By: Russ Kamp, Managing Director, Ryan ALM, Inc.

We’ve written about the asset allocation rollercoaster to uncertainty (ruin) and discussed the massive shift away from bonds toward riskier, less liquid assets that has transpired during the last 4+ decades and questioned frequently whether these moves have paid off for Pension America. We do know that contribution costs have risen and the volatility of returns has increased but we don’t truly know if the absolute returns generated have warranted this action.

While most of Pension America believes that the goal of a pension system is to achieve a return on asset target (ROA), we remain steadfast in believing that the primary goal must be the securing of the promised benefits in a cost-efficient manner and with prudent risk. Migrating a ton of assets into the alternative bucket certainly doesn’t meet the “in a cost-efficient and with prudent risk” smell test, let alone the securing of the promised benefits. The last decade of S&P 500 performance, which has been terrific, has likely masked some of what has been going on within alternatives, but the first quarter of 2022 is about to deliver a kidney punch the likes we haven’t felt in roughly 20 years.

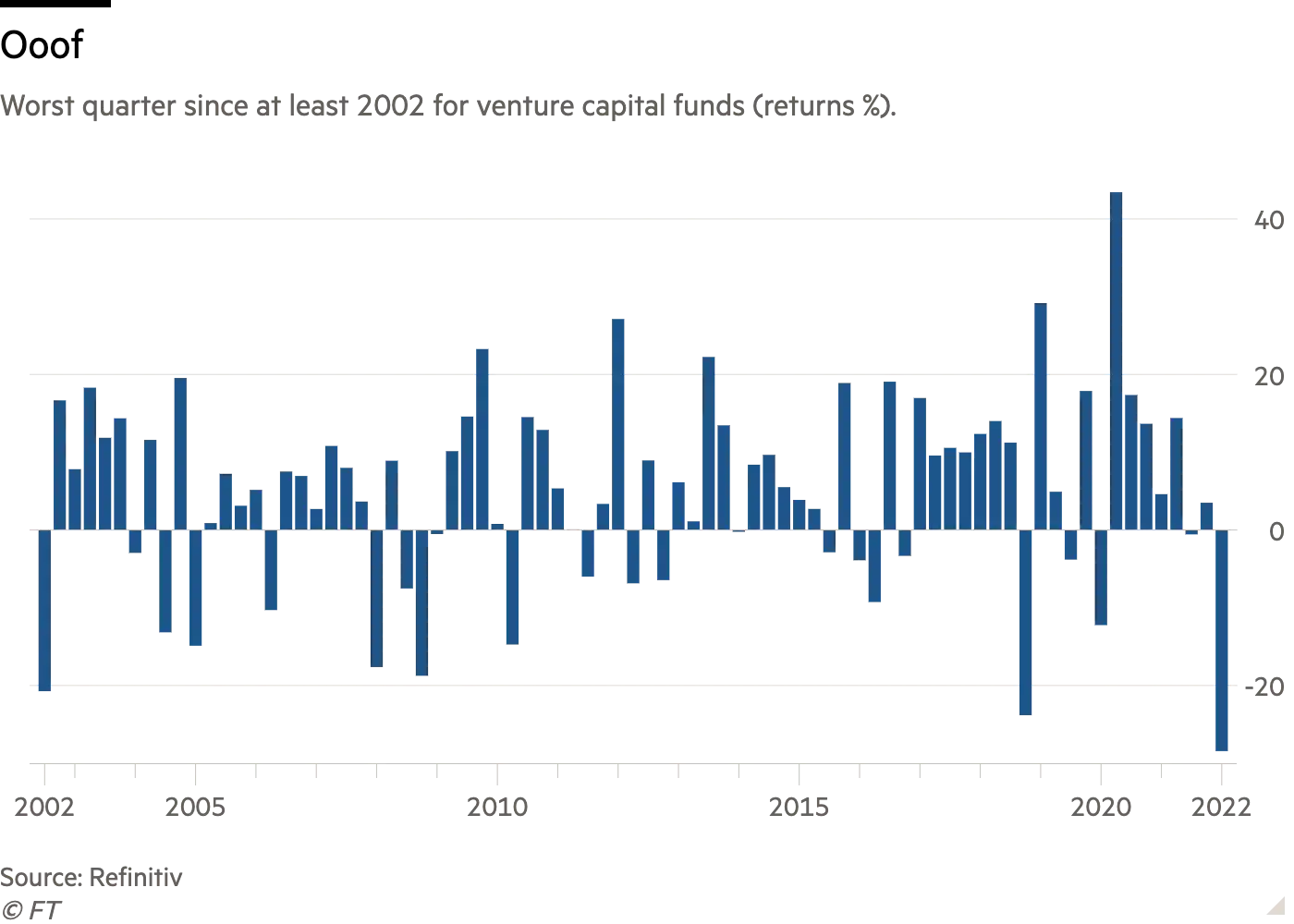

The FT has published the following chart that was produced by Refinitiv.

Ooof is such a great word to describe what has just transpired. Most followers of the markets knew that Q1’22 was challenging for public equity markets, especially growth-oriented stocks, and of course bonds, as the Federal Reserve finally got serious about addressing our runaway inflation, but who really knew what was going on under the radar of private markets? I certainly didn’t. The first quarter return for Venture Capital (VC) is atrocious. Furthermore, according to the FT “at the end of last year, 70 percent of so-called growth investors — in between early-stage venture capital funds and private equity investors that target mature companies — said they expected valuations to hold steady or rise, according to a survey of the top 25 investors in the field by Numis. Now, 95 percent of investors anticipate offering lower valuations in the coming 12 months — an abrupt shift for the fastest-growing corner of the private capital industry.” Lower than what has already been witnessed? WOW!

We’ve been encouraging plan sponsors to adopt a bi-furcated asset allocation (liquidity and growth buckets) for this very reason. Most alternative investments need time in order to meet their long-term expectations, but at the same time plan sponsors need liquidity to meet the monthly benefits and expenses. Separating the plan’s assets into two buckets improves the plan’s liquidity to meet the Retired Lives Liability, while the growth portfolio generates the necessary return to meet the plan’s future liabilities. Putting too many eggs in the growth portfolio without addressing the plan’s need for liquidity could exacerbate any downward price movements for assets during periods of dislocation.

Rising interest rates, outsized inflation, stretched valuations, supply chain disruptions, and a war whose outcome is far from known is not a great combination for the asset side of the pension ledger. Now is the time to pay much more attention to the plan’s liabilities. Measure, monitor, and manage plan liabilities with the aim of SECURING them, and your plan’s economic future is more certain.