I suspect that those who read this blog regularly are likely able to finish this next point before they get to the end of the sentence. But it is worth repeating. The primary objective in managing a DB pension plan is to SECURE the promised benefits (liabilities) in a cost-efficient manner and with prudent risk. If everyone had focused on that objective 4 decades ago, instead of a return objective, we wouldn’t have a pension funding crisis today. Pension plans could have secured the promises with very little risk back in the early 1980s. In fact, investing solely in the Lehman Aggregate Index (now Bloomberg Barclays), one would have achieved a 40-year annualized return of 7.69%, easily beating most ROA objectives, with only a 4.65% standard deviation. Yes, you read that right – only a 4.65% SD over 40-years, which equates to a Sharp Ratio of 0.77.

One didn’t have to get fancy by adding a plethora of products/asset classes, reducing liquidity to meet benefits in the process, while enduring ever-growing contribution expenses. No, a simple strategy to invest 100% in fixed income would have solved all of your funding issues. All of them! Regrettably, we outthought ourselves and as a result, we are paying the piper today. Major cities are struggling under the weight of the contributions that they must make, as they take up more and more of the annual budgets. Corporate America has basically abandoned private pension plans. None of this had to happen if we had just remembered that the pension objective is to secure benefits.

We missed the opportunity in the early ’80s and again in 1999 when most pension plans were fully funded. We equated the yield of a bond with its return, which is not correct. As bond yields declined asset allocation “strategies” minimized the use of fixed income believing that bonds would be an anchor on returns. As a result, we subjected our plan’s asset bases to huge volatility, perhaps 3-4 times the volatility of the Aggregate index. As I wrote the other day, the main consequence of riding the asset allocation rollercoaster is the tremendous growth in contributions, which you can’t recoup.

At the end of 2021, we were imploring pension America to take risks off the table. Funded ratios had been improved and markets performed well above long-term expectations. Did anyone listen? Unfortunately, equity and fixed income markets have performed poorly to start the year. Funded ratios and funded status are under pressure. Inflation, the possibility of rising rates, and war in Europe are creating potentially huge headwinds for our pension systems. The good news: it isn’t too late to do something about it.

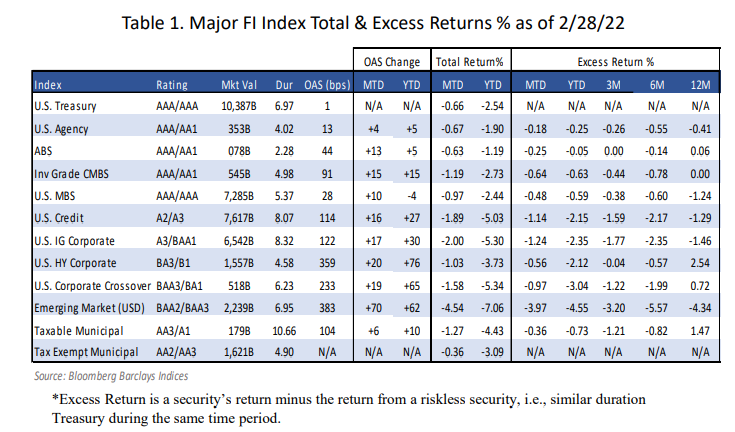

As we’ve discussed, traditional total return fixed income programs will be under stress in a rising rate environment. The 39-year bull market in bonds may have expired. It doesn’t take much of an interest rate move upward to generate some pretty ugly performance. The following chart from RW Baird highlights the impact in just the first two months of 2022 on a variety of fixed-income instruments.

Solution: Don’t use the fixed income assets for returns. Use bonds for their cash flows, as they are the only asset class with a known cash flow schedule of interest and principal payments (ie future values). One can construct a carefully matched portfolio of asset cash flows to liability cash flows to secure those promised benefits at both a reasonable cost and with prudent risk! Sound familiar? Defined benefit plans need to be protected and preserved as they are the only true retirement account. However, burgeoning contribution expenses are jeopardizing the future of these important vehicles. Let’s get back to pension basics. Treat your pension system as if it were a lottery system or insurance company. Understand what that future promise looks like and manage to it. Don’t let a return-focused asset allocation strategy guarantee more volatility with no assurance of success.