By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Equity market participants were recently reminded of the fact that markets can fall, and unfortunately they usually don’t decline with any kind of notice. The impetus behind the markets’ most recent challenging day was the Fed’s relatively tame forecast for likely interest rate moves in 2025. There is no question in my mind that the nearly 4-decade decline in rates from lofty heights achieved in the early ’80s, when the Fed Funds Rate eclipsed 20%, to the covid-fueled bottom reached in early 2020, when the yield on the 10-year Treasury Note was at 0.5%, made bond returns a lot stronger than anyone’s forecast.

It certainly seemed that the US Federal Reserve provided the security blanket any time there was a wobble in the markets. This action allowed “investors” to keep their collective foot on the gas with little fear. Sure, there were major corrections during that lengthy period, but the Fed was always there to lend a hand and a ton of stimulus that propped up the economy and markets, and ultimately the investment community. As we saw in 2022, the Fed had run out of dry powder and ultimately had to raise US interest rates to stem a vicious inflationary spike. Rates rose rather dramatically, and the result was an equity market, as measured by the S&P 500, that declined 18% for the calendar year. Bonds faired only marginally better as rising rates impacted bond principals creating a collective -12.1% return for the BB Aggregate Index.

As we enter 2025, do we once again have a situation in which the Fed’s ability to reduce rates has been curtailed due to a stronger economy than anticipated? Will the continued strength and massive government stimulus drive inflation and rates higher? According to a blog post from Apollo’c CIO, here are his list of the potential risks and the probabilities:

Interesting that he feels, like we do at Ryan ALM, Inc., that the economy is likely to be stronger than most suspect (#6) leading to higher inflation, rising rates (#7), and a 10-year Treasury Note yield in excess of 5% (#8). That yield is currently at 4.6% (as of 3:06 pm).

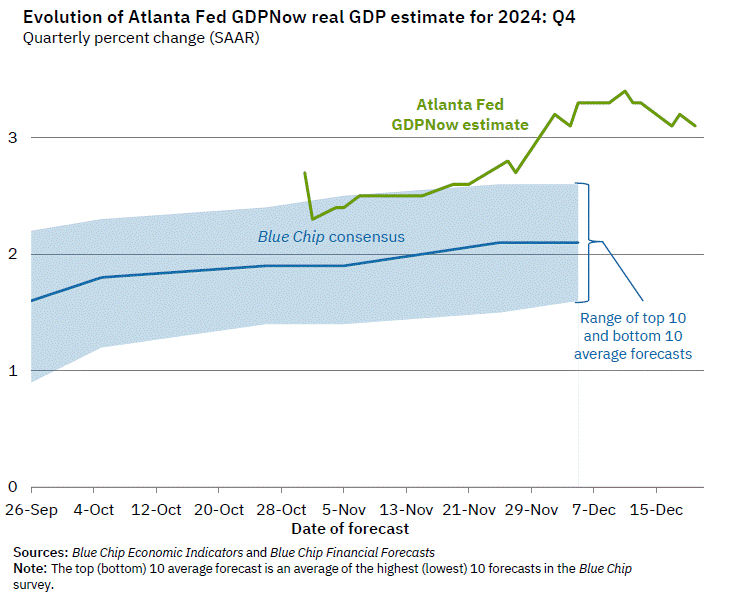

For those that might be skeptical, the Atlanta Fed’s GDPNow model is currently forecasting GDP growth for Q4’24 at 3.1% annualized. They have done a wonderful job forecasting quarterly growth rates. Their forecasts have consistently been above the “street’s” and as a result, much more accurate.

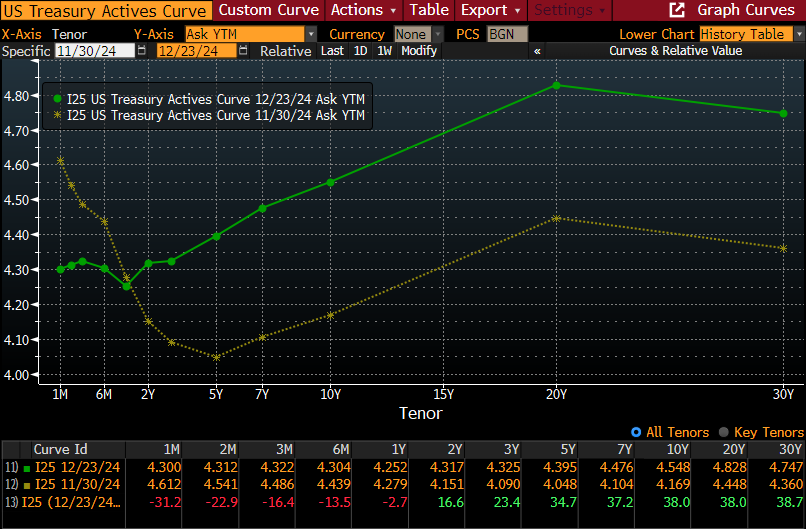

In addition, despite the third rate cut by the Federal Reserve at the most recent FOMC meeting of their benchmark Fed Funds Rate (-1.0% since the easing began), interest rates on longer dated maturities have risen quite significantly, as reflected below.

Rising US rates, stronger growth, and greater inflation may just be the formula for a significant contraction in equity valuations, especially given the current level. Be proactive. Reduce risk. Secure the promised benefits. Under no circumstance should you just let your “winnings” ride.