By: Russ Kamp, Managing Director, Ryan ALM, Inc.

I’ve witnessed quite a lot during my forty years in this business, but I’ve never seen anything quite like that which I’ve seen during the last couple of weeks. Given the current economic backdrop (high inflation and rising rates) coupled with the great uncertainty regarding the Russian invasion of Ukraine, stocks should not be rallying to the extent that they have relative to the performance of US Treasuries. I’ve previously referenced John Authers, Bloomberg, for the great work that he does in bringing clarity to confusing times through the presentation of impressive charts and graphs (some his and some borrowed). I’m borrowing one of his today to highlight the inconsistency in the equity market performance.

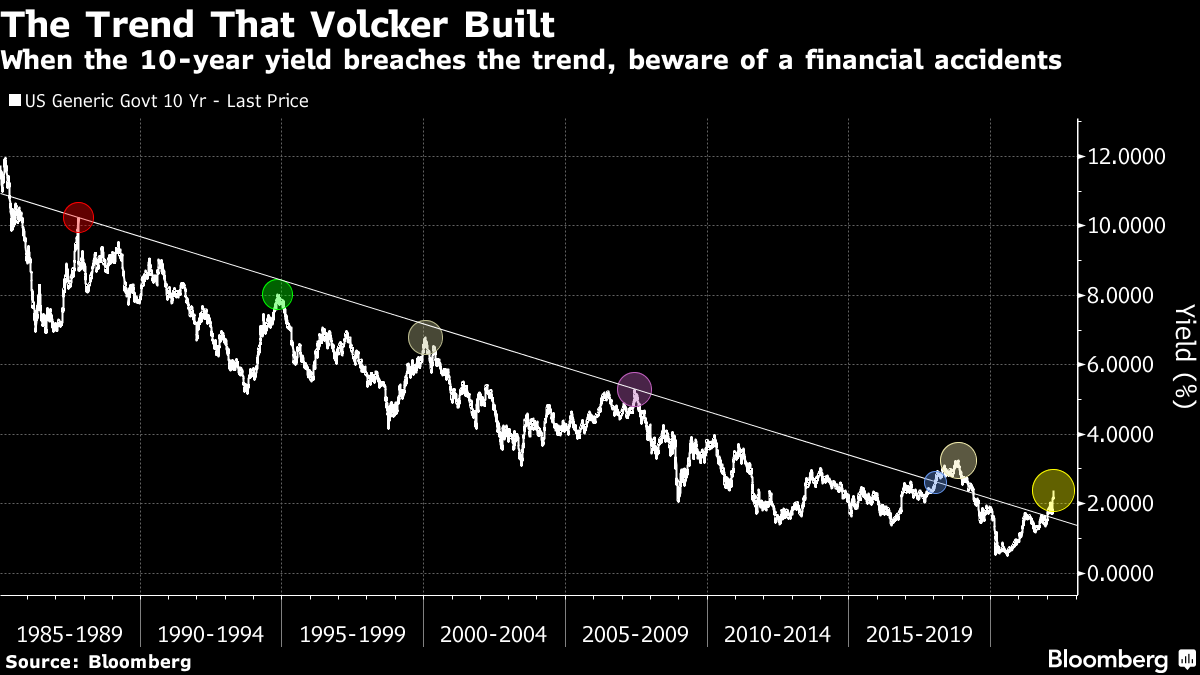

As John highlights and as we’ve pointed out on numerous occasions, our equity markets have been benefiting tremendously from the accommodative monetary policy since Volcker was the Fed Chair. The circles on the chart above highlight points in time when it looked like the downward trend in rates (10-year US Treasury note yield) was about to be reversed through Fed tightening. In each case, something dramatic occurred in the markets, such as the 1987, 2000, 2018 stock market crashes that forced the US Federal Reserve to once again provide easy money. The Fed was able to accommodate markets during those extraordinary occurrences because inflation was well-contained.

Today, we have consumer inflation at nearly 8% and producer inflation at almost 10%. There is little opportunity for the Fed to provide additional stimulus without seeing our current inflationary environment further spiral out of control. Given that the Fed has already indicated that it will move aggressively (potentially 6 more Fed Funds increases) to contain inflation providing stimulus should equity markets break is a non-starter. We know that rising interest rates will harm the performance of bonds, but as we witnessed during the 1970s, equities will also have great difficulty providing a real return in a high inflationary environment.

Most public pension systems are underwater from a funding standpoint despite strong equity markets since the Great Financial Crisis. We cannot allow the funded status to deteriorate further, which will lead to greater contributions, especially if the higher interest rates eventually lead to a recession. Asking taxpayers to provide additional funding for these plans during an economic downturn may just be the death knell for public pensions.

Pingback: This Doesn’t Make Sense – Now What? – Ryan ALM Blog

50% Fib retracement seems feasible.

[cid:image001.png@01D83EA6.FFEEE850]

Cheers,

Stuart | 415-674-4004 | Salt Lake City

nice to hear from you, Stuart. I hope that you are doing great. Russ