Milliman has reported that pension funding for Corporate plans declined in August. The Milliman 100 Pension Funding Index (PFI) recorded its most significant decline of 2024, as the funded ratio fell from 103.6% to 102.8% as of August 31, 2024. No, it wasn’t because markets behaved poorly, as the month’s investment gains of 1.81% lifted the combined plans’ market value by $17 billion, to $1.347 trillion at the end of the period. It was the result of falling US interest rates that impacted the liability discount rate on those future promises.

According to Milliman, the discount rate fell from 5.3% in July to 5.1% by the end of August. That 20 basis points move in rates increased the projected benefit obligations (PBO) for the index constituents by $27 billion. As a result, the $10 billion decline in funded status reduced the funded ratio by 0.8%. The index’s surplus is now at $36 billion.

Markets seem to be cheering the prospects of lower US interest rates that may be announced as early as September 18, 2024 following the next FOMC. Remember, falling rates may be good for consumers and businesses, but they aren’t necessarily good for defined benefit pension plans unless the fall in rates rallies markets to a greater extent than the drop in rates impacts the growth in pension liabilities.

“With markets falling from all-time highs and discount rates starting to show declines, pension funded status volatility is likely in the months ahead, underscoring the prudence of asset-liability matching strategies for plan sponsors”, said Zorast Wadia, author of the PFI. We couldn’t agree more with Zorast. As we’ve discussed many times, Pension America’s typical asset allocation places the funded status for DB pension on an uncomfortable rollercoaster. Prudent asset-liability strategies can significantly reduce the uncertainty tied to current asset allocation practices. Thanks, Milliman and Zorast, for continuing to remind the pension community of the impact that interest rates have on a plan’s funded status.

Football season has kicked off in earnest. If you are a NY Giants fan, as I’ve been for nearly 60-years, you are already looking forward to hockey! It wasn’t any better for fans of Notre Dame’s football team, which somehow lost to Northern Illinois.

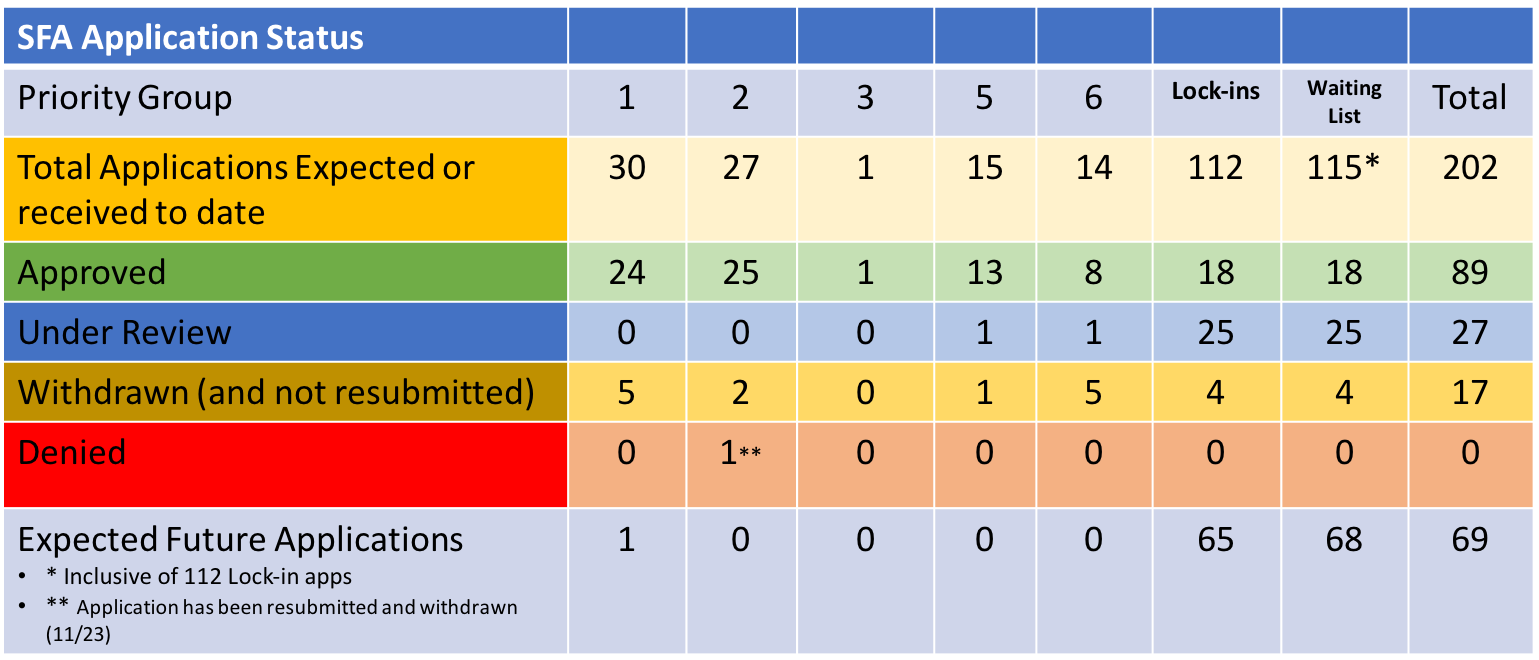

Now on to the important “stuff”. With regard to the PBGC’s effort implementing the ARPA pension legislation, last week was quiet. There were no new applications filed or withdrawn. There were no new applications approved, but there was one fund that received payment on 9/3 for its approved application. Printing Local 72 Industry Pension Plan received $39.4 million in SFA including interest. In addition, there were no plans added to the waitlist at this time.

Carpenters Industrial Council of Eastern Pennsylvania Pension Fund repaid excess SFA as a result of incorrect census data. They forfeited $106,298.69 from the original grant payment of $14.1 million or 0.75% of the proceeds. At this time, 13 funds have repaid $139.3 million or 0.36% of the grants. Of course, most of the rebate was from Central States, as its repayment makes up 91% of the total funds recaptured.

Uncertainty surrounding the upcoming Presidential election and the potential impact on markets (bonds and stocks) from the candidates’ policies (taxes, capital gains, social safety net, geopolitics, etc.) should keep recipients of the SFA taking precautions before diving into an asset allocation decision at this time.

One of the greatest attributes of managing a cash flow matching (CFM) portfolio is the fact that we don’t have to predict the direction of US interest rates. Most of us don’t have a clue about the direction, let alone the magnitude of the potential move. With CFM, you build the portfolio, and the cost reduction (savings) is locked in on day one, as future values are not interest rate sensitive.

Clearly, we and the plan sponsor community would like to see US rates remain fairly elevated, as higher rates equate to lower cost and more savings when using a CFM strategy. They also mean that coverage of the annual return on asset (ROA) objective is more certain, as opposed to traditional asset allocation frameworks that come with incredible volatility (annual standard deviation) and greater uncertainty in this environment.

All this said, we, at Ryan ALM, are still students of the markets, especially related to interest rates and the factors that impact those rates, such as GDP growth, labor markets, wages, inflation, geopolitical risk, etc. Clearly, the US investing community is excited at the prospect of the Fed’s FOMC cutting rates on September 18th. There appears little question that the Fed will act at that meeting. What is unknown at this time, is the magnitude of the potential cut. Will it be 25 bps or 50 bps or something entirely different. Who knows? However, those engaged in fixed income management certainly seem to have decided that rates will fall precipitously, as the Fed finally realizes the “error” of its way and reduces rates in a very meaningful way.

However, as the chart above highlights, rates have moved rather dramatically already without any action by the Fed. Since May 31, 2024, US Treasury yields for both 2-year and 3-year maturities have fallen by >0.9%. By almost any measure, US rates were not high based on long-term averages. Sure, relative to the historically low rates during Covid, US interest rates appeared inflated, but as I’ve pointed out in previous posts, in the decade of the 1990s, the average 10-year Treasury note yield was 6.52% ranging from a peak of 8.06% at the end of 1990 to a low of 4.65% in 1998. I mention the 1990s because it also produced one of the greatest equity market environments. Given that the current yield for the US 10-year Treasury note is only 3.74%, I’d suggest that the present environment isn’t too constraining. In fact, I’d suggest that the environment is fairly loose.

Could it be that there’s been an overreaction to the potential Fed easing? Might Fed action that results in smaller and fewer cuts lead to yields backing up from these levels? Again, who knows? Since none of us do, why don’t you get out of the guessing game and retain a strategy that doesn’t need rates to move down in order to add value. Bring a significant degree of certainty to the management of pensions where great uncertainty is the present name of the game.

We are pleased to share with you a recent white paper produced by Ron Ryan, Ryan ALM’s CEO. In this excellent piece, Ron reminds us of the fallacy that achieving the ROA as an underfunded DB pension system will make everything good – it won’t! As he correctly points out, the funded ratio may remain the same, but the funded status will continue to deteriorate. If the pension plan is 60% funded, at a market value of $100, that system has a funded status deficit of $40. If that 60% funded plan achieves the 7% ROA, assets will grow by $4.20. However, liabilities at that same discount rate will grow at $7. After 5 years, the funded status will have deteriorated by >40% and the deficit will now be >$56.

DB Pension systems that are poorly funded need to work extra hard to keep pace with the growth in the promised benefits or contribute significantly more to close the funding gap. There aren’t many plan sponsors in a position to contribute whatever is necessary to keep the plan in good funded status. Ron also discusses the need for plan sponsors to produce an Asset Exhaustion Test (AET), which is a requirement under GASB 67/68. It is a test of solvency. Ryan ALM modifies the AET to accurately determine the required ROA to fully fund the liability cash flows. Has your actuary produced the AET for your plan? If not, would you like Ryan ALM to calculate the ROA needed to fully fund your plan?

Please don’t hesitate to reach out to us with any questions that you might have regarding this white paper. Also, don’t hesitate to go to RyanALM.com for all the research that we’ve produced throughout the years. We look forward to being a resource for you.

We hope that you enjoyed a terrific Labor Day Weekend with family and friends. I can’t believe that we are 2/3rds of the way through 2024. Can you?

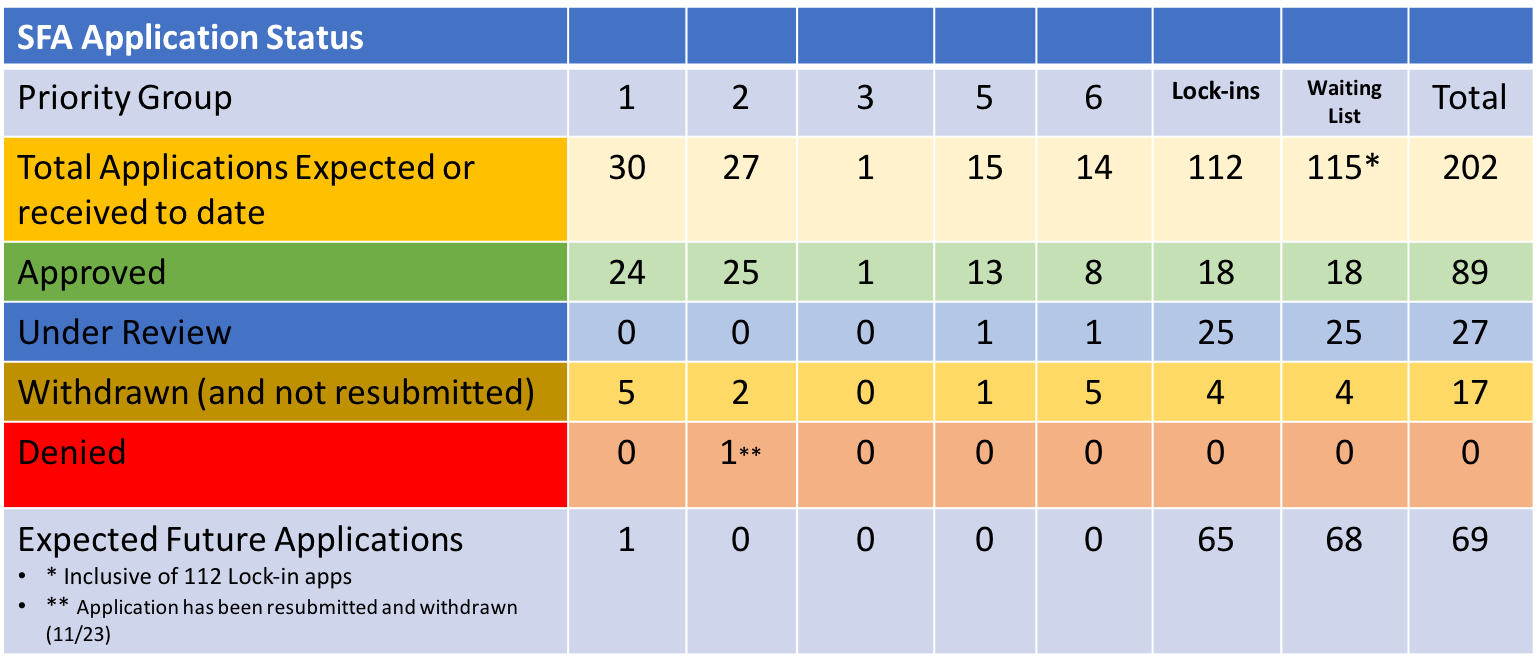

With regard to the PBGC’s effort implementing the ARPA legislation, there wasn’t a ton of apparent activity last week. We did have Teamsters Local 11 Pension Plan, a North Haledon, NJ (about 10 minutes from my home) non-priority plan file its revised application seeking $27.3 million in Special Financial Assistance (SFA) to help support the benefit promises to 2,012 plan participants.

There were no SFA awards last week. Furthermore, there were no applications denied or withdrawn. However, we continue to see some previous SFA recipients repay excess grant awards. In the last week, Laborers’ Pension Plan Local Union No. 186 and IBEW Local No. 237 Pension Plan repaid a total of $76,898.71 on grants of $79.8 million or 9.6 bps. Since the issue of overpayments due to incorrect census data was first recognized, nine pension plans have repaid a total of $138 million (mostly Central States) or 0.36% of the grants awarded.

There is still much to be done by the PBGC in completing the ARPA implementation. There are 113 potential applications that have yet to be approved, and in many cases, even reviewed (69). At this time, 44% of the expected applications have received SFA totaling $67.7 billion in SFA grants. That is an incredible total of benefits that have been secured. Let’s hope that the investment programs implemented are also securing those assets that have been received and benefits that have been promised.

As we get set to gather with family and friends for the upcoming Labor Day Weekend, let us reflect on the history of this Federal holiday. The Industrial Revolution during the late 19th Century led to the rise of labor unions advocating for workers’ rights, better working conditions, and fair wages. The first “Labor Day” parade, which featured a large gathering of workers, was organized by the Central Labor Union in New York City on September 5, 1882. While this gathering signaled the labor movement’s growing unity and determination to fight together for better working conditions, it would still be more than 15 years before the Labor Day Act was officially signed into law by President Grover Cleveland on June 28, 1894.

During the interim, and throughout the 1880s, numerous strikes and protests occurred, further highlighting the discontent of the working class. Notable events included the Haymarket Affair (aka Haymarket Riot) in May 1886, which was a rally organized in Haymarket Square, Chicago, IL to protest the killing of striking workers gathered to demand an eight-hour workday. Also, the Pullman Strike in 1894, which led to a nationwide railroad boycott and significant unrest, which finally brought labor issues to the forefront. It was after the Pullman Strike (May 11, to July 20, 1894) that the U.S. government sought to appease labor by establishing Labor Day as a federal holiday.

Despite the recognition (celebration) of Labor Day as a Federal holiday, the Labor movement in the United States has experienced many peaks and valleys since 1894. During the early 20th Century, the labor movement gained significant strength, leading to major labor laws, improved working conditions, and culminating with the establishment of the eight-hour workday. But there were tragic events, too. The Triangle Shirtwaist Factory fire is one of the deadliest industrial disasters in U.S. history. This fire caused death of 146 mostly young immigrant woman and ultimately led to significant reforms in safety standards.

Times weren’t as rosy during President Wilson’s eight-year tenure in office, as union membership and activities were disrupted by vigilante groups supported by American corporations. However, shortly thereafter, Ford Motor Company adopted the two-day weekend in 1926 to improve worker productivity and morale (I thought it was created to allow us to watch football). The conclusion of World War II witnessed a rebirth for Unions that once again thrived as the post-war economic expansion led to greater wages and benefits for workers, including more secure retirement benefits due to greater use of defined benefit pension plans.

Regrettably, during the later stages of the 20th century, union membership once again began to decline, this time due to a series of factors that combined to reduce labor’s overall influence including globalization, changes from a manufacturing-led to a service-focused economy, technological advancements, and anti-union legislation. However, in recent years, there has been a renewed interest in labor issues, with movements advocating for higher minimum wages, better working conditions, and support for gig economy workers. In addition, the PBGC is currently implementing the Butch Lewis Act, which was attached to ARPA in March 2021, with the goal to protect and preserve the promised retirement benefits for millions of American workers.

Again, as we sit back and enjoy good company, food, beverages, and a little R&R, remember the sacrifices made by countless American workers and their unions who sought better working conditions, wages, benefits, etc. that we all enjoy today. It’s through the strength of unions that further gains will be made.

“True heroism is remarkably sober, very undramatic. It is not the urge to surpass all others at whatever cost, but the urge to serve others at whatever cost.” — Arthur Ashe

Nasdaq eVestment has published capital market forecasts gathered from 11 leading asset consulting firms. The 2024 capital markets outlooks in their report were gathered across the self-authored documents in Nasdaq eVestment’s “Market Lens” from 11 consulting firms (AON, Callan, Cambridge, Cliffwater, Fiducient Advisors, Meketa, NEPC, RVK, Segal Marco Advisors, Verus, and Wilshire), who presented their findings to public plans. This report specifically focuses on the 10-year nominal, risk and return expectations from these consultants. I don’t mean to spoil that outcome, but the ending isn’t pretty.

According to this collection of forecasts, inflation is expected to average 2.34% for the next 10 years. US Large Cap (presumably the S&P 500) is only expected to produce a 6.3% annualized return or roughly 4.0% “real”. Worse, that 6.3% return is attached to an estimated 16.9% annual standard deviation. Despite less the stellar results for non-US equities, forecasts are for slight improvement relative to US equities, but only marginally so at 7.04%. However, it is accompanied with 19.2% annual volatility. The existence of a small cap “premium” is being called into question as small cap, which has dramatically underperformed large cap (15.0% (S&P 500) versus 8.9% (R2000)) for the last 5-years through July 31, 2024. That said, this collection of consultants believe that US-small cap can outperform large cap by 13 bps during the next 10-years, but in order to accomplish that feat, annual volatility is predicted to be 21.8% or roughly 5% greater than US-large cap.

With regard to alternatives, which seem to be drawing the most attention and cash flow activity, hedge funds (4.71%), private debt (8.28%), private equity (9.21%), real assets (7.71%), and real estate (6.90%) are also forecast to produce returns below historic norms. Furthermore, outside of hedge funds (6.85%), these forecasted results are accompanied by significant volatility projections. Private equity, the darling of the alternative set is forecast to produce annual volatility of 23.76% around that 9.2% forecasted 10-year result. Is the 9.2% worth the higher fees, lack of liquidity, and minimal transparency?

The darling of these forecasts is related to bonds, which may not have the highest predicted returns, but those forecasted results are achieved with very reasonable annual volatility. For instance, US core portfolios (likely related to the BB Aggregate) are forecast to generate a 4.8% 10-year result with only a 5.1% annual standard deviation. Interesting to note that the 4.8% estimated core fixed income return is 69% of the US – large cap return forecast but comes with only 26% of the annual risk. Furthermore, US short government/credit expectations call for a potential return of 4.28% for only a 2.83% annual variation. We are often asked to defease 1-5 years of a pension plan’s liabilities, which benefits from the attractive return/risk characteristics at the front of the yield curve.

I recently produced a blog post on the evolution of pension asset allocations and the tremendous change in the annual volatility associated with the migration of assets from traditional equity and fixed markets into various alternatives. Given the much higher fixed income returns now available to pension plan sponsors, hopefully asset allocations will once again reflect this reality at much more modest levels of risk.

From the report: “The higher interest rates of the last two years mean that many investors should be able to take on less risk than they have over the past decade if they want to achieve their target returns.” – Meketa

Again, the primary objective in managing a defined benefit plan is to SECURE the promised benefits at a reasonable cost and with prudent risk. It isn’t a return objective, which is a good thing given the 10-year projections cited in this report. Use the attractive fixed income yields to secure benefits (Retired Lives Liability) as far into the future as your fixed income allocation will cover. Not only do you have a dramatically improved liquidity profile, but you’ve just bought significant time for those non-bonds to achieve the forecasted returns, while wading through all that volatility.

I will produce another blog post on Social Security in October when the official COLA is announced. Currently, estimates are targeting an increase of roughly 2.6% for 2025 benefits. That is truly unfortunate because “Sticky” and “Core Sticky” inflation are far outpacing the likely 2.6% adjustment. Furthermore, the “Common Man” inflation rate is still in excess of 4%. This metric measures the inflation associated with “staples” and not discretionary items.

I’m bringing this to your attention today because of a note that I read in the Glen Eagle trading “Market Moment”, which I very much enjoy getting on a roughly weekly basis. In today’s email, they mentioned that “nearly half of workers plan to claim Social Security benefits before reaching full eligibility due to fears of the program running out of money or needing funds. The most popular ages to file are 65 (23%) and 62 (12%). Only 10% plan to wait until age 70 to receive the maximum benefit.” That is truly unfortunate. Most Americans have been told that Social Security is running out of money. In fact, they are warned that the end is coming soon. What a bunch of baloney. There are many reasons why folks choose to take this important benefit prematurely, but it should not occur because one feels that the SS “fund” will dry up.

As I’ve reported in previous blog posts, it is a fallacy to believe that there exists an “operational constraint on the government’s ability to meet all Social Security payments in a timely manner. It doesn’t matter what the numbers are in the Social Security Trust Fund account, because the trust fund is nothing more than record-keeping, as are all accounts at the Fed.” (Warren Mosler, “Seven Deadly Innocent Frauds of Economic Policy”) He continues, “When it comes time to make Social Security payments, all the government has to do is change numbers up in the beneficiary’s accounts, and then change numbers down in the trust fund accounts to keep track of what it did. If the trust fund number goes negative, so be it. That just reflects the numbers that are changed up as payments to beneficiaries are made.”

I worry about those individuals who decide to take the “benefit” at 62-years of age as they reduce future earnings from Social Security by 30%! That is a massive cut on a monthly basis. Furthermore, it never resets and future COLAs are predicated on the reduced amount. You also potentially impact what your surviving spouse my receive should you pass first. The US government enjoys the benefits of having a fiat currency. As long as our debts continue to be funded by US $s, we have no fear of SS running out of money. Congress making poor decisions as a result of its collective lack of knowledge on how our monetary system truly operates should be of greater concern. More to come in a couple of months.

Welcome to the last week of August. How did that happen? We wish for you a wonderful and safe Labor Day Weekend, especially for those families depositing children back at schools scattered throughout the US.

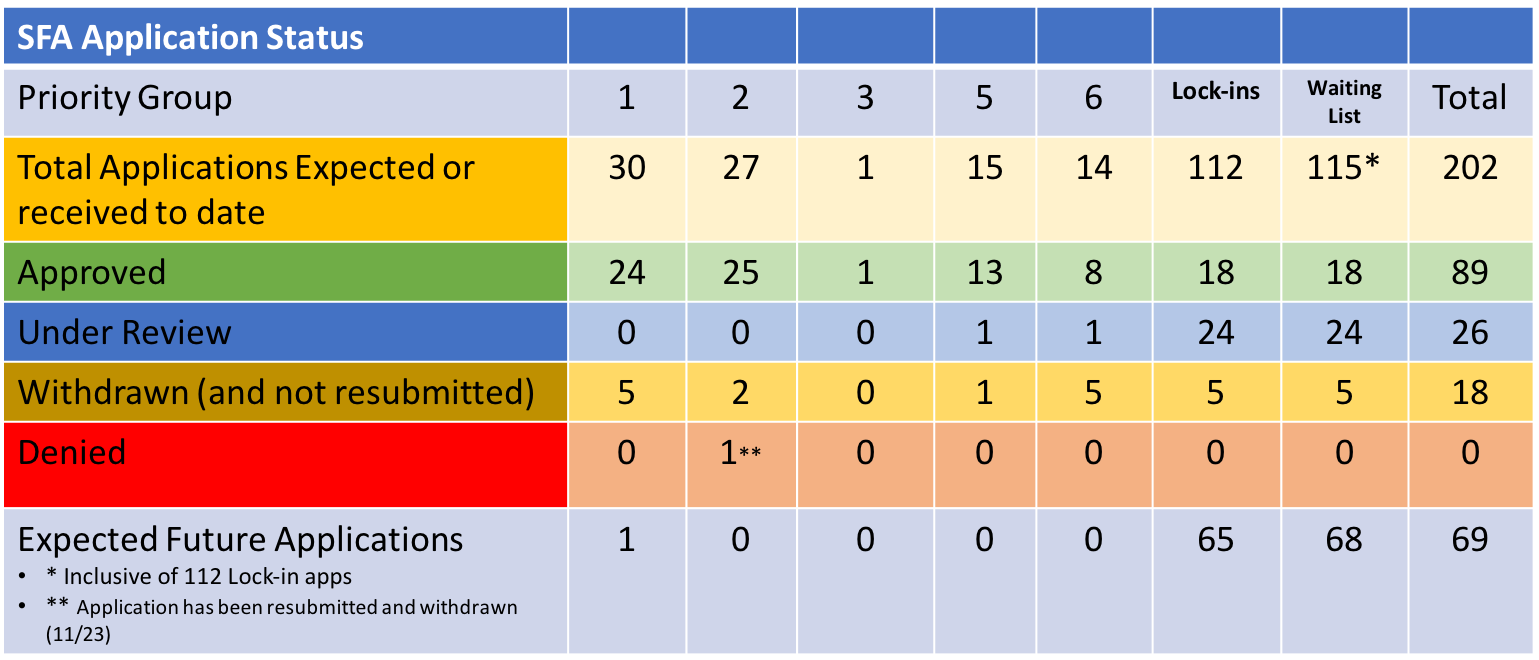

With regard to the implementation of the ARPA legislation, two more plans filed applications with the PBGC seeking Special Financial Assistance (SFA). Those plans include United Food and Commercial Workers Union and Participating Food Industry Employers Tri-State Pension Plan, a Priority Group 6 member and the Pressroom Unions’ Pension Plan, a non-Priority plan. Both have submitted revised applications. In the case of the UFCW plan, they are seeking $638.1 million for its more than 29K members, while the Pressman are seeking $59.2 million for its 1,344 participants.

In other ARPA news, three pension plans, including Idaho Signatory Employers-Laborers Pension Plan, Local Union No. 466 Painters, Decorators and Paperhangers Pension Plan, and United Independent Union – Newspaper Guild of Greater Philadelphia Pension Plan have agreed to repay the excess SFA received as a result of census errors, which amounted to $681,669.11 or 0.21% of the SFA grants.

There were no applications approved or denied during the week, and there were no applications withdrawn. Finally, there were no additional multiemployer pension plans seeking to be added to the waitlist, which currently stands at 69 applications that haven’t been submitted at this point.

Falling US rates would ordinarily help those plans seeking SFA as the lower discount rate inflates the present value of those liabilities. However, only a few of the applicants on the waiting list haven’t locked in the rate at this time. For those plans that have recently received grants or those that are hoping to have applications approved, the lower rate environment works against them in their pursuit to secure the promised benefits as far into the future as the allocation will go.

I very much enjoyed my two days attending the NCPERS conference. Not only did I get the opportunity to share some insights related to cash flow matching (CFM) and the application of this strategy for negative cash flow plans, but I also had the opportunity to listen to wonderful presentations related to a number of relevant topics. The Folks at NCPERS did a terrific job assembling a content rich forum.

One of the presentations that most impressed me was Gene Kalwarski’s. Gene is the CEO for Cheiron, a leading actuarial firm, and someone with whom I had the opportunity to meet through our work on the Butch Lewis Act. He and his firm did an incredible job analyzing 114 multiemployer plans that were thought to be potentially eligible for SFA at that time. At NCPERS, Gene’s presentation was focused on asset allocation for mature plans. He emphasized, and I absolutely agree, that more mature plans need a different asset allocation reflecting, in many cases, different liquidity needs, as they become more cash flow negative.

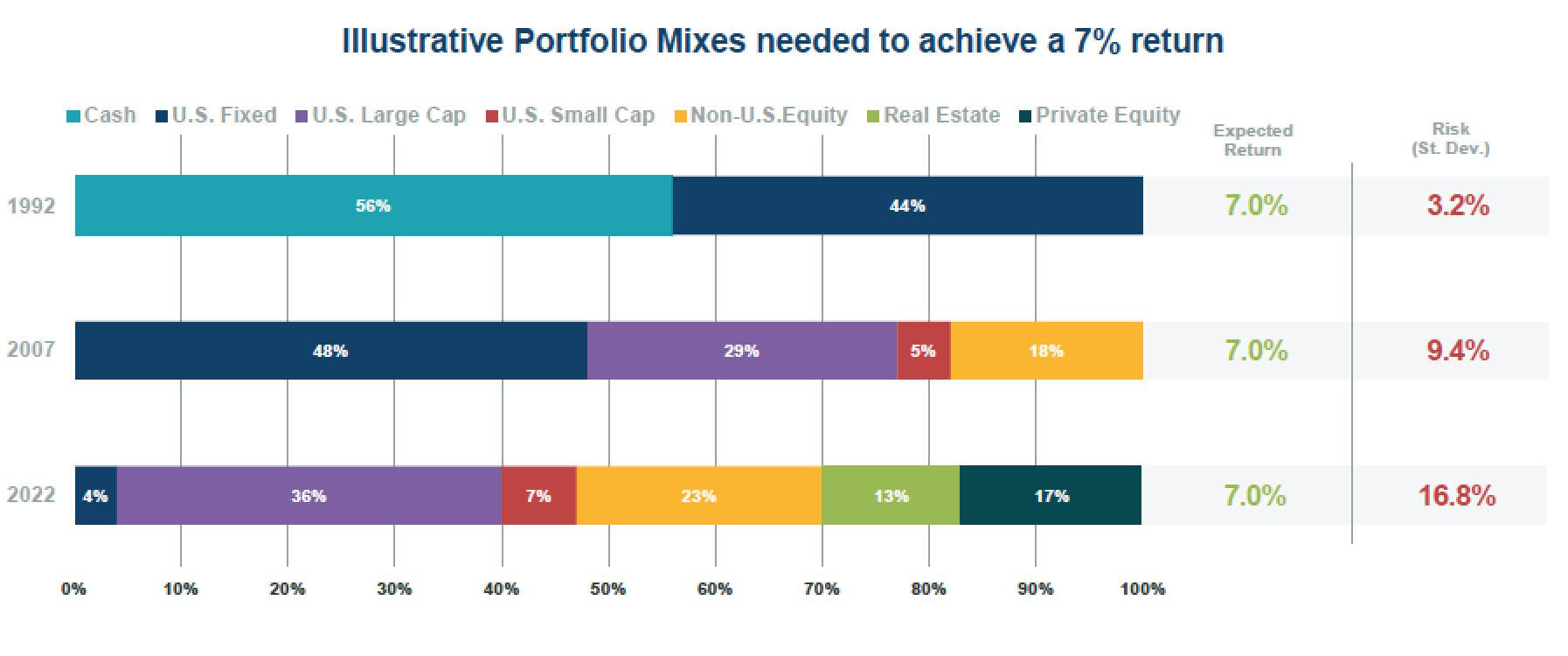

Regrettably, our industry continues to pursue a return focus, no matter how mature a plan may be, by cobbling together plan assets with the ultimate goal of achieving a return on asset (ROA) target. As I’ve written about this subject quite often, that objective hasn’t guaranteed success for the plan sponsor, but it has led to a significant increase in volatility, whether that be the funded ratio or contributions. Just how bad has the volatility of returns become? Gene presented the information in the graph below, which was produced by Callan.

It is incredible to see just how much risk plan sponsors are assuming through today’s asset allocation. Callan estimated that a pension system could strive for 7% in 1992 and would only expect a 1 standard deviation (SD) observation of +/- 3.2%. In other words, 68% of the time, that plan would have expected a return of +3.8% to +10.2%. Rather tame, wouldn’t you agree? By 2007, and just in time for the Great Financial Crisis, that 7% return objective came with a 1 SD observation of +/- 9.4%, meaning that plans should have expected that roughly 2/3rds of the time a result of between -2.4% and + 16.4%. Not great, but not horrible either.

Fast forward to 2022, or just in time for both equities and bonds to suffer meaningful losses, that 7% target now came with a 1 SD observation of +/- 16.8%. Wow! With that risk profile, a plan sponsor should not have been surprised with a return between -9.8% and +23.8%. That’s a far cry from the days when 68% of the observations fell between 3.8% and 10.2%. Unfortunately, that 1 SD observation only measures expectations for 13 out of 20 years. Since we can’t ignore the other 7 years, as much as we might like to, let’s extend the analysis to include 2 SD events or 95% of the observations (19/20 years). In this scenario, today’s asset allocation would create a range of results of -26.6% and +40.6%. That canyon of expectations should be horrifying! Why would any pension professional structure an asset allocation with such a potential dispersion?

In addition to the uncertainty of outcomes, this new asset allocation comes with increased fees, less liquidity, more opaqueness, and greater complexity. What a bargain! So, as many public pension systems mature, they enter the negative cash flow territory, in which liquidity to meet ongoing benefit payments becomes a greater challenge. Yet, these plans have truly hamstrung themselves through the migration of assets into alternatives. According to Callan, that allocation to alternatives is on average at least 30%, if not more depending on private debt usage today.

Given this incredible reality, mature public pension funds must begin to think of a strategy that will reliably provide the necessary liquidity to meet current benefits and expenses, while growing the corpus to close the funding gap that exists for most plans given the fact that Milliman has estimated that the average public pension system is only 80% funded. Cash Flow Matching (CFM) is the answer. Plan’s need to get away from a singular focus on return and begin to create an asset allocation strategy that bifurcates the assets into liquidity and growth buckets. The liquidity bucket will provide all of the necessary funds to meet benefits (and expenses) chronologically through a defeased bond strategy, while the growth bucket (non-bonds) will benefit from the extension of the time horizon. The objective for the growth bucket is future liabilities.

We, at Ryan ALM, Inc., are experts in CFM. We would be pleased to provide you with a free analysis of how CFM could positively impact your plan’s asset allocation, liquidity, transparency, etc. No pension plan sponsor should live in a world in which annual outcomes can be as wide as the Grand Canyon. How do you sleep at night given the current asset allocation frameworks come with a range of results at +/- 33.6% for 2 SD observations?