By: Russ Kamp, Managing Director, Ryan ALM, Inc.

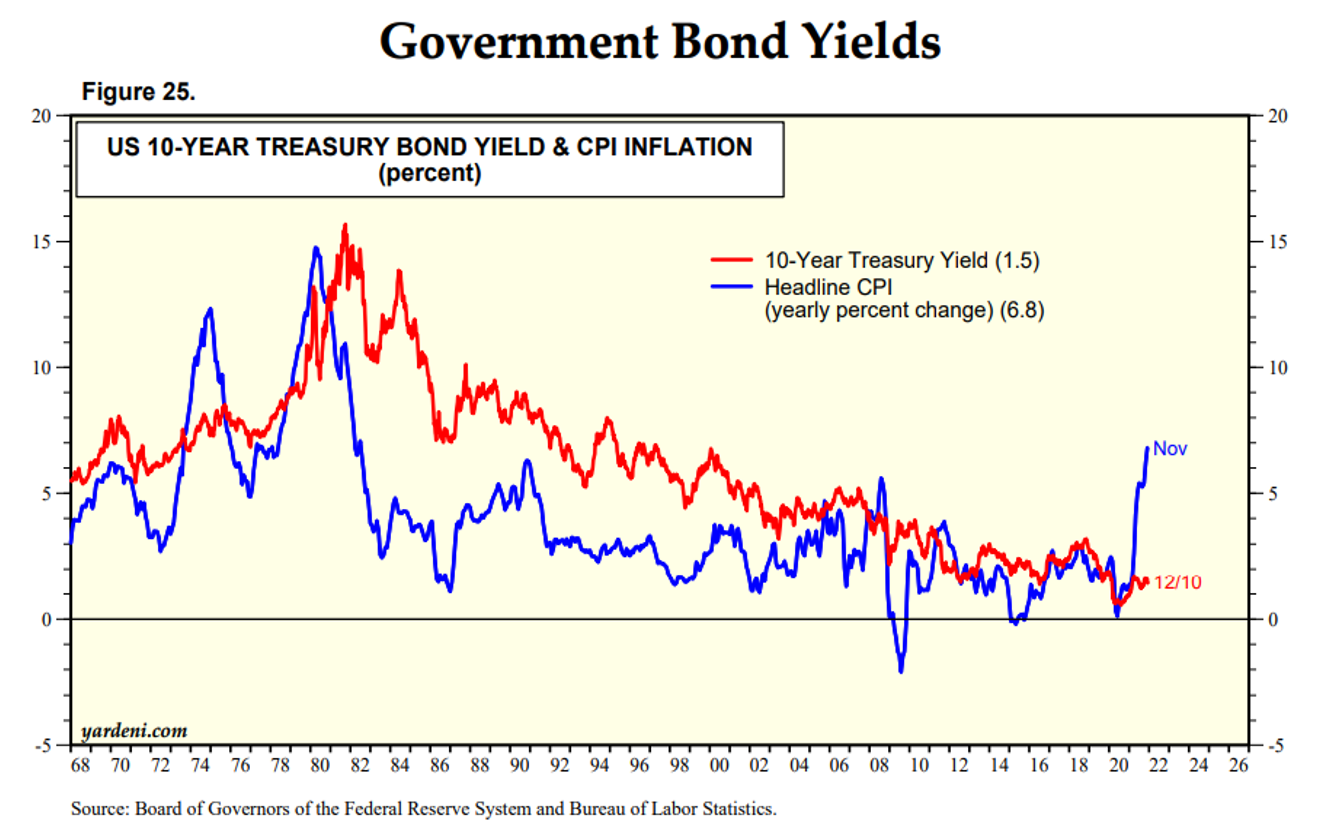

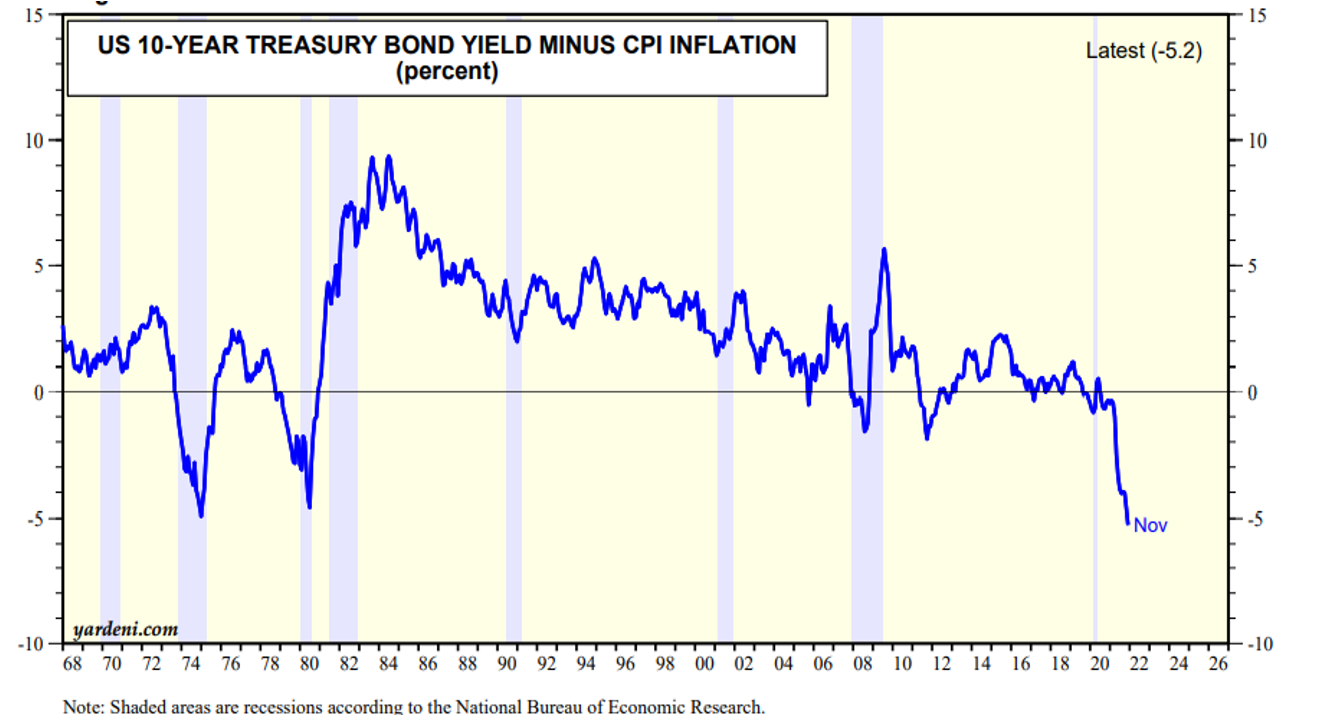

The 1970s were one of the most challenging times for our capital markets. The decade began somewhat harmlessly although equity valuations were inflated following incredibly strong equity markets during the 1960s. These stretched valuations would eventually produce the infamous “Nifty Fifty” stocks, including IBM, Xerox, Coca Cola, and other large-cap stocks whose P/E multiples approached levels not seen to that point with many reaching and exceeding 100 X earnings. The Nifty Fifty bubble burst in 1973 as the US grappled with political unrest (Nixon), an oil embargo, and rising inflation and interest rates. Increases that would eventually produce double-digit short- and long rates. Is it time to once again quote Yogi Berra? Is it “deja vu all over again”?

For those who have studied the 1970s, it was an incredibly painful decade, which some market historians describe as a “lost decade” from a performance standpoint. Pension plans that had adopted a more traditional 60%/40% mix of equities/bonds were particularly hit hard as bonds produced a negative return, while equities squeaked out marginal gains. As a result, most pension systems fell far short of their plan’s return on asset assumption (ROA) creating a situation in which escalating contribution expenses were needed to close the funding gap created by this exceptionally poor performance period.

Goldman Sachs has produced a very interesting chart highlighting 1-year and 10-year drawdowns for a 60/40 implementation.

I was not only shocked to see the magnitude of the performance shortfall during the decade of the ’70s but also the duration. From the mid-’70s to the early ’80s the standard 60/40 asset mix got crushed. Given our current economic and political landscape, is it too far-fetched to conclude that we may just be looking at the ’70s once again? Don’t we have massive inflation, a Fed that has telegraphed significant interest rate increases, oil trading at nearly $110/barrel, a war whose outcome is far from known, a speculative real estate market, and equity valuations that remain significantly elevated? What’s the difference?

Pension plans that don’t protect themselves are doomed to repeat the failures of the past. Why allow your current asset allocation to damage your plan’s funded status leading to significant growth in contributions? Now is the time to bifurcate your assets into two buckets – liquidity (Beta) and growth (Alpha). Convert your current fixed income from a return-seeking strategy to one that will use bonds for their cash flows to meet liability cash flows (benefit payments). Adopting this strategy allows the alpha assets to grow unencumbered for the period of time covered by the Beta assets. Buying time will enable the portfolio to work through unsettling market conditions. Public pension fund contributions have grown tremendously during the last two decades. Taxpayers, many of whom don’t have access to a traditional pension plan, may be opposed to seeing their tax $s continue to be used to fund retirement benefits that they themselves lack. We are in the early stages of the Fed’s interest rate increases. Now is the time to act before it is too late.