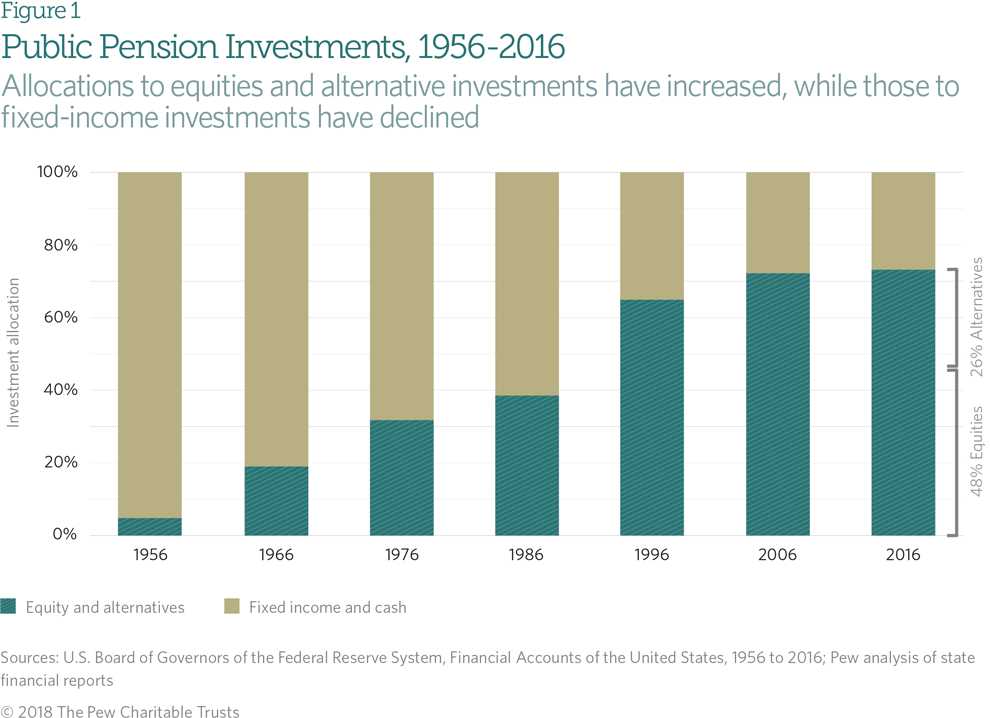

As the chart below depicts, there has been a massive shift in the asset allocation of DB plans since the mid-50s from mostly fixed income allocations to significant exposure to risk assets.I suspect that most of the motivation has been driven by the plan sponsors desire/need to achieve a target return or hurdle rate (ROA). The idea is if the ROA is achieved then contribution costs remain as projected…but has this goal been achieved?

Actuaries do a wonderful job (very difficult task) of forecasting the plan’s liabilities despite ever changing inputs, such as life expectancy, which fortunately has expanded leaps and bounds since the 1950s. I often say that my crystal ball is no better than anyone else’s if not worse. Actuaries can’t afford to have a crystal ball that is foggy. Their forecasts of future benefit costs are amazingly accurate despite the many inputs that drive their calculations. Given the reliability of their data and the importance of meeting those future expenditures, why aren’t plan sponsors and their consultants using these insights to drive asset allocation and investment structure decisions?

Most DB plans were well overfunded in 1999. They had the opportunity to remove substantial risk from their portfolios by defeasing the plan’s Retired Lives Liabilities and securing the funded status. To achieve the ROA, asset allocation models did the opposite! As a result, their increased equity exposure got crushed when significant market corrections occurred in 2000-02 and again in 2007-09. Did we learn anything? It doesn’t appear that we did, as equity exposures continue to ratchet higher despite the appearance of dramatic overvaluation. Could it be that fixed income, after an historic 39-year bull market, scares plan sponsors and their consultants to a greater extent? Could be. However, as we’ve stated on several occasions, bonds should not be viewed as performance or Alpha assets in this environment. They should be used exclusively for the certainty of cash flows that they generate as liquidity assets or Beta assets.

We believe that a cash flow matching implementation that defeases a plan’s net benefit payments chronologically from next month’s needs to as far out as the allocation will permit will provide many benefits, including: 1) improved liquidity, 2) elimination of interest rate risk on the bonds that are used to defease liabilities, 3) buys time for all of the equity exposure now in DB plans, and 4) allow the alpha assets (non-bonds) to grow unencumbered, as the re-investment of dividends is critical to the long-term success of investments, such as the S&P 500.

Increasing equity exposure in the hope that a greater return will reduce the need for future contributions hasn’t yet proven to be true. It has ensured that total expenses (management fees) have gone up, as well as the overall volatility of the funded status, but success hasn’t been guaranteed. Given where valuations currently reside, either dramatically reduce the equity exposure or reconfigure your fixed income exposure from a total return seeking mandate to a cash flow matching implementation that now allows time for the alpha assets to recover after the next equity market correction. There will be one.

Pingback: Pushing the Envelope – Ryan ALM Blog