By: Russ Kamp, CEO, Ryan ALM, Inc.

I have the pleasure of drafting this post from beautiful Newport, RI, where I’m attending and speaking at the Opal Public Fund Forum East. The West forum’s location wasn’t too shabby either as it took place in Scottsdale last January! Business travel isn’t as glamorous as those who don’t travel think, but there are some nice perks, too. As they say in real estate: location, location, location!

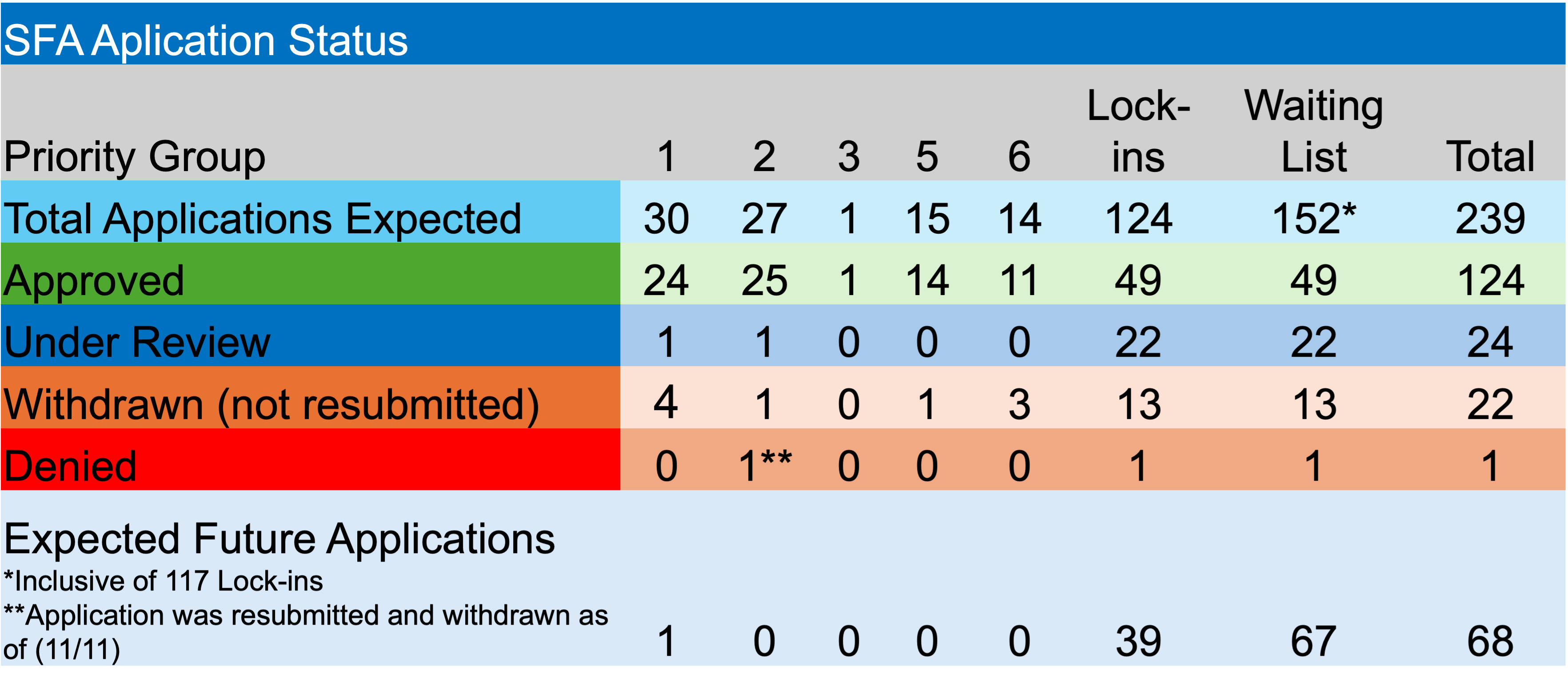

With regard to ARPA, since you likely didn’t decide to open post this to find Waldo or Russ, the PBGC was fairly busy during the previous week, as there was one new application, one approved application, two new additions to the waitlist and two funds that locked-in their measurement date. Now the details.

I’m pleased to report that the Roofers Local 88 Pension Plan, a Canton OH-based fund, has filed a revised application seeking $9 million for their 484 participants. As usual, the PBGC has 120-days to act on the application or it is automatically approved. In addition, Union de Tronquistas de Puerto Rico Local 901 Pension Plan, a San Juan, PR-based fund, a Priority Group One member will receive $49 million in SFA and interest for the 3,397 members.

In other news, Local 400 Food Terminal Employees Pension Trust Fund and the Textile Processors Service Trades Health Care Professional and Technical Employees International Union Local No. 1 Pension Fund (that name is a mouth full) have both added their funds to the PBGC’s waitlist for the submission of an SFA application. Good luck. There were also two funds from the waitlist, Iron Workers Local 473 Pension Plan and Greenville Plumbers and Pipefitters Pension Fund have locked in their measurement date and both chose April 30, 2025.

Lastly, there were no applications denied or withdrawn, and none of the previous SFA recipients were asked to rebate a portion of their proceeds due to census errors. As reported previously, the PBGC has their work cut out for them, as all of the outstanding applications need to be filed by year-end.