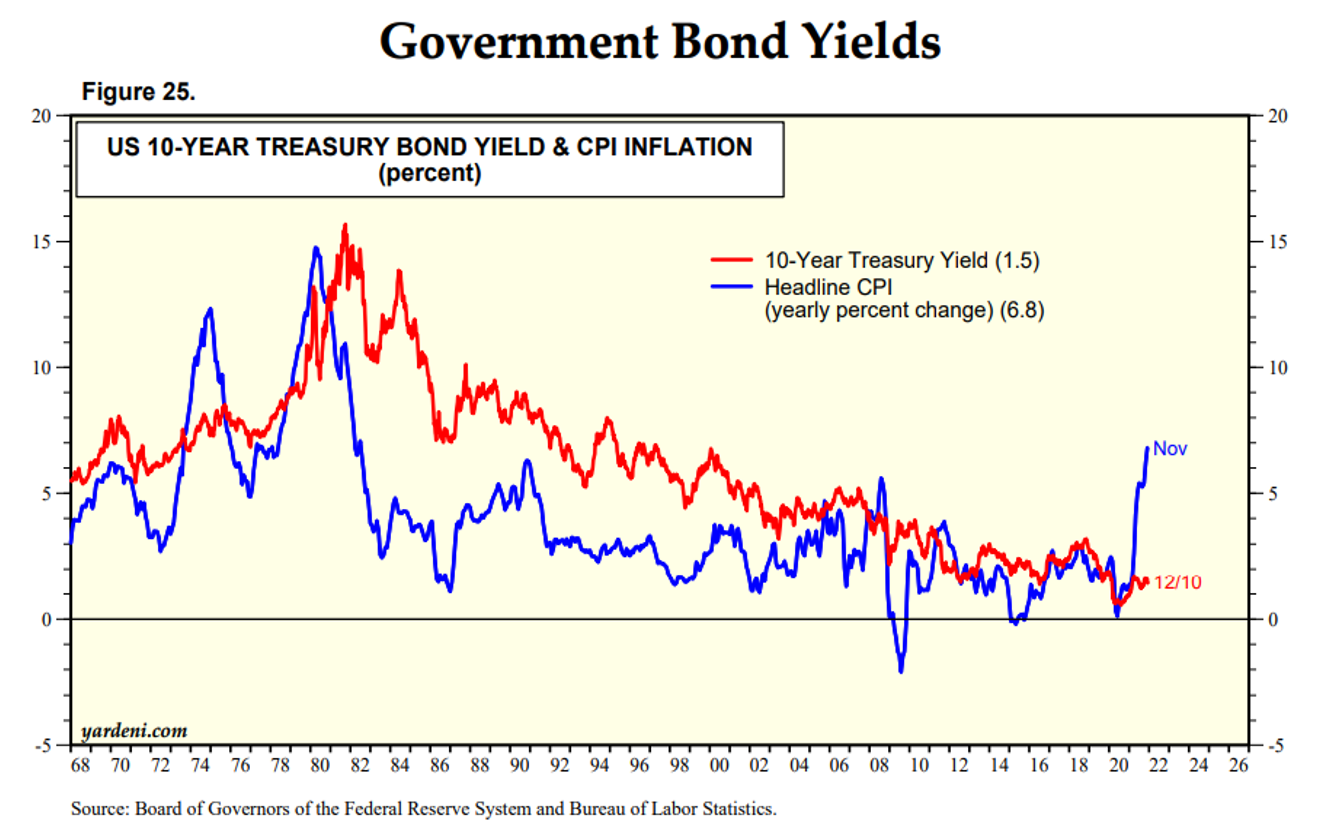

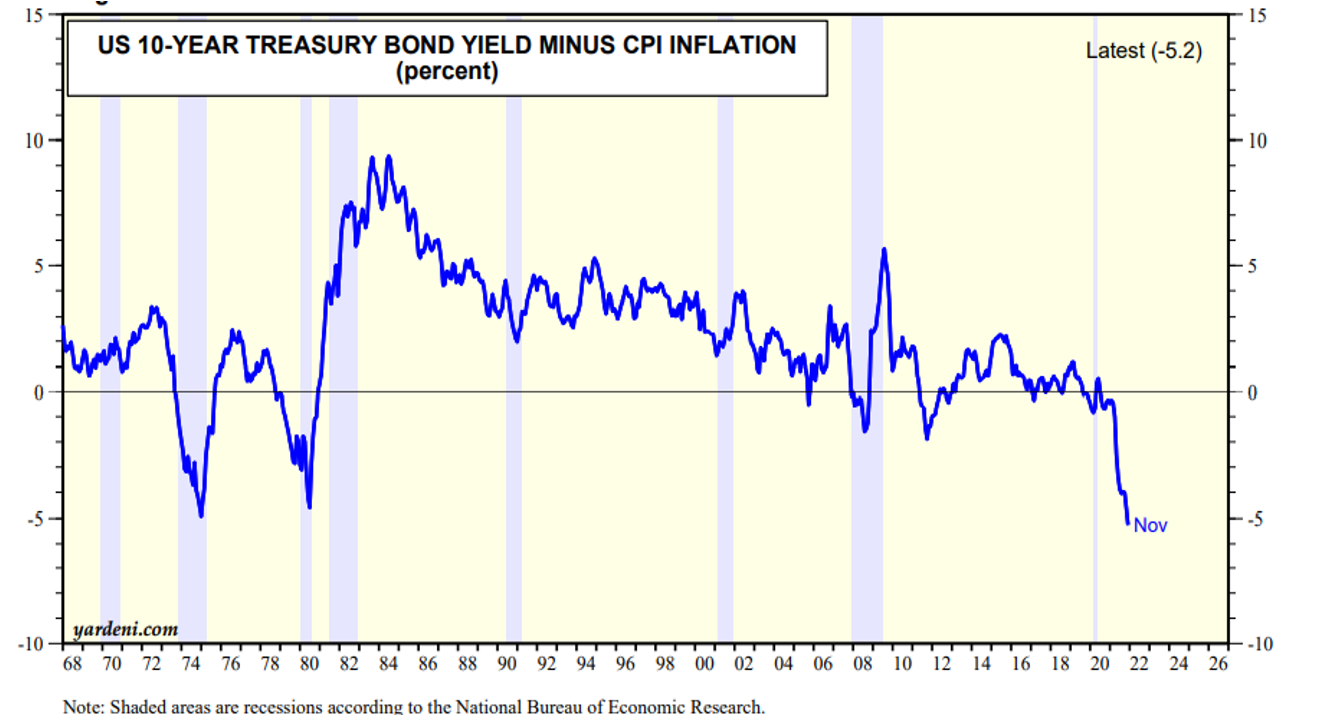

The Bloomberg survey for the 4th quarter of 2022 has the US 10-year Treasury Note yield projected to be 2.25%. The 10-year is currently trading at 1.995% (3/10 at 11:20 am EST). That doesn’t seem to be much of a forecasted increase given today’s announcement that the CPI was recorded at 7.9% and recent trends indicate that the CPI has a high probability of hitting 10% before it resumes a path lower. If the CPI # proves accurate, how is it possible that the 10-year Treasury Note yield is only going to be 2.25% in the fourth quarter? As the chart below highlights, bond investors have demanded a premium real yield with few exceptions, which tend to be short-lived.

As we’ve indicated in previous blog posts, the 39-year bull market in bonds is likely over. An interest rate rise will put pressure on total return bond programs. It only takes a 30 basis points rise in rates for a 7-year duration bond to have a negative return for the year. That isn’t much of a buffer, especially since we’ve witnessed 30 bps moves on a fairly regular basis.

If predictions hold that we post a 10% CPI during this rampant inflationary environment, a 2.25% yield on the 10-year would equate to a negative real return of 7.75% or roughly 50% more than the previous low in real yields. Why would investors accept this condition? Rising rates will help reduce the present value of your plan’s liabilities, but it will also impair your assets. Why take the risk that asset level falls greater than your plan’s liabilities? Match asset cash flows with liability cash flows to help secure the promised benefits and reduce funding volatility while controlling contributions. DB pension systems are too critically important to allow chance to dictate future outcomes.