Credit to the PBGC for not letting Valentine’s Day get in the way of a productive week, as they continue to implement the ARPA legislation, which is quickly approaching its fourth anniversary!

The eFiling portal has been sporadically open since the beginning of the year. Last week they turned the spigot on a little more, as three non-priority group plans submitted applications, including Teamsters Local 277 Pension Fund, Teamsters Local 210 Affiliated Pension Plan and Cement Masons Local No. 524 Pension Plan. In the case of Local 277, this was the initial filing, while the other two submitted revised applications. In total, these three pension plans are seeking $153.2 million in SFA for the nearly 10k participants.

In other news, the checks are no longer in the mail, as Laborers’ Local No. 265 Pension Plan, Local 734 Pension Plan, Upstate New York Engineers Pension Fund, and The Legacy Plan of the UNITE HERE Retirement Fund received the approved SFA plus interest and FA loan repayments. The $800 million gorilla within this group was Unite Here receiving $868.8 million from a total distribution of $1.1 billion. I suspect that the 103,118 members of these plans slept pretty well this weekend knowing that the promised benefits had been secured.

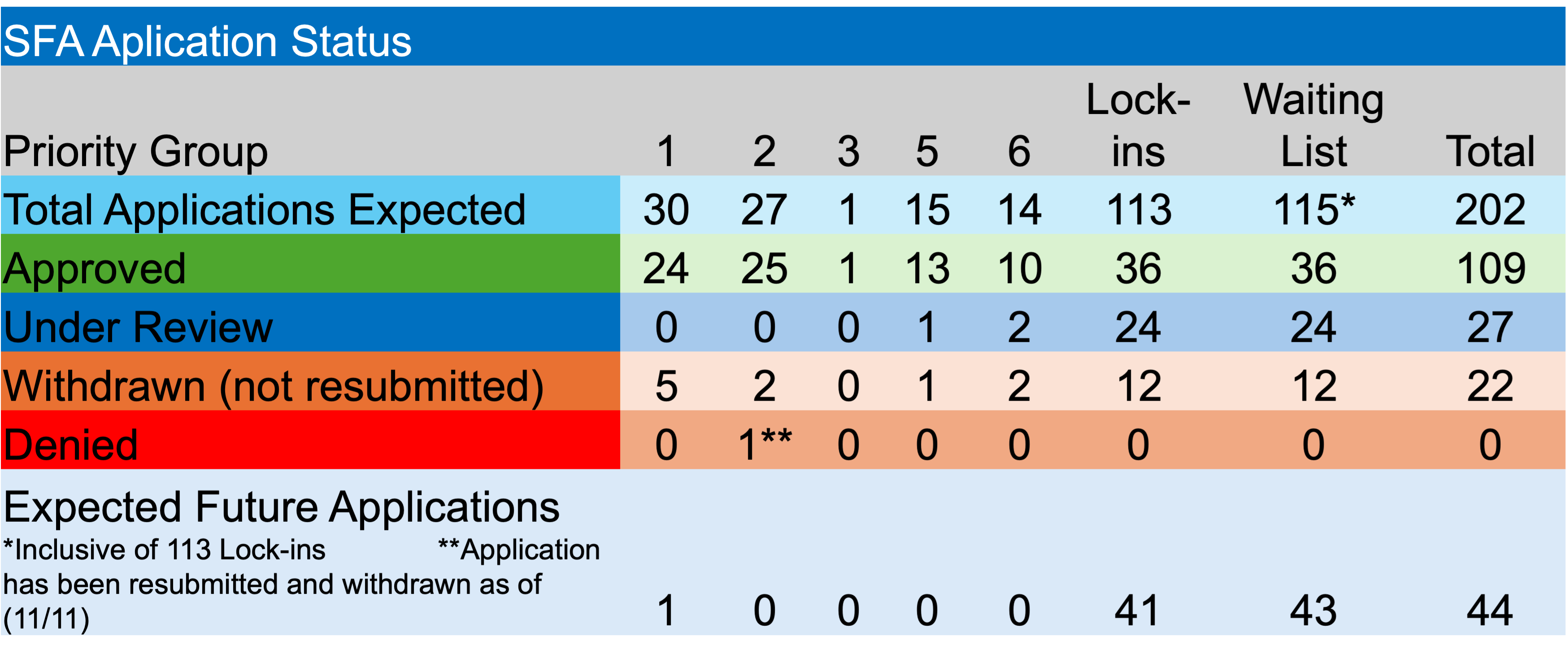

I’m pleased to report that no applications were denied during the past week. In addition, there were no plans required to repay excess SFA on account of census issues. Lastly, there were no new funds seeking inclusion on the waitlist. The chart below highlights where we are in the process. Despite the significant progress to date, there remains quite a bit of work for the PBGC.

Don’t forget, the legislation requires pension funds receiving SFA to rebalance the allocation between fixed income and equities back to 67%/33% one day every 12-months. Given the significant outperformance of equities vis-a-vis bonds plus the monthly benefit payments most likely coming from the fixed income program, there should be some significant rebalancing needs. It seems like a good time to reduce risk and take some profits.

Yesterday’s financial news delivered an inflation surprise (0.5% vs. 0.3%), at least to me and the bond market, if not to the U.S. equity market. The Federal reserve had recently announced a likely pause in their rate reduction activity given their concerns about the lack of pace in the inflation march back to its 2% target. This came on the heels of “Street” expectations after the first 0.5% cut in the FFR that there were “likely” to be eight (8!) interest rate cuts by the summer of 2025. Oh, well, the two cuts that we’ve witnessed since that first move last September may be all we get for a while. “Ho hum” replied the U.S. stock market.

The discounting of yesterday’s inflation release is pretty astounding. Like you, I’ve read the financial press and the many emails that have addressed the CPI data 52 ways to Sunday. Much of the commentary proclaims this data point as a one-off event. For instance, the impact of egg price increases (13.8% last month alone) is temporary, as bird flu will be contained shortly. Seasonal factors impacting “sticky-priced” products tend to be announced in January. I guess those increases shouldn’t matter since they only impact the consumer in January. As a reminder, Core inflation (minus food and energy) rose from 3.1% to 3.3% last month. That seems fairly significant, but we are told that the other three core readings were down slightly, so no big deal. Again, really? Each of those core measures are >3% or more than 1% greater than the Fed’s target.

Then there are those that say, “what is significant about the Fed’s 2% inflation objective anyway”? It is an arbitrary target. Well, that may be the case, but for the millions of Americans that are marginally getting by, the difference between 2% and 3% inflation is fairly substantial, especially when we come up with all of these measures that exclude food, energy, housing (shelter), etc. Are you kidding?

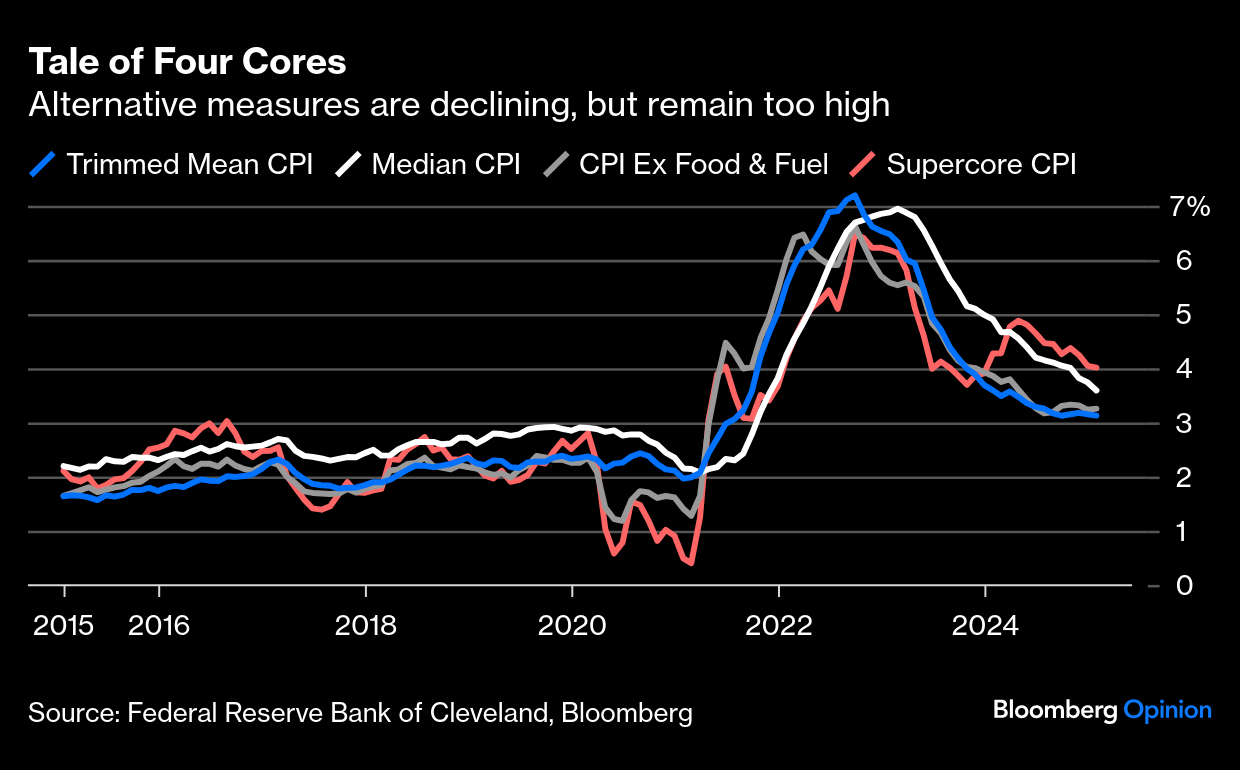

As mentioned previously, expectations for a massive cut in interest rates due to the perception that inflation was well contained have shifted dramatically. Just look at the graph above (thanks, Bloomberg). Following the Fed’s first FFR cut of 50 bps, inflation expectations plummeted to below 1.5% for the two-year breakeven. Today those same expectations reveal a nearly 3.5% expectation. Rising inflation will certainly keep the Fed in check at this time.

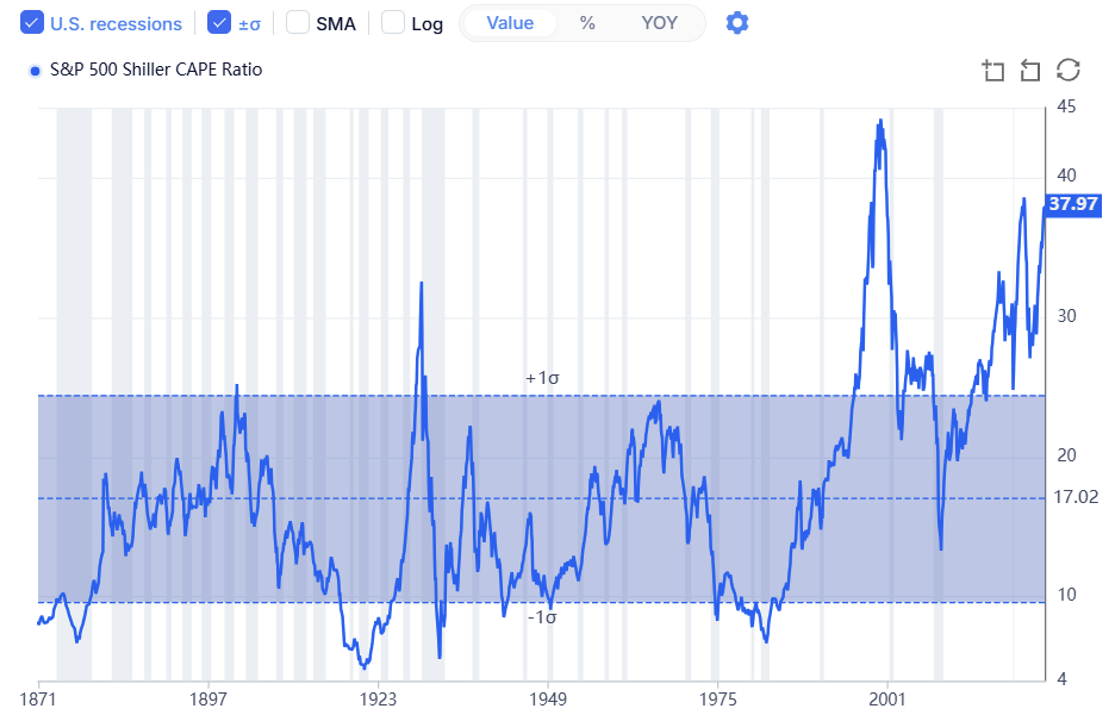

As mentioned earlier in this post, U.S. equities shrugged off the news as if the impact of higher inflation and interest rates have no impact on publicly traded companies. Given current valuations for U.S. stocks, particularly large cap companies, any inflation shock should send a shiver down the spines of the investing community. Should interest rates rise, bonds will surely become a more exciting investment opportunity, especially for pension plans seeking a ROA in the high 6% area. How crazy are equity valuations? Look at the graph below.

The current CAPE reading has only been greater during the late 1990s and we know what happened as we entered 2000. The bursting of the Technology bubble wasn’t just painful for the Information Technology sector. All stocks took a beating. Should U.S. interest rates rise as a result of the current inflationary environment, there is a reasonable (if not good) chance that equities will get spanked. Why live with this uncertainty? It is time to get out of the game of forecasting economic activity. Why place a bet on the direction of rates? Why let your equity “winnings” run? As a reminder, managing a DB pension plan should be all about SECURING the promised benefits at a reasonable cost and with prudent risk. Is maintaining the status quo prudent?

Milliman has provided its monthly update on the health of corporate America’s largest 100 pension plans with the release of the Milliman 100 Pension Funding Index (PFI). The good news continues, as the funded ratio for the PFI plans advanced last month from December’s 104.8% to 105.8% as of January 31, 2025. The improved funded ratio reflected both asset growth of $9 billion as a result of a 1.19% return for the index, while a minimal increase of 1 basis point in the discount rate (now 5.6%) reduced plan liabilities to $1.237 trillion. According to the Zorast Wadia, author of the Milliman PFI, the improved funded ratio marks a 27-month high.

Zorast went on to say, “With Fed rate cuts still a possibility this year, prudent asset-liability management remains a key directive for plan sponsors to preserve the funded status gains achieved thus far.” We don’t make interest rate forecasts at Ryan ALM, but we wholeheartedly agree with Zorast regarding the prudence of preserving the impressive funding gains realized during the last couple of years. Given the stretched equity valuations, taking risk of the table and securing the promised benefits through a cash flow matching strategy makes great sense.

Welcome to February! I am a day late in reporting on the PBGC’s activity from last week, as I was an instructor at the IFEBP’s Advanced Trustee and Administrator’s Conference. Fortunately, it is in Orlando and not New Jersey, where the weather remains cold, snowy, and wet! For one of the first times in my 43-year professional career I’m hoping for a significant flight delay of perhaps three days!

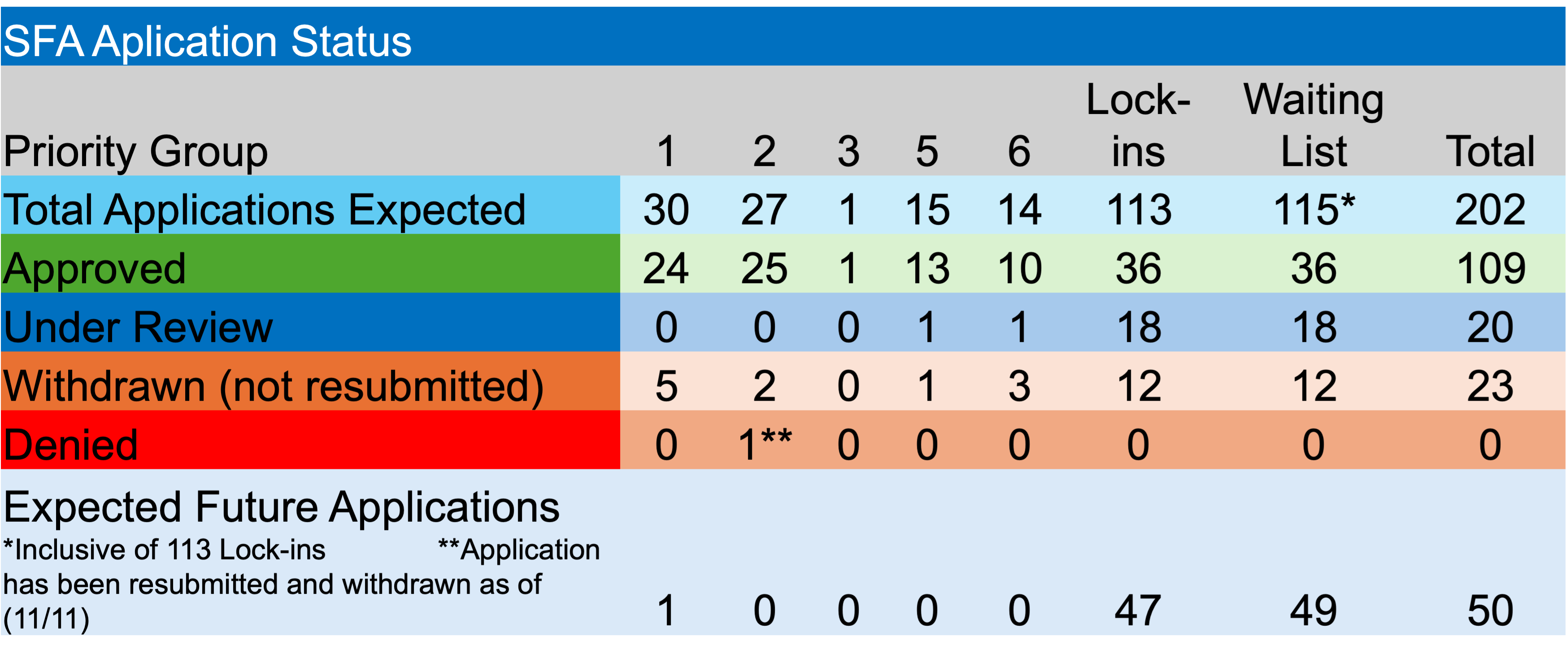

The PBGC’s eFiling portal is now open but defined as limited. During the previous week there was one new application submitted. The Retail Food Employers and United Food and Commercial Workers Local 711 Pension Plan is seeking $64.2 million in Special Financial Assistance (SFA) for their 25,306 plan participants or $2,538.65 per member, which seemed modest, and in fact it is, as the average SFA payout has been $46,385 per beneficiary on applications that have been approved.

In addition to the one new application, two non-priority plans, Laborers’ Local No. 130 Pension Fund and Pension Plan of the Asbestos Workers Philadelphia Pension Fund each withdrew an initial application. Collectively, they are seeking $72.4 million for 2,124 members.

There were no applications denied or approved during the past week. In addition, there were no plans required to repay an overpayment of SFA due to census errors. There hasn’t been a repayment since December 2024. Finally, there were no plans seeking to be added to the waitlist. There are still 49 plans waiting to submit an initial application to the PBGC.

The U.S. interest rate environment remains favorable for plans looking to defease the pension liabilities with the proceeds from the SFA. Investment-grade corporate bond portfolios are currently producing yields above 5% despite very tight spreads between corporates and the comparable maturity Treasury. Given the elevated valuations for domestic equities, particularly large cap stocks, now is the time to use 100% of the SFA to secure the promises.

PensionAge’s, Paige Perrin, has produced an article that referenced recent research from Ortec Finance. The research, which surveyed senior pension fund executives in the UK, US, the Netherlands, Canada, and the Nordics, found that 77% believe that risk will be elevated, either dramatically or slightly, in 2025. That’s quite the stat. It also follows on reporting from P&I that referenced heightened uncertainty by U.S. plan sponsors. As regular readers of this blog know, I’ve been suggesting to (pleading with) sponsors that they don’t need to live with uncertainty, which is truly uncomfortable.

Among several risks cited were interest rates, inflation, and market volatility. I can’t say that I blame them for their concerns. Who among us are able to adequately forecast rates and inflation? Seems like most fixed income professionals and bond market participants have been forecasting an aggressive move down in rates. Some of these prognosticators were forecasting as many as 7 rate reductions in 2024 and several others in 2025. We didn’t get 2024’s tally. Who knows about 2025 given that inflation has remained fairly sticky.

There is an easy fix for those of you who are concerned about interest rates and inflation. Adopt a cash flow matching (CFM) strategy that will carefully match asset cash flows of interest and principal with liability cash flows (benefits and expenses). Because benefit payments are future values (FVs), they are not interest rate sensitive. Problem solved! Furthermore, the use of CFM extends the investing horizon for the remainder of the fund’s growth assets, so they now have the appropriate time to grow to meet future liabilities.

One other startling stat caught my attention, as “77 per cent of senior pension fund executives believe the increasing number of retirees relative to the number of new hires in defined benefit (DB) plans pose a “significant” or “slight” risk to the DB pensions industry.” That concern is misplaced. I just wrote a post earlier this week on that subject. DB Pension plans are not Ponzi Schemes. They don’t need more depositors than those receiving payments. It is truly frightening that a significant percentage of our senior plan sponsors don’t understand how these plans are actuarial determined and subsequently funded.

Lastly, I nearly jumped out of my chair with excitement when I read the following quotes from Marnix Engels, Ortec Finance’s managing director for global pension risk, who stated the following:

“We believe assessing the risks of both (the bolding is my emphasis) assets and liabilities in combination is crucial to get the full picture on the health of a pension fund,” he said.

“If the impacts of risk drivers are only understood for one side of the funding health equation, then it is possible to misrepresent the overall effect.”

“If a fund is not assessing both assets and liabilities, then it is difficult to conclude the overall impact of interest rate hikes on the plan’s funding ratio.”

I recently stumbled onto an article that was highlighting the impending pension crisis (disaster) that is unfolding in Florida. The author’s primary reason for concern is the fact that there are now more beneficiaries collecting (659,333) than workers paying in (459,428). Briefly mentioned was the fact that the pension system currently has a funded ratio of 83.7% up from 82.4% last year. The fact that there are more recipients than those paying into the system is irrelevant. DB pension systems are not Ponzi Schemes, which in nothing more than a fraudulent vehicle that relies on a continuous influx of new “investors” (substitute plan participants) to pay the existing members of the pool.

A DB pension’s promises (benefit payments) are calculated by actuaries who have an incredibly challenging job of forecasting each individual’s career path (tenure), salary growth, longevity, etc. They do a great job, but they’ll be the first to tell you that they don’t get the individual participant calculations correct, but they do an amazing job of getting the total universe of payments nearly spot on. An acquaintance of mine, who happens to be an excellent actuary shared the following, “pension plans are funded over an active member’s career so that there will be sufficient funds to pay retirement benefits for life. The funding rules in Florida require contributions to get the plan 100% funded over time.”

Granted, there are states that have not made the annual required contribution, in some cases for decades, and those plans are suffering (poorly funded) as a result. That isn’t the actuary’s issue, but they are left to try to make up the difference by forecasting the need for greater contributions and more significant returns. The payment of contributions comes with little uncertainty, while the reliance on greater investment performance comes with a huge amount of uncertainty over short time frames. I wouldn’t want my pension fund or livelihood (Executive Director, CIO, etc.) dependent on the capital markets.

I frequently hear the concern expressed about negative cash flow plans (i.e. contributions do not fully fund benefits). Why? If pension systems are truly designed based on each participant’s forecasted benefit, mature plans are bound to eventually fall into negative cash flow situations. These plans are designed to pay the last plan participant the last $1 of assets. These pension systems aren’t designed to be an inheritance for some small collection of beneficiaries who make it to the finish line. Importantly, there should be different investment strategies used for plans that are collecting more than they are paying out versus those in negative cash flow situation.

DB pensions are critically important retirement vehicles that need to be protected and preserved. Fabricating a crisis based on an incorrect observation is not helpful. If plan sponsors contribute the necessary amount each year and manage the assets prudently, these pension systems should be perpetual. Neglect the basics and all bets are off!

I frequently get terrific questions following the publishing of one of my blog posts. Today’s question of the day was related to the ARPA pension legislation. I was asked, “Russ when does this legislation expire and when is the final date that a plans application must be submitted?” Terrific question. I’ve been meaning to provide this information as part of one of my weekly ARPA updates. Thanks for the prompt.

According to the final language in the Bill, ‘‘(f) APPLICATION DEADLINE.—Any application by a plan for special financial assistance under this section shall be submitted to the corporation (and, in the case of a plan to which section 432(k)(1)(D) of the Internal Revenue Code of 1986 applies, to the Secretary of the Treasury) no later than December 31, 2025, and any revised application for special financial assistance shall be submitted no later than December 31, 2026.

Furthermore, “The corporation (PBGC) shall not pay any special financial assistance after September 30, 2030.” As an aside, I’m not quite sure how a “revised” application that must be filed by 12/31/26 would not be paid before 2030 is beyond me, especially given the 120-day window to have an application acted on.

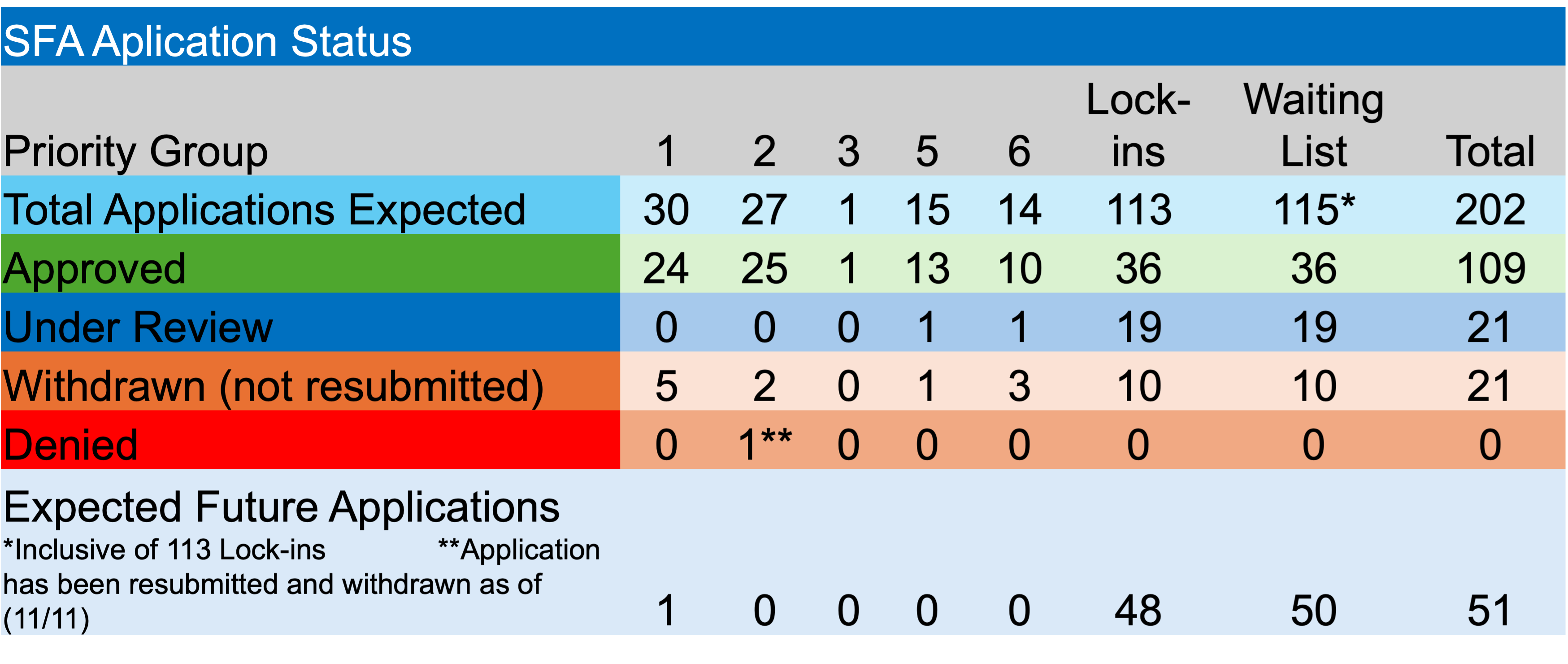

As reported in yesterday’s blog post, of the potential 202 applications, 109 have been approved, 21 are currently under review, while another 21 plans have withdrawn the applications. That leaves 51 plans that have yet to file (remember the 12/31/25 deadline) including a Priority Group 1 fund.

So, despite the terrific effort to date, the PBGC clearly has its work cut out for it. Currently, the eFiling portal to submit applications is closed. The PBGC has been opening and closing access to the filing portal based on its ability to meet the 120-day deadline. They may need to accelerate the pace of submissions and approvals in the coming months in order to complete the process by 12/31/26. Obviously, more to come from the PBGC. Also, keep your questions coming!

Somewhat shockingly, one month of 2025 is now in the books. That said, the PBGC continues to implement the ARPA legislation, which will soon celebrate its fourth anniversary since being signed into law on March 11, 2021. By all measures, this has been an incredibly successful program, with much yet to be accomplished with 93 pension plans still in the process of securing Special Financial Assistance (SFA).

The last few weeks have witnessed a moderation in the pace of implementation. The prior week saw no new applications received or approved. There was one application withdrawn, as Rocky Hill, CT-based, Sheet Metal Workers’ Local No. 40 Pension Plan withdrew their initial application seeking $18.8 million in SFA for 984 plan participants. In addition, there was one plan, St. Louis Motion Picture Machine Operators Pension Fund, that locked in the measurement date (liability valuation) as of October 31, 2024. They submitted the request as of January 24, 2025. With this action, there are only 2 plans of the 115 non-priority plans to have not locked in a valuation date.

I’ve previously mentioned the onerous impact of MPRA which passed in 2014. Fortunately, the PBGC/ARPA provided SFA of $477 million to restore to the 18 plans affecting 11 unions that under MPRA had reduced benefits an average of 22% for 60,620 retirees in pay status with some plans reducing benefits as much as 55 percent. These plans received an additional $3.5 billion in SFA to help ensure they remain solvent and able to pay all 87,862 participants in those plans their full retirement benefits through at least 2051.

For the first time since the dot.com bubble burst, the equity risk premium on the S&P 500 has fallen below 0. If you are concerned that U.S. large cap equities are looking frothy, this graph certainly supports that sentiment. Is now the time to take some equity profits and migrate those assets to bonds? We believe that the time is right to protect your enhanced funded status from the uncertainty as to where inflation and U.S. interest rates are going and the potential impact on traditional core fixed income strategies that are based on generic market indices instead of funding liability cash flows.

If you are like us (Ryan ALM, Inc.), and prefer not to make one’s living forecasting events that one can’t control, like interest rates, inflation, geopolitical events, etc., we suggest that you don’t engage in fixed income strategies that could be harmed by an upward movement in U.S. interest rates. Take those equity profits and invest in a cash flow matching strategy (CFM) that will secure your fund’s promised benefits, while eliminating interest rate risk since the process defeases future benefit payments that are not interest rate sensitive. A $1,000 monthly benefit payment is $1,000 whether rates are at 2% or 10%. In addition, you’ll be extending the investing horizon for the portfolio’s remaining growth (alpha) assets. CFM is the bridge over potentially troubled waters!

I’m going to divert from my normal focus on cash flow matching (CFM) and the defeasing of pension liabilities to write about a subject that I love and one that doesn’t get nearly the air time that it should. I was reminded of this topic at the FPPTA’s latest TLC program in Orlando, which I’ve thoroughly enjoyed participating. If you aren’t aware of the TLC (Thought Leadership Council) this is the FPPTA’s newest advanced educational program for experienced pension trustees. The program is limited to 20-25 trustees who get to roll up their sleeves with highly experienced coaches/mentors. I’m grateful to be included.

On Monday, one of the discussions centered on active managers, particularly US domestic equity managers, who have an incredibly challenging job trying to outperform their respective benchmarks, especially given the concentrated nature of the U.S. equity stock market during the last couple of years. Asset consultants have an even more challenging job trying to figure out which of those active asset managers will actually provide alpha NET of fees. As mentioned during one particular session, there are many aspects of the investment management process that are evaluated by consultants in an attempt to try and identify those few outperformers. These screening criteria may include the depth and consistency of staff, overall experience in managing the strategy, AUM in the product, and of course, performance. However, just because a manager outperformed (provided an excess return vis-a-vis the benchmark) an index at one point doesn’t mean it will happen again. Was the outperformance the result of skill or luck or a little of both?

As I explained to the TLC participants, stock selection factors (indicators or ideas) used to “pick” stocks to be included in the manager’s portfolio have an information content that can be measured. The “value-added” from an idea/factor can ebb and flow depending on a number of factors. Is the “deterioration” in the information coefficient (IC) an indication that the factor is losing it’s forecasting ability or is it just currently out of favor? As investment management firms get larger, the AUM that they control can overwhelm those insights diminishing the forecasting ability of that idea. Other investment management firms have bright people looking for an edge, too. They might just capture the same or similar insights rendering everyone’s use of that idea less robust, which I witnessed first hand in 2007’s quant manager meltdown. Below are two posts that touch on this topic. I hope that my ideas prove useful to you.

In a previous life, I was the CEO of Invesco’s quant business, which featured roughly 50 incredibly bright team members located both here and abroad and we managed about $30 billion in AUM. During our time together, we developed roughly 55 different strategies (optimizations), mostly U.S. equity mandates for which we had specific return/risk characteristics such as our Structured Core Equity product that was designed to achieve a 2% return for a 3% tracking error or a 0.67 information ratio versus the S&P 500.

We also thought that it was critically important to determine what we believed was the natural capacity of each strategy, as we didn’t want to arbitrage away our own insights. For instance, our Small Value product’s capacity was <$500 million, while many of the larger cap offerings had abundant capacity equal to billions of $s. Trustees should ask their managers what they believe is the natural capacity of the strategy(ies) that they are invested in and how they determined it.

Lastly, I would ask each manager to discuss a stock selection idea (factor / indicator) that they once used, but no longer do and why. Furthermore, I’d ask them to discuss an idea that they are now using to help them choose their portfolio constituents that they might not have been using 3-5 years ago. I’d make sure to understand how often they review every aspect of their investment management process. If that isn’t a normal part of their process, I’d be very concerned. For standing pat means that you are likely falling behind. It will be interesting to hear the replies.

Given how challenging it is to identify value-added managers as a consultant or consistently add value as an investment manager, I’m glad that Ryan ALM focuses on defeasing pension liability cash flows of benefits and expenses with asset cash flows from bonds (principal and interest). There is little uncertainty in our process. It is truly a sleep well at night strategy for all involved.