I penned the original post on 3/17. Why did it take this long for investors to realize that the Fed wasn’t kidding? US interest rates, particularly on the backend of the curve, have moved massively over the last two days. This move up in rates is far from done. The impact on our capital markets is just being felt. The first quarter for bonds was the worst one we’ve experienced since 1981. Total return bond programs will continue to get hurt. It is time to do something different or Pension America will suffer severe consequences.

Category Archives: Uncategorized

Pushing the Envelope

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

We’ve written about the asset allocation rollercoaster to uncertainty (ruin) and discussed the massive shift away from bonds toward riskier, less liquid assets that has transpired during the last 4+ decades and questioned frequently whether these moves have paid off for Pension America. We do know that contribution costs have risen and the volatility of returns has increased but we don’t truly know if the absolute returns generated have warranted this action.

While most of Pension America believes that the goal of a pension system is to achieve a return on asset target (ROA), we remain steadfast in believing that the primary goal must be the securing of the promised benefits in a cost-efficient manner and with prudent risk. Migrating a ton of assets into the alternative bucket certainly doesn’t meet the “in a cost-efficient and with prudent risk” smell test, let alone the securing of the promised benefits. The last decade of S&P 500 performance, which has been terrific, has likely masked some of what has been going on within alternatives, but the first quarter of 2022 is about to deliver a kidney punch the likes we haven’t felt in roughly 20 years.

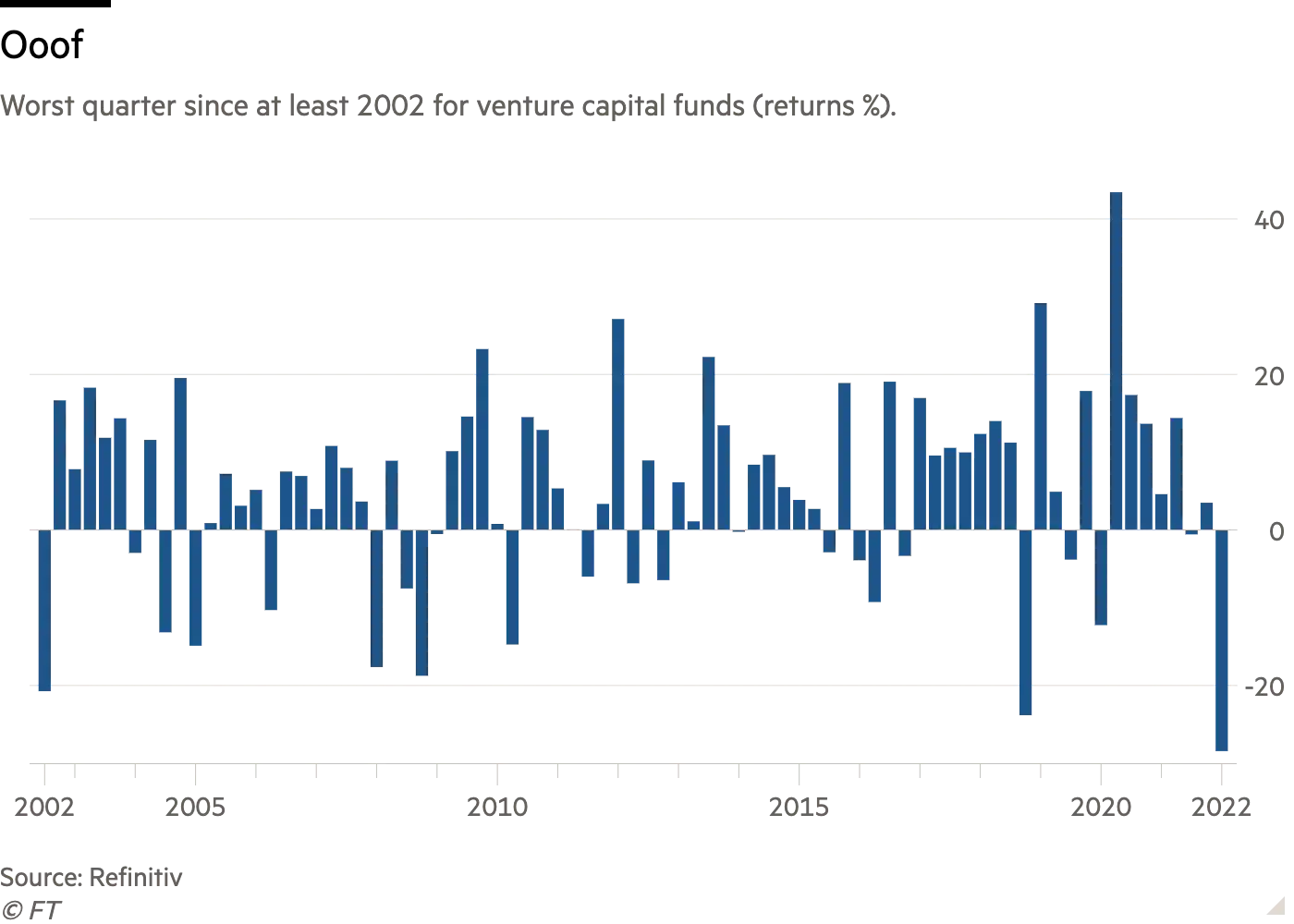

The FT has published the following chart that was produced by Refinitiv.

Ooof is such a great word to describe what has just transpired. Most followers of the markets knew that Q1’22 was challenging for public equity markets, especially growth-oriented stocks, and of course bonds, as the Federal Reserve finally got serious about addressing our runaway inflation, but who really knew what was going on under the radar of private markets? I certainly didn’t. The first quarter return for Venture Capital (VC) is atrocious. Furthermore, according to the FT “at the end of last year, 70 percent of so-called growth investors — in between early-stage venture capital funds and private equity investors that target mature companies — said they expected valuations to hold steady or rise, according to a survey of the top 25 investors in the field by Numis. Now, 95 percent of investors anticipate offering lower valuations in the coming 12 months — an abrupt shift for the fastest-growing corner of the private capital industry.” Lower than what has already been witnessed? WOW!

We’ve been encouraging plan sponsors to adopt a bi-furcated asset allocation (liquidity and growth buckets) for this very reason. Most alternative investments need time in order to meet their long-term expectations, but at the same time plan sponsors need liquidity to meet the monthly benefits and expenses. Separating the plan’s assets into two buckets improves the plan’s liquidity to meet the Retired Lives Liability, while the growth portfolio generates the necessary return to meet the plan’s future liabilities. Putting too many eggs in the growth portfolio without addressing the plan’s need for liquidity could exacerbate any downward price movements for assets during periods of dislocation.

Rising interest rates, outsized inflation, stretched valuations, supply chain disruptions, and a war whose outcome is far from known is not a great combination for the asset side of the pension ledger. Now is the time to pay much more attention to the plan’s liabilities. Measure, monitor, and manage plan liabilities with the aim of SECURING them, and your plan’s economic future is more certain.

It Has the Potential, but it Isn’t All Bad News!

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

“The Lost Decade”, a phrase originally used to describe Japan’s economic performance during the 1990s, has been recently showing up in story after story in the financial press. In fact, Stifel’s chief equity strategist, Barry Bannister, has said that investors should prepare for the likelihood of a lost decade ahead with returns of 0% in the US stock market from the end of 2021 through the end of 2031. This of course follows a decade when the S&P 500’s compounded annual rate of return was more than 13% during the 2010s. We’ve had a number of booms and busts for decades which isn’t surprising given that regression to the mean tendencies is very prevalent in our markets.

Furthermore, with the prospect of an aggressive US Federal Reserve raising interest rates to combat the current unrelenting inflation you have the potential to have the US bond market possibly generating similar results as those predicted by Bannister for US stocks. Given the focus of Pension America on the return on asset assumption (ROA), you have a formula for disaster when two major asset classes each have the possibility of generating annualized returns below long-term expectations. In addition, a rising rate environment has the potential to harm the US real estate market which has seen housing and rental costs soar since 2018.

Given this potential scenario, are pension plans soon to witness funded ratios that plummet, and contribution expenses accelerate upwards? Quite possibly. Is there anything that can be done to mitigate these potential outcomes? Sure! First, let us share some possibly good news. Given the US accounting rules (GASB) that permit plan sponsors (and their actuaries) to use the plan’s ROA as the liability discount rate, changes in the economic or market present value of a public pension plan’s future liabilities are hidden from view. The 39-year bull market in bonds that may have recently come to an end crushed pension funding, as liability growth far outpaced asset growth during that timeframe. If we are to experience a rising rate environment, the economic or market present value of those future promises will fall. Given the average duration of pension liabilities of roughly 12 years and you have the potential for “returns or growth rate” to be quite negative for pension liabilities.

In a rising rate environment that has the economic present value of future liability payments falling, asset growth doesn’t have to achieve the ROA. For every 1% rise in US rates, the impact on the average pension plan (with a 12-year duration) would have liability economic growth fall 12% before the yield is added back in. A zero percent return on the plan’s total asset portfolio would look amazingly good relative to negative liability economic growth. However, this potential scenario doesn’t mean that plan sponsors should do nothing. In fact, restructuring one’s asset allocation in anticipation of a potential lost decade is a must. We highly recommend bifurcating the plan’s assets into liquidity (beta) and growth (alpha) buckets.

The liquidity bucket is going to be the plan’s bond exposure. In a rising rate environment, traditional return-focused bond programs with long maturities are going to get hurt. Convert return-seeking fixed income into a cash flow matching strategy that uses bonds for their cash flow generating capability (both principal, income, and cash flow reinvestments). These asset cash flows should be optimized to match and fund the plan’s liability cash flows. Importantly, this strategy will eliminate interest rate risk (since it is matching liability future values) for that portion of the portfolio that is optimized. Once that step has been completed, your pension plan’s alpha bucket will enjoy an investing horizon that has been extended.

This buying of time is an important investment tenet. Allowing the alpha bucket (non-bonds) to grow unencumbered is critical, as market performance may be quite choppy as we look 10-years out. One doesn’t want to force liquidity where it may not naturally exist, especially given that America’s public pension systems have moved significant assets into private markets during the last couple of decades. This strategy is like a bridge over troubled waters. We witnessed very challenging equity markets during the first decade of this century. Unfortunately, the equity market declines were coupled with a significant fall in US interest rates. This combination proved to be crushing for Pension America’s funded status. Perhaps our pension systems will suffer less of a hit in this next environment if rates rise substantially and liability growth falls. Don’t close your eyes to this potential reality. Measure, monitor, and manage your plan’s liabilities much more frequently than the current practice of seeing those promises only once per year, at most.

Misleading Indicators

By: Ronald J. Ryan, CFA, CEO, Ryan ALM, Inc.

The Commerce Department reports with some glee that sales and income figures show an easing up of the rate at which business is easing off, which is taken as proof that there is a slow down as well as a noticeable slowing up of a slowdown.

In order to clarify the cautious terminology of the experts, it should be noted that a slowing up of the slowdown is not as good as an upturn in the down curve, but it is a good deal better than either a speedup of the slowdown or a deepening of the down curve, and it does suggest that the climate is about right for an adjustment to the readjustment.

Turning to unemployment, we find a definite decrease in the rate of increase, which clearly shows that there is a letting up of the letdown. Of course, if the slowdown should speed up, the decrease in the rate of increase of unemployment would turn into an increase in the rate of decrease of unemployment. In other words, the deceleration would be accelerated.

But the indicators suggest a leveling off, referred to on Wall Street as a bumping along rock bottom. This will be followed by a gentle pickup, then a faster pickup, a slowdown of the pickup, and finally a leveling off again.

It is hard to tell before the slowdown is completed, whether a particular pickup is going to be fast. At any rate, the climate is right for a pickup this season, especially if you are about twenty-five, unmarried, and driving a red convertible.

It’s April 1… don’t be fooled!

ARPA Update as of 3/31/22

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

I’m pleased to report that the PBGC yesterday announced that another pension system’s SFA application has been approved. Teamsters Local 641 Pension Plan, which originally filed for the SFA on September 9, 2021, only to have to withdraw and resubmit another application on December 1st, will receive $503.9 million. The plan, based in Union, New Jersey, covers 3,610 participants in the transportation industry.

According to the PBGC’s press release, “Local 641 Plan became insolvent in March 2021. At that time, PBGC started providing financial assistance to the plan. As required by law, the Local 641 Plan reduced participants’ benefits to the PBGC guarantee levels, which was roughly 55 percent (my emphasis) below the benefits payable under the terms of the plan. PBGC’s approval of the SFA application enables the plan to restore all benefit reductions caused by the plan’s insolvency and to make payments to retirees to cover prior benefit reductions.” This development is sure to put a smile on the faces of the 3,610 participants who have been forced to “live” with a benefit that was roughly half of that with which they were entitled.

In other SFA news, there have been NO additional applications filed since March 16th, only two applications were filed last month, and only three have been submitted since January. That pace is comparable to the number of plans that have received SFA approval from the PBGC which stands at three since January 24th. At this point, not all of the eligible Priority Group 1 and 2 plans have filed the SFA application. Priority Group 3 plans (plans with >350,000 participants) are eligible beginning today (4/1) and that’s no April Fool’s joke. Perhaps we’ll get the Final, Final Rules from the PBGC before Priority Group 4 candidates are slated to file beginning on 7/1/22.

How Ugly? Quite!

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

The inflationary environment and the impact of Federal Reserve tightening are combining to create a challenging environment for traditional fixed income core mandates – the significant majority of fixed income exposure among public and multiemployer pension systems. The year-to-date performance for the Bloomberg Barclays Aggregate index reveals a -6.3% return through yesterday’s market close (3/29). As we’ve pointed out on several occasions, fixed income market participants have enjoyed quite the run during the last 39-year bull market. But the party may have just received the final call. So, just how bad is the nearly completed first-quarter return? It is ugly.

Since 1980, the Aggregate index has declined only 4 times on an annual basis. Four times in 42 years! The most significant annual decline was only -2.92% (1994), or <50% of the decline observed during the first three months of 2022. The worst quarter during this extraordinary period was -4.1% (quarter ending 9/81). This shouldn’t come as a major surprise to anyone who regularly reads this blog, as we’ve been saying for quite some time that the current inflationary environment would lead to Fed tightening AND that this action would also be quite bad for traditional bond management. Given that the US Federal Reserve has indicated future interest rate increases at each of the remaining FOMC meetings for 2022, the interest rate rise witnessed to date is only a small deposit of what’s to come.

We strongly encourage plan sponsors and their advisors to refocus their plan’s fixed-income away from a return-seeking mandate to one that uses bond cash flows to match and fund the plan’s liability cash flows (benefits and expenses). This action will ensure that the portion of assets used to defease the plan’s liabilities will move in lockstep. We don’t know the magnitude or duration of a potential interest rate increase, but we certainly have history to guide us. Prior to the astonishing 39-year bull market, we suffered through a 30-year bear market that was accompanied by high inflation, oil shocks, political instability, and significantly rising US interest rates. Sound familiar?

It Should Have Been A Warning!

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

A former colleague has for years provided me with an excellent monthly performance report from a terrific regional asset consulting firm. What had been a 7-8 page document of equity and fixed income indexes became a 5-page document in the middle of 2021. I was taken aback by the absence of the fixed income index section. I reached out to my former colleague and was told that “no one” was interested in fixed income so those indexes were removed by the consulting firm. Wow! I was shocked given the role that bonds play in all types of investment programs, especially corporate DB plans. I remember saying to myself that those that aren’t interested today might certainly be in a few months when interest rates start to rise.

Well, that period is upon us and the returns to a variety of fixed income benchmarks YTD are painful, and likely to get even more so if the US Federal Reserve can’t successfully navigate through this inflationary environment. After 39-years of a bond bull market, it is time to pay the piper. This benign neglect had me recall all of the “talk” in the late 1990s about a new paradigm. As you may recall, Value investing was dead and the only play in town was to invest in high momentum growth stocks. We all know what soon followed. Sound reminiscent of today’s environment?

Our markets move in cycles, such as Value versus Growth, large-capitalization stocks versus small caps, the US versus non-US, and on and on. Some of the cycles are longer than others, such as the US interest rate bull market cycle of nearly 40 years others are much shorter. These cycles are driven by market sentiment and cash flow. The building or unwinding of positions/strategies leads to strong or weak performance. This is how it has always been, and it will remain so. When it becomes so painful to maintain an exposure it is usually the time to double down not abandon ship.

Because of the nearly singular focus on return (ROA) as the primary objective in managing a DB pension plan, sponsors and their advisors have for years significantly expanded their use of equity and equity-like products. What this has done is increase both the cost of managing a plan and the volatility surrounding the potential outcomes. It has done very little to ensure success. If a pension system achieves the targeted ROA but fails to beat liability growth has the plan won? Of course not. But given that many sponsors (and their advisors) don’t know how their plan’s liabilities are behaving on a daily, monthly, or quarterly basis they are blind to whether or not their fund is meeting the primary pension objective of SECURING the promised benefits at a reasonable cost and with prudent risk.

I would suggest that now IS NOT THE TIME to close a blind eye as to how the fixed income market is performing. Traditional return-focused fixed income products are going to get hammered if the Fed isn’t successful in migrating through this inflationary environment. Use bonds for their cash flows and carefully (skillfully) match those asset cash flows with the plan’s liability cash flows to secure the promised benefits. There are many benefits from restructuring the fixed income allocation including improving the plan’s liquidity profile, removing interest rate risk from that portion of the pension plan, while also extending the investing horizon (buy time) for the plan’s other assets to now grow unencumbered. Many in our industry haven’t had to manage through a rising interest rate environment that lasted more than a few quarters. It is a new day! Are you prepared?

ARPA update as of March 25th

Here’s the latest from the PBGC through March 25th. Last week witnessed zero new applications, zero new approvals, zero disbursements of the SFA, and zero applications withdrawn. So much for progress! But who can blame the PBGC, as March Madness has clearly gripped everyone? Perhaps the folks at the PBGC are a bunch of St. Peter’s alum?

So, we remain at seven approved applications with five having received their SFA ($1.1 B). Total applications still in review remain at 26, with U.T.W.A. – N.J. Union – Employer Pension Plan having been the last application submitted on March 16th. As a reminder, the big boys, those plans with >350,000 participants, are eligible to begin filing under Priority Group 3 status beginning April 1st.

There have been only four of the 18 MPRA suspension plans filing an application for the SFA. Priority Group 2 candidates became eligible on December 31, 2021. Are they waiting for the “Final, Final Rules” from the PBGC, or are there other extenuating circumstances that have created this delay? Only time will tell, but I can only imagine the angst that this further delay is giving to participants in those plans. Stay tuned!

This Doesn’t Make Sense – Now What?

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Earlier today I published a post titled, “This Doesn’t Make Sense”, in which I questioned the current market action for US equities (especially large-cap growth stocks) given the great uncertainty associated with the Russian invasion of Ukraine, rising interest rates, decades high inflation, oil prices exceeding $113/barrel, supply chain issues that continue to cause delays, and equity valuations that remain stretched. Several regular readers of this blog provided positive feedback on the post (thank you), but many others asked the question: “Now what?” It is a great question that deserves an appropriate response.

As Ron Ryan and I have stated on many occasions, the primary objective in managing a DB pension plan is to SECURE the promised benefits in a cost-efficient manner and with prudent risk. It is NOT a return objective (ROA). Given this goal and the current economic environment, it would behoove plan sponsors and their consultants to quickly migrate from traditional total return focused fixed income into a cash flow matching strategy in which bonds are used for the certainty of their cash flows (income and principal) to match and fund liability cash flows (Liability Beta Portfolio™). In a rising rate environment, total return bond programs will generate negative returns. If a 1% real return were to be achieved (historically bonds produce 1-2% real returns above inflation) in this current fixed income environment, a 6-year duration bond would generate a return of -35% or worst.

Once a cash flow matching strategy has been implemented, your bond allocation will move in lock-step with the fund’s Retired Lives Liability. This strategy eliminates interest rate risk, as you are now defeasing a future value that is not interest-rate sensitive. Ideally, the allocation should provide 10-years of benefits and expenses coverage (improved liquidity management). If achieved, you have now built an expanded investing horizon (a bridge over troubled waters), for the remainder of your assets (Alpha assets) to grow unencumbered.

Most public pension systems (and multiemployer plans) have dramatically increased their plan’s exposure to risky assets during the last couple of decades as bond yields fell. That strategy has certainly created the potential for more return, but it has guaranteed more volatility and higher costs. In addition, it has impacted liquidity as many of these strategies are locked up in funds that have 10-12 year lives. Creating a bifurcated asset allocation of liquidity assets (Beta) and growth assets (Alpha) that secures the promised benefits, improves liquidity to meet those benefits, extends the investing horizon for the plan’s alpha assets to work through choppy markets, while also eliminating interest rate risk for the portion of assets that are defeased seems like a most prudent strategy to adopt given all of the uncertainty within our capital markets. This recommendation isn’t knee-jerk! It is an asset allocation model with a long and successful history! Putting in place an asset allocation structure that provides the necessary protections WHEN markets go awry is fundamental to the success of DB pension systems. For too long we’ve played the return game. Very few plans are well-funded. Isn’t it time for a return to pension basics?

This Doesn’t Make Sense!

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

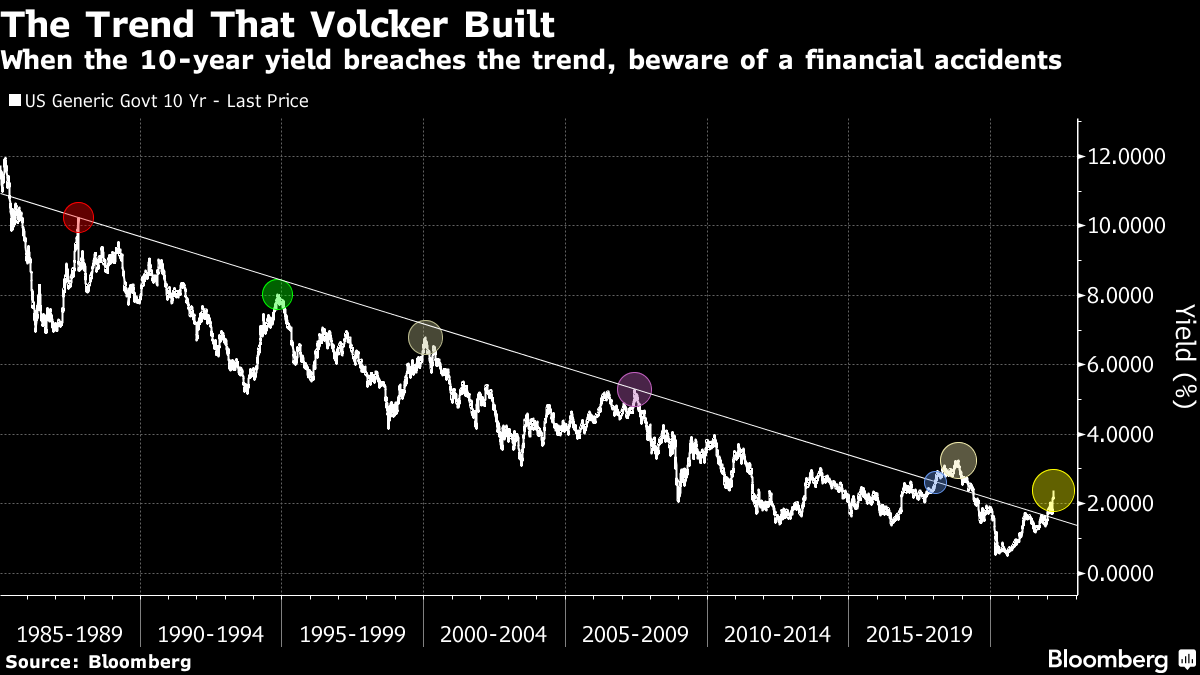

I’ve witnessed quite a lot during my forty years in this business, but I’ve never seen anything quite like that which I’ve seen during the last couple of weeks. Given the current economic backdrop (high inflation and rising rates) coupled with the great uncertainty regarding the Russian invasion of Ukraine, stocks should not be rallying to the extent that they have relative to the performance of US Treasuries. I’ve previously referenced John Authers, Bloomberg, for the great work that he does in bringing clarity to confusing times through the presentation of impressive charts and graphs (some his and some borrowed). I’m borrowing one of his today to highlight the inconsistency in the equity market performance.

As John highlights and as we’ve pointed out on numerous occasions, our equity markets have been benefiting tremendously from the accommodative monetary policy since Volcker was the Fed Chair. The circles on the chart above highlight points in time when it looked like the downward trend in rates (10-year US Treasury note yield) was about to be reversed through Fed tightening. In each case, something dramatic occurred in the markets, such as the 1987, 2000, 2018 stock market crashes that forced the US Federal Reserve to once again provide easy money. The Fed was able to accommodate markets during those extraordinary occurrences because inflation was well-contained.

Today, we have consumer inflation at nearly 8% and producer inflation at almost 10%. There is little opportunity for the Fed to provide additional stimulus without seeing our current inflationary environment further spiral out of control. Given that the Fed has already indicated that it will move aggressively (potentially 6 more Fed Funds increases) to contain inflation providing stimulus should equity markets break is a non-starter. We know that rising interest rates will harm the performance of bonds, but as we witnessed during the 1970s, equities will also have great difficulty providing a real return in a high inflationary environment.

Most public pension systems are underwater from a funding standpoint despite strong equity markets since the Great Financial Crisis. We cannot allow the funded status to deteriorate further, which will lead to greater contributions, especially if the higher interest rates eventually lead to a recession. Asking taxpayers to provide additional funding for these plans during an economic downturn may just be the death knell for public pensions.