By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Welcome to ECLIPSE DAY. Good luck found me in Dallas today for the TexPERS conference, as it is in the path of totality (complete darkness). Bad luck has it heavily overcast today following a Sunday that had beautiful blue skies. Oh, well. Perhaps we’ll get lucky.

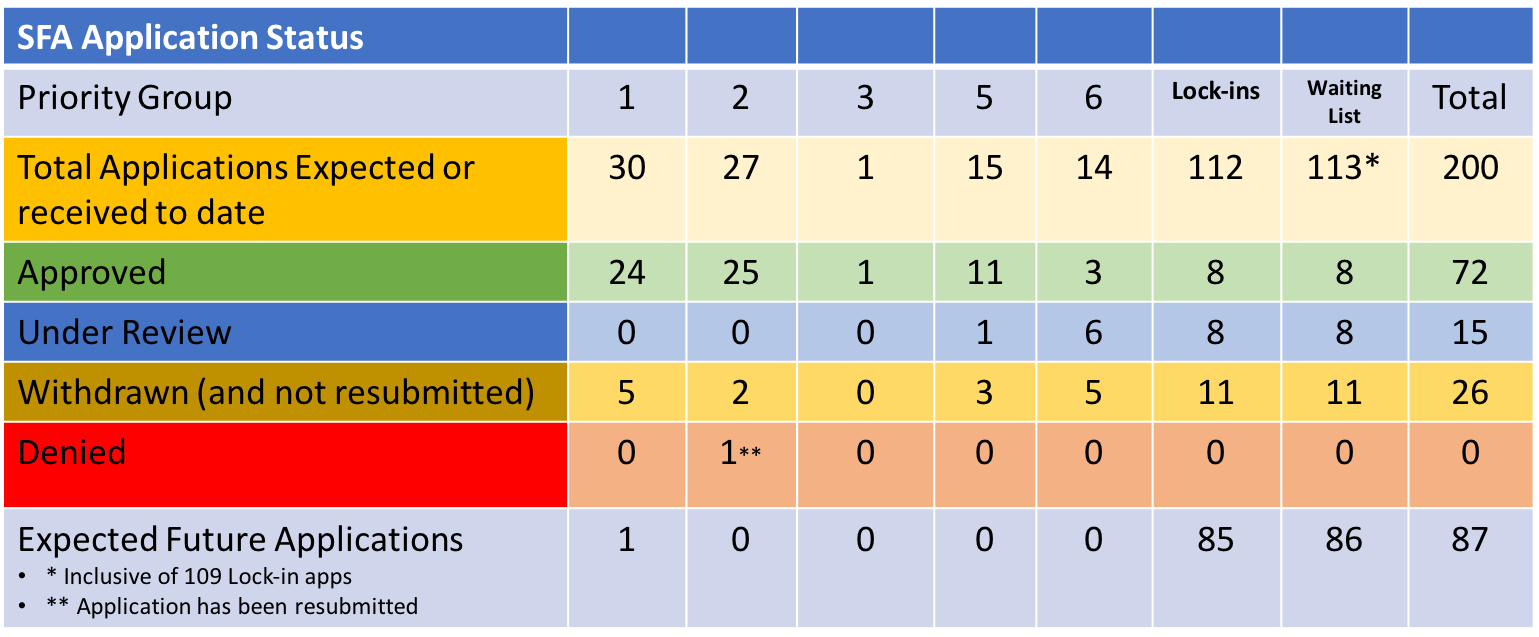

APRA’s implementation by the PBGC has slowed, and we don’t have earthquakes (NJ residents are still shaking their heads), eclipses, or any other natural event to blame. That is not to say that nothing has been done, as there was one new application received during the week. Printing Local 72 Industry Pension Plan, a Priority Group 5 member, submitted its revised application seeking $37 million in SFA for the 787 plan participants. Beyond that, I suspect that they are busy reviewing the 19 applications that have been submitted that are currently waiting on approval. Only 5 of those applications are the initial version.

As we’ve discussed in previous updates, census data used to determine SFA grant payments has had to be checked and rechecked following the announcement that Central States received more SFA grant $ than they were eligible to receive since some of the participants were no longer alive. That revelation and the corrective measures taken to ensure that SFA monies are only being allocated for eligible participants has really slowed an already cumbersome review. Despite some of these impediments, it is great that 72 plans have gotten the SFA awards totaling nearly $54 billion.

We might not have great visibility as it pertains to the eclipse, but with US interest rates tending higher, inflation remaining more “sticky” than hoped, and a Fed that may just not cut in 2024, visibility is clearer that cash flow matching the SFA is the way to secure the benefits and expenses well into the future. As a reminder, as rates rise, the cost to defease those promised benefits falls. Higher rates aren’t only good for savers. They are particularly good for SFA recipients and all plan sponsors of DB plans.

As an example of how that math works, when I entered this industry on October 13, 1981, the 10-year Treasury was yielding 14.9%. It would have only cost you $17.82 to defease a $1,000 30-year liability. On August 4, 2020, when the 10-year Treasury yield dipped to 0.52%, it would have cost you an extraordinary $860.40 to defease the same $1,000 30-year liability. As of April 5, 2024, the 10-year Treasury is yielding 4.41% and the cost to defease that 30-year liability is much more manageable at $301.00. You should be cheering for a higher for longer scenario.