By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Welcome to Thanksgiving Holiday week. We wish for you and your family a day filled with love, laughs, and lots of great eating. I wish for myself a TV blackout so that I don’t have to watch the Giants!

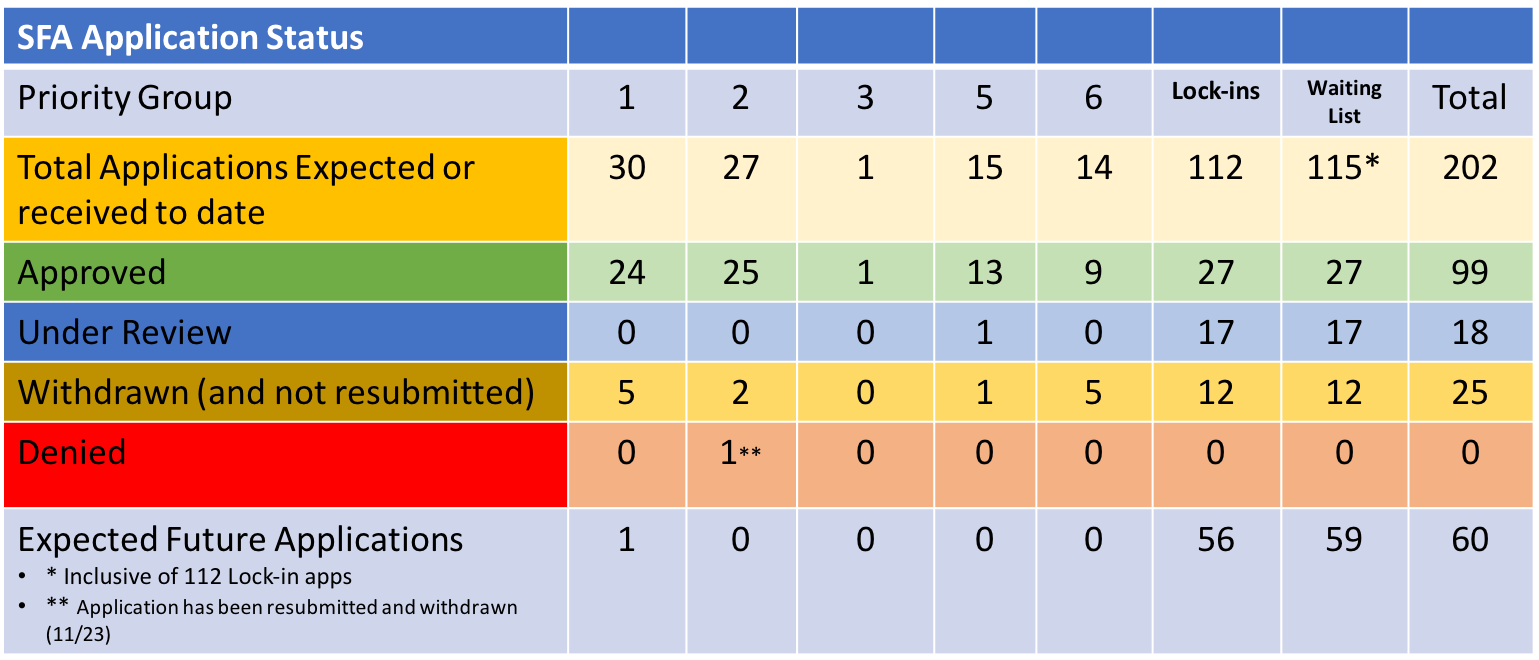

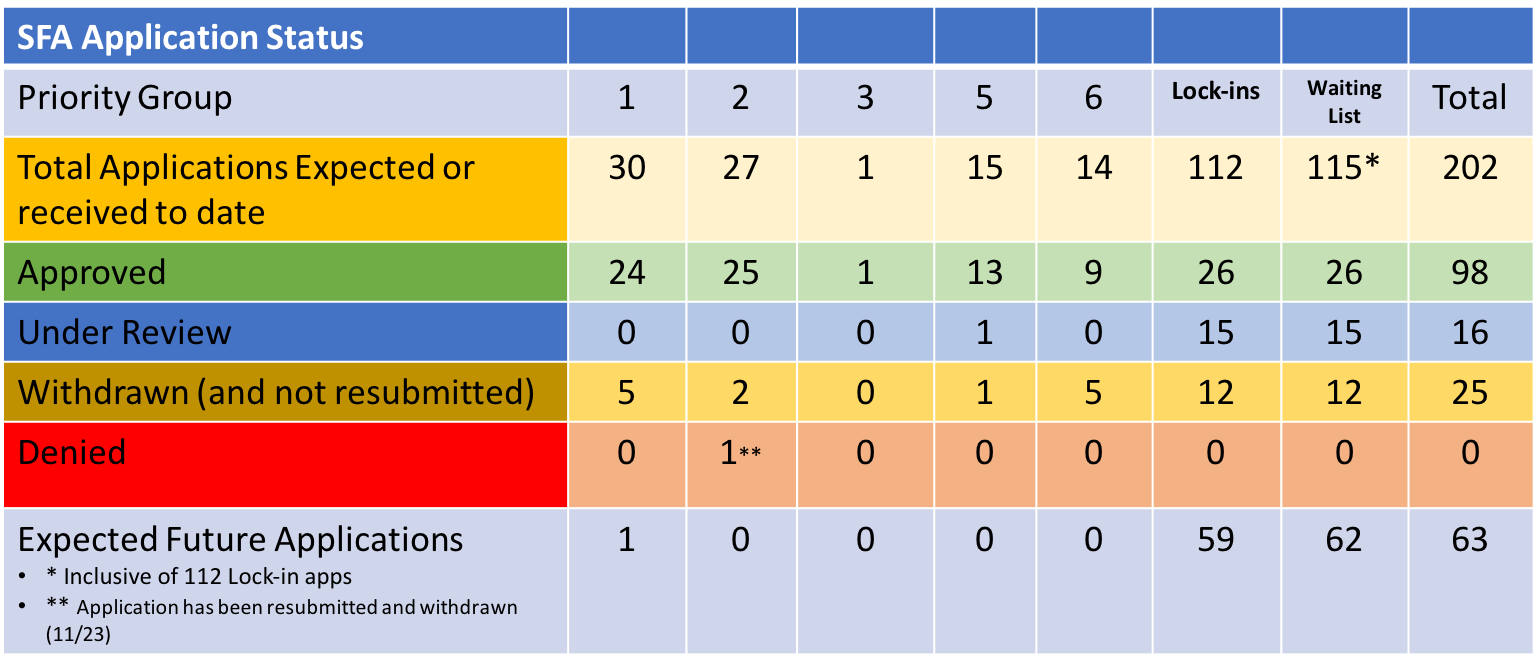

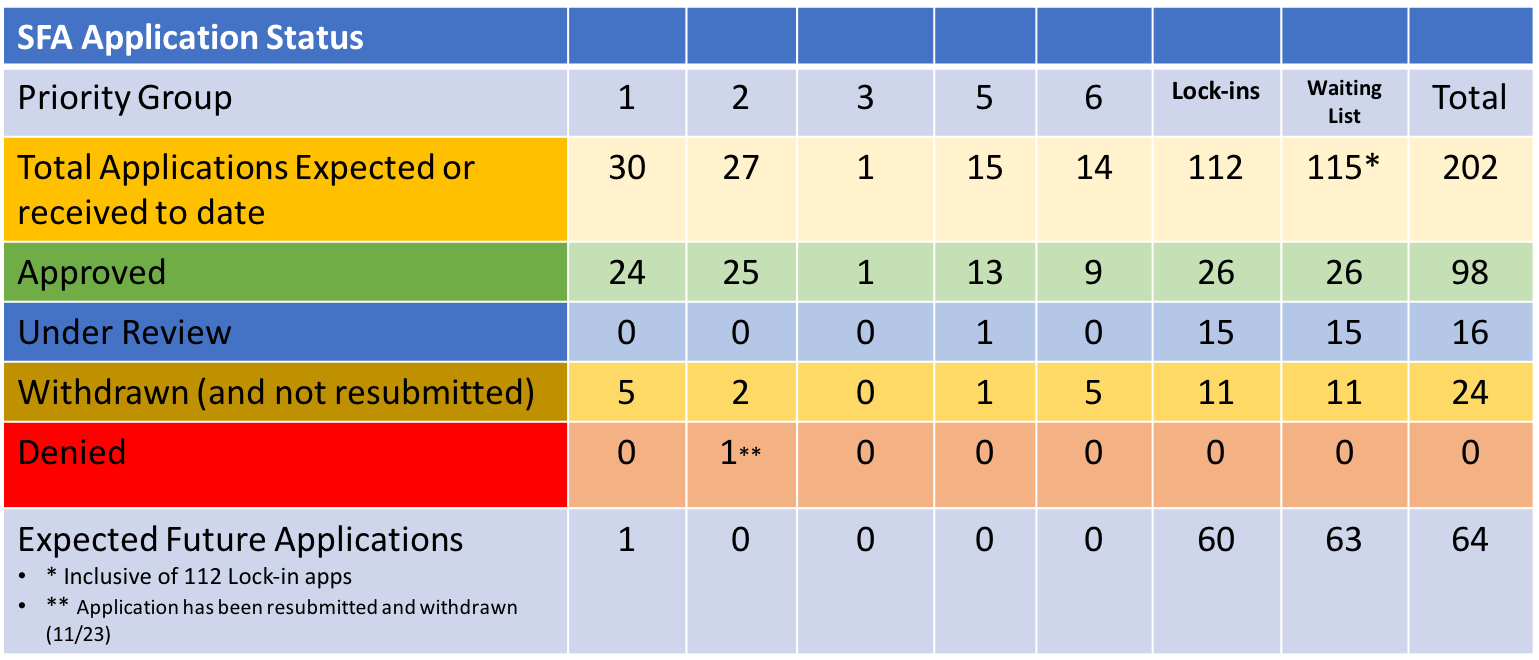

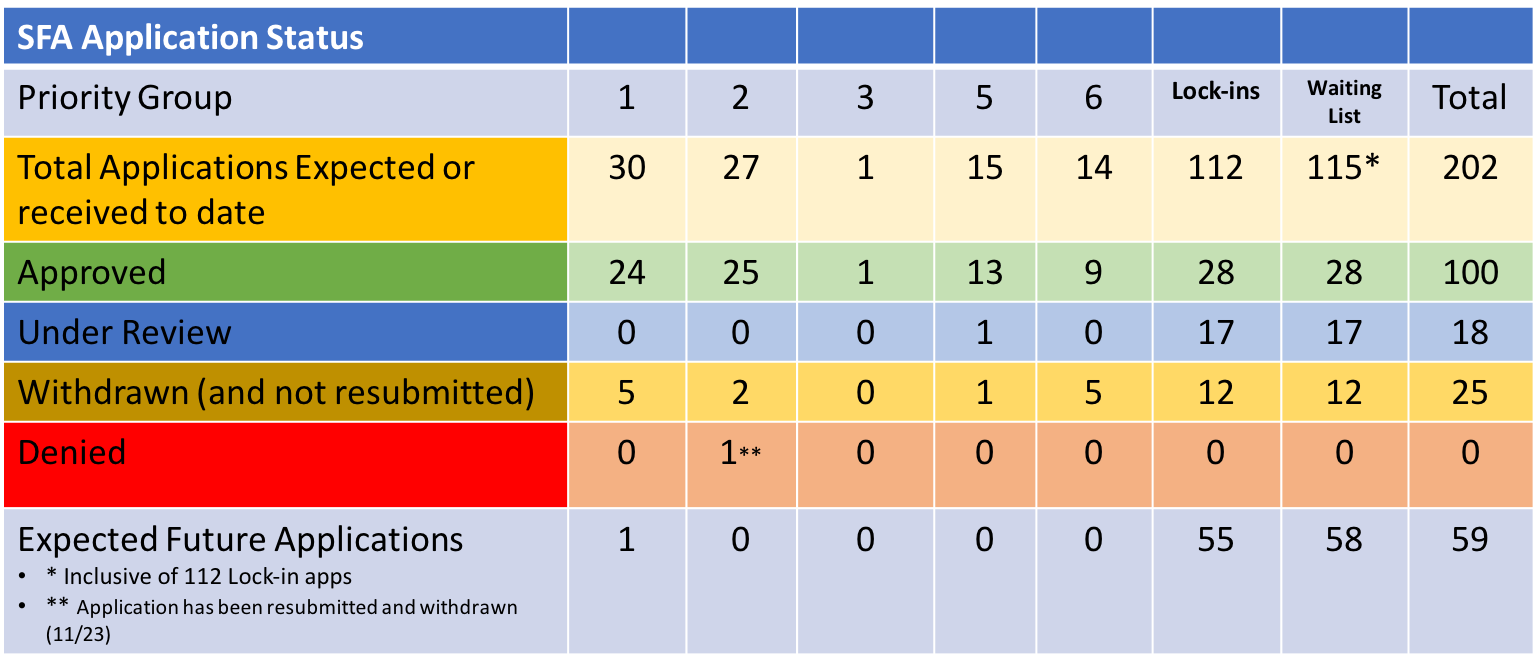

We are thrilled to report that the PBGC has approved the Special Financial Assistance (SFA) for the 100th multiemployer plan. Employers’ – Warehousemen’s Pension Plan, a Los Angeles, CA, based non-priority plan will receive $41.4 million in SFA grants and interest for its 1,821 plan participants. The PBGC has now approved grants in the amount of $69.5 billion. By our estimate, there are still 102 funds in the queue to potentially receive an SFA allocation. Clearly, there is much more to do.

In other news from last week, Laborers’ Local No. 265 Pension Plan was permitted to submit a revised application seeking just over $55 million to support its 1,460 members. Rounding out the week, there were no applications denied or withdrawn. There were no excess SFA funds returned. Finally, no pension funds sought to be added to the waitlist, which currently has 58 funds waiting to submit an initial application.

As we enter the Thanksgiving holiday week, let us be incredibly thankful for how beneficial the ARPA legislation has been for the 1,414,505 plan participants who have seen their promised benefits SECURED. For many of these pensioners who were in pension plans on the verge of collapse, the securing of these benefits through the SFA grants has been the difference between supporting oneself or being at the mercy of the Federal social safety net through no fault of their own. The nearly $70 billion may seem like a steep price to pay to some, but it is far less expensive than the cost of a pay-as-you-go system to support those 1.4 million American workers who buy goods and services with their pension checks. We all benefit from that activity. Great job ARPA and the PBGC.