Unlike any other asset class, fixed income (bonds) have two risk/reward values:

- Total Return

- Certain Cash Flows

Total Return Value

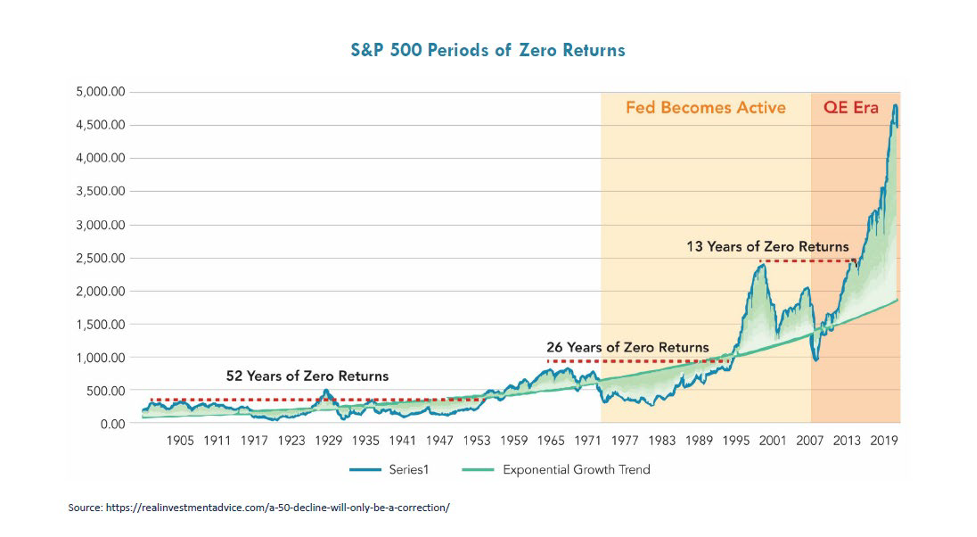

The total return value in bonds is the converse of interest rate movements. When rates go down, as they have from 1981 to 2021, they produce price appreciation and higher total returns. And the opposite happens when rates go up as they did from 1953 to 1981.

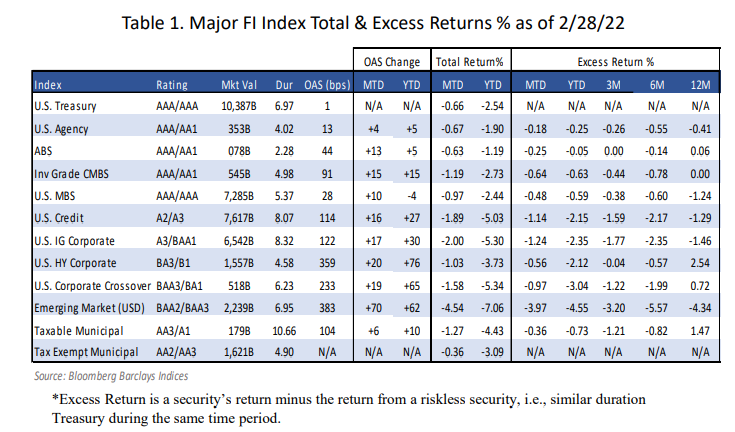

Since the start of 2022, interest rates have trended upward causing negative bond returns (BB Aggregate Index -3.25% YTD thru 02/28/22 ). Given the current inflation rate of over 7.0% on the CPI and over 9.0% for the PPI, coupled with the expectation that the Fed will raise short rates several times this year… this interest rate trend to higher rates should continue. As a result, pensions should expect negative fixed income returns this year and for the foreseeable future.

Certain Cash Flow Value

If you buy bonds for their intrinsic value (certainty of cash flows) you will immunize or mitigate interest rate risk! Since cash flows are future values they are not affected by interest rate movements. Moreover, any excess cash flow reinvested will be able to buy new cash flows at reduced costs. This is truly the value in bonds and we strongly recommend that pensions use bonds as their liquidity or Beta assets. Let the performance or Alpha assets be the non-bond assets. Use bonds to cash flow match pension benefits and expenses chronologically. This synergy of Beta and Alpha assets should secure benefits, reduce funding costs, and buy time for the Alpha assets to grow unencumbered.

Cash flow matching by any name (defeasance, dedication, immunization) may be the oldest fixed-income strategy. It should be the core portfolio of a pension and the fixed income strategy chosen by pensions today given the likelihood of higher interest rates. With stocks also struggling this year (S&P 500 -10.7% YTD thru 03/07/22), a cash flow matching bond allocation will buy time for the equity allocation to recover without any dilution to fund benefits and expenses. It isn’t too late to change your fixed income approach, as we are only in the 1st inning of what could be a full 9-inning game!