By: Russ Kamp, Managing Director, Ryan ALM, Inc.

The WSJ produced an article on April 22, 2024 titled, “Path for 10-Year U.S. Treasury Yield to 5% Is Possible but Tricky” At the time of publication, the 10-year Treasury note yield was just under 4.7%. It is currently at 4.66%. Those providing commentary talked about the need to further reduce expectations for potential rate cuts of another 25 to 40 basis points. As you may recall, there were significantly greater forecasts of rate cuts at the beginning of 2024, but those have been scaled back in dramatic fashion.

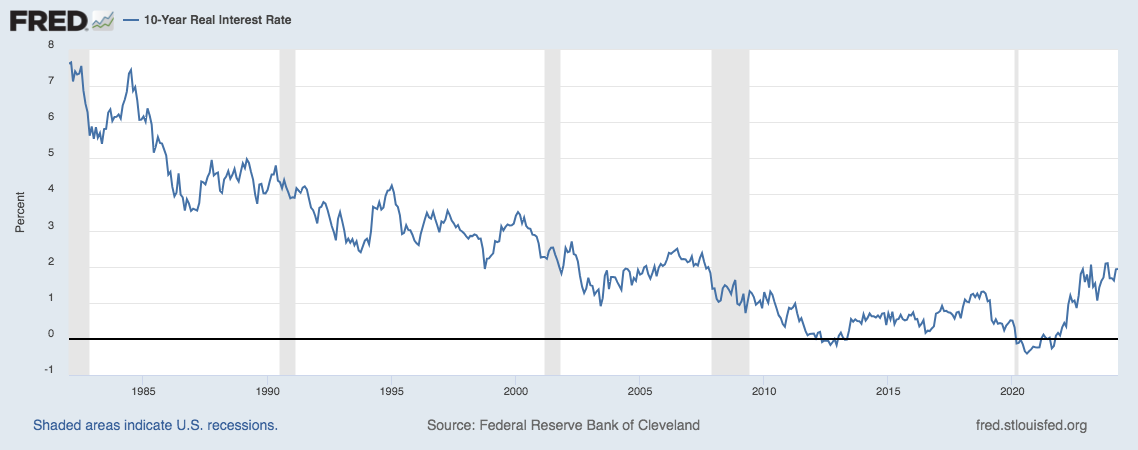

Given the current inflationary landscape in which the Consumer Price Index for All Urban Consumers (CPI-U) increased 0.4 percent in March and 3.5% annually, a move toward 5% for the US 10-year Treasury note’s yield shouldn’t be surprising or tricky. According to the graph below, the US 10-year yield has averaged a “real” yield of nearly 2% (1.934%) since 1984. A 2% inflation premium would place today’s 10-year Treasury note yield at roughly 5.6%.

Given the current economic conditions (2.9% GDP growth for Q1’24) and labor market strength (3.8% unemployment rate), it certainly doesn’t seem like the Fed’s “aggressive” action elevating the Fed Funds Rate from 0 to 5.5% today has had the impact that was anticipated. Inflation in 2024 has been sticky and may in fact be increasing. Should geopolitical issues grow in magnitude, inflation may get worse. These current conditions don’t say to me that a move to a 5% 10-year Treasury note yield should be tricky at all. As a reminder, the yield on this note hit 4.99% in late October 2023. Financial conditions have not gotten more restrictive since then.

Should the Treasury yield curve ratchet higher, with the 10-year eventually eclipsing 5%, plan sponsors would have a wonderful opportunity to secure the future promised benefits at significantly reduced cost in present value terms, especially if the cash flow matching portfolio used investment grade corporate bonds with premium yields. Although US corporate bond spreads are tight relative to average spreads, they still provide a healthy premium. Don’t let this rate environment pass without taking some risk from your plan’s asset allocation. We’ve seen that scenario unfold before and the outcome is scary.