By: Russ Kamp, CEO, Ryan ALM, Inc.

I’ll be wearing my green tomorrow. How about you? Perhaps the luck of the Irish will carry some weight with the PBGC during the upcoming week, but it didn’t have much sway last week.

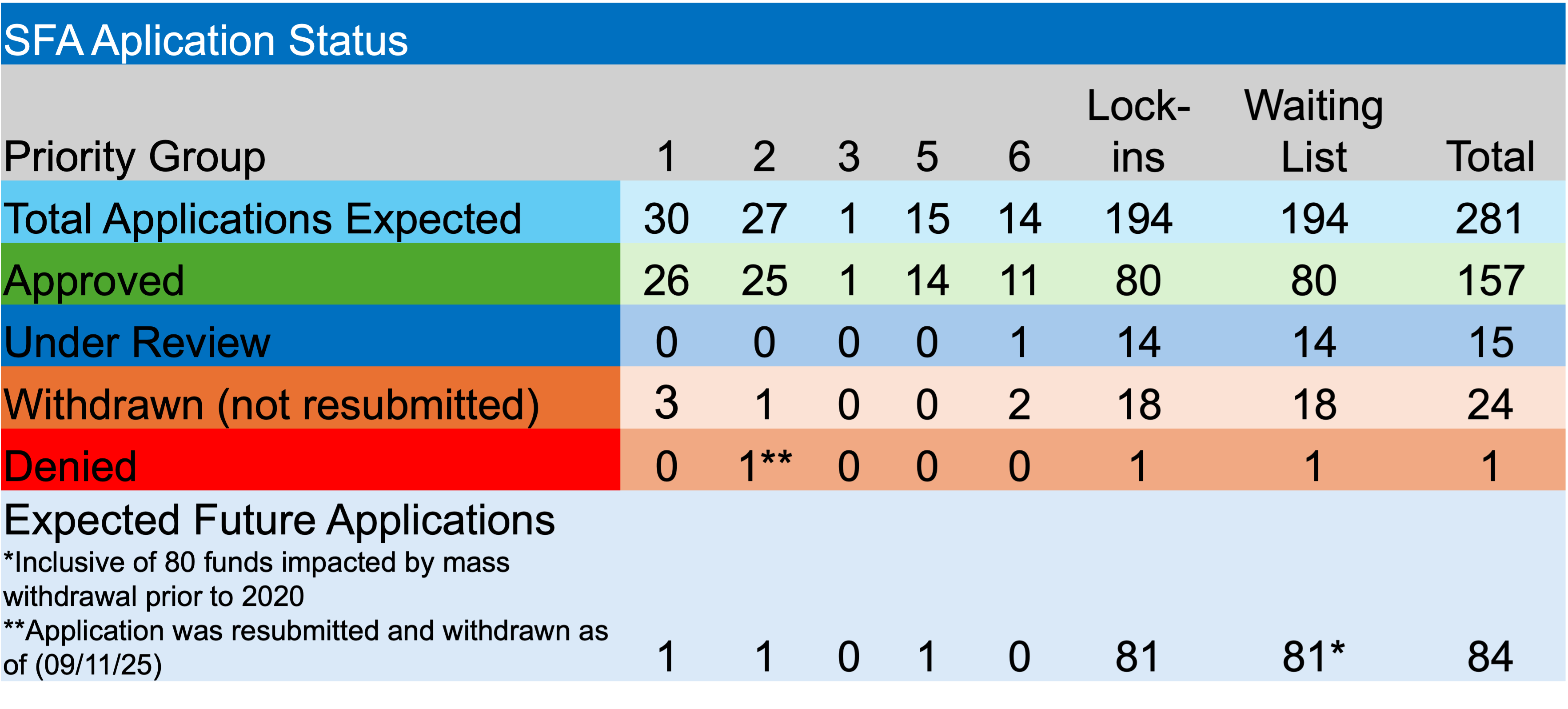

The PBGC accepted two revised applications for Special Financial Assistance (SFA) for the week ending March 13th. Iron Workers Local No. 12 Pension Fund and the Iron Workers-Laborers Pension Plan of Cumberland, Maryland submitted revised applications. Together they are seeking a modest $24.2 million for their 1,413 plan participants. The PBGC will have 120-days to act on the applications.

According to the PBGC’s website, their e-Filing Portal remains temporarily closed. As discussed previously, there is one fund currently on the waitlist that hasn’t submitted an initial application that is not classified as a Plan Terminated by Mass Withdrawal before 2020 Plan Year.

In other ARPA news, there were no applications approved or denied in the past week, and none withdrawn. The PBGC currently has 15 applications under review, including nine that are an initial application. Fortunately, it seems as if any SFA recipient that might have had to repay a portion of the grant due to census issues has done so at this point. There have been no payments of excess funds since last September.

There has not yet been a public, plan‑by‑plan PBGC resolution of the mass‑withdrawal‑terminated plans on the SFA waitlist. As previously mentioned, the legal landscape has changed (2025) which puts pressure on the PBGC oversight. What changed from the original interpretation of “eligible plans” was the Second Circuit’s decision held that the SFA statute does not exclude multiemployer plans that had previously terminated by mass withdrawal, reversing PBGC’s denial of SFA to a fund that terminated in 2016. Furthermore, the court read ARPA’s “critical and declining” language to focus on status in the 2020–2022 window, and rejected PBGC’s position that lack of ongoing “zone status” or prior termination automatically barred eligibility.

As a result, the PBGC’s Office of Inspector General (OIG) issued a 2025 risk advisory flagging that the appellate decision opens the door for 123 terminated plans to seek SFA (80 currently on the waitlist), 91 of which are terminated and insolvent and 32 that are terminated but not yet insolvent and have not received traditional financial assistance. The OIG estimates that if SFA is ultimately provided to that group, gross SFA exposure could be on the order of billions of dollars. But, just think about the American Workers that might eventually recoup their promised benefits.