has 120 days to act on an application once it has been submitted. Fortunately, US interest rates remain elevated providing plan sponsors with the opportunity to use cash flow matching to secure the SFA assets and significantly reduce the risk associated with a traditional asset allocation. Sponsors would be wise to use the legacy assets to assume a more traditional asset allocation since those assets now have the benefit of an extended investing horizon.

We hope that you have a wonderful week.

Money Managers Recaptured 1/2 the 2022 losses – Should We Be Pleased?

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

P&I has produced an article highlighting the fact that money managers recaptured nearly half of the institutional assets lost (-$9 trillion) in 2022’s market correction. They mention that this was accomplished despite “lingering economic and political uncertainties that kept a lot of money sidelined, including a record $6 trillion parked in money market funds alone.”

According to Pensions & Investments’ 2023 survey of the largest money managers, institutional assets for 411 managers around the globe rose 9.7%, or $4.89 trillion, to $55.23 trillion as of Dec. 31, 2023 for a recovery rate of 52.5%. This recapture of assets was primarily driven by equities, both US (+26%) and global X US (+18%), while bonds were up 5.6% domestically and abroad.

Obviously, it was great to see the “rally” despite wide-spread uncertainty related to the economy, inflation, interest rates, and the labor market. Issues that are still impacting perceptions today. But the real question one should ask has to do with the cyclical nature of markets and what plan sponsors and their advisors can do to mitigate the peaks and valleys. As I reported earlier this week, since 2000, public pension plans have seen a tripling (or more) in contribution expenses as a % of pay, while the funded status of Piscataqua research’s universe of 127 state and local plans has fallen by 25%.

Isn’t it time to get off the asset allocation rollercoaster? The nearly singular focus on return (ROA) by pension plan sponsors has placed pension funding on a ride that does little to guarantee success, but has certainly exacerbated volatility. In the process, contributions into these critically important retirement systems have skyrocketed. Let’s stop thinking that the only way to fund pensions is through outsized market returns. Today’s interest rate environment is providing plan sponsors with a wonderful opportunity to SECURE a portion of their future promises by carefully constructing a defeased bond portfolio that matches and funds asset cash flows of principal and interest with liability cash flows of benefits and expenses.

By doing so, you eliminate the impact of drawdowns, as the assets and liabilities will now move in tandem. How refreshing! Because you are defeasing a future benefit, you are also eliminating interest rate risk, as future values are not interest rate sensitive. Furthermore, you have now created a liquidity profile that is enhanced, as the bond portfolio now pays all of the benefits and expenses chronologically as far into the future as the allocation to the cash flow matching program lasts. Lastly, the growth or alpha assets can now grow unencumbered, as they are no longer a source of funding. The need for a cash sweep has been replaced by cash flow matching with bonds.

Let’s stop having to celebrate recovery rates of roughly 50%, when we can institute investment programs that eliminate these massive and harmful drawdowns. They aren’t helpful to the sustainability of DB pension plans, which we so desperately need if we are to provide a dignified retirement to the American worker. Let’s get back to the fundamentals, as the true objective of a pension is to fund benefits in a cost-efficient manner with prudent risk. It isn’t a performance arms race!