Please don’t tell me that the equity market’s afternoon swoon has to do with Powell indicating that a 50 bps move is on the table (if not locked in). Where have you been hiding if that is the case? Once again, the Fed’s greatest focus right now is on inflation. As Powell has said, “Economies don’t work without price stability.” In order to fight inflation, you need to remove stimulus from the economy. They don’t care what the impact is on markets. That isn’t their role nor should it be.

Category Archives: Uncategorized

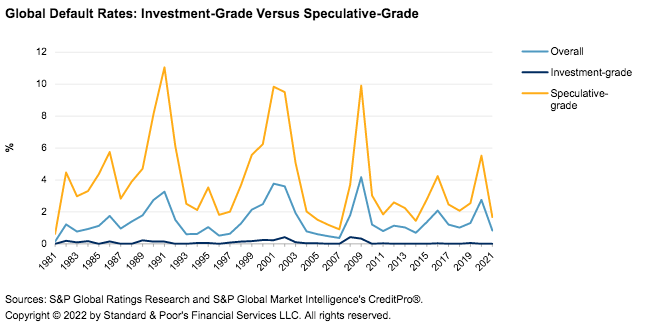

Is the Credit Rating Stupor About to End?

I warned bond investors just the other day about potential default risk escalating. The WSJ published an article yesterday about the potential impact of rising rates on leverage loans, which financed nearly $1 trillion in acquisitions just in 2021. Quarterly repricing helps investors, but it can damage the borrower. Roughly 15% of the outstanding loans are in companies that have a coverage ratio of <1.5X. The average company is >3X. The rapidity by which the Fed is raising rates may become a heavy burden for many lower quality bonds.

Rising Rates and the Impact on ARPA

By Russ Kamp, Managing, Director, Ryan ALM, Inc.

There was a little more activity related to ARPA and SFA approvals, which I will address in my next update. However, the bigger news surrounding ARPA is the impact of rising rates on both pension assets and pension liabilities. For those plans that have filed applications already, the impact of rising rates has more of an impact on the asset side of the equation. As a reminder, SFA assets are to be kept separate from the plan’s legacy assets. Under the Interim, Final Rules, the SFA assets received (7 funds have been paid to date) are to invest those proceeds in investment-grade fixed income. They can do that in one of two ways: either create a total return-focused portfolio or a cash flow match portfolio of plan assets to plan liabilities – the strategy that we at Ryan ALM espouse.

I suspect that those that have received their payouts have likely invested those assets in an IG portfolio designed to outperform some generic index – likely the BB Aggregate Index. If so, their assets have taken it on the chin as rising rates have impaired bond prices. For instance, the Aggregate index has declined on a total return basis by -8.8% YTD through April 19th. The biggest annual loss since 1981 is <3%. Oh, boy!

Depending on the size of the SFA payment, a pension system might be able to defease 8-12 years of pension liabilities. The present value (PV) of pension liabilities falls as interest rates rise, which provides a plan that is defeasing liabilities the opportunity to defease more of those future payments. As mentioned, the assets get hurt in a rising rate environment, but higher rates also help reduce future costs. Furthermore, once the defeasing strategy is constructed, the savings to the plan are locked in and assets and liabilities move in tandem whether that is up or down. Interest rate risk has been eliminated.

Now the liability news. The ARPA legislation calls for eligible pension plans to use either PPA’s 3rd Segment Rate + 200 basis points or the plan’s current discount rate, whichever is lower. A higher discount rate reduces the economic present value of pension liabilities, which impacts the amount of SFA to be received, so a rising rate environment would reduce the present value of that future liability. Fortunately, the legislation uses a 24-month average (unadjusted) to calculate the current 3rd Segment Rate, which as of April is 3.29% before the addition of the 200 bps. Despite the significant rise in rates in 2022, the 3rd segment +200 bps rate has not moved much at all, as US interest rates were in the 4% range for the 3rd Segment in 2020. As that year falls out of the 24-month calculation it is being replaced by a slightly lower # at this time.

We, at Ryan ALM, are not in the business of predicting rates. We are in the business of SECURING the promised benefits. Allowing pension assets to potentially swing wildly as a result of harmful interest rate moves is not a sound financial strategy. We highly recommend that plan sponsors defease pension liabilities with the SFA proceeds. As a reminder, the ARPA legislation’s goal was to secure the promised benefits for 30-years. We know that isn’t going to happen because of how the SFA is being calculated, but there is no reason to not secure benefits for as long as possible. Doing so allows the pension plan’s legacy assets to now grow unencumbered as they build to meet future pension liabilities. Rising interest rates are not a panacea for pension assets, but they do help pension liabilities and defeasement strategies. More to come on this subject!

Is the Credit Rating Stupor About to End?

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

S&P is out once again with its outstanding research on corporate defaults with the publication of the “2021 Annual Global Corporate Default And Rating Transition Study”. Despite significant issues related to business continuity from Covid-19, supply chain disruptions, inflation, etc. global corporation defaults remained incredibly low. As the chart below reflects, the last 40-years for investment-grade bonds reveal almost no defaults. Is the party about to end?

The US bond market has enjoyed an unparalleled 39-year bull market that has seen interest rates fall from the mid-teens in 1981 to historically low levels until recently. The US Federal Reserve has embarked on a potentially aggressive tightening path that may lead to significantly higher US interest rates. How will this trend impact those companies that have maintained their IG rating despite having modest interest coverage ratios that may become quite challenged in the near future? As a reminder, a significant majority of corporate debt issuance has been rated BBB, and that category now makes up >50% of all IG debt outstanding. Another interesting fact, despite the relative calm, overall credit quality has deteriorated. According to the S&P report, the “ratings distribution among companies we rate remained weak, with 14.5% of ratings at ‘B-‘ or lower as of year-end, up from 7.4% 10 years earlier.” Could this be the canary in the coal mine?

Total return bond products have had a very difficult start to 2022, with the Bloomberg Barclays Index (still the dominant index for Pension America) down 6% in the first quarter. To date, these bond funds have only had to deal with interest rate risk. Let’s see what happens when defaults escalate.

ARPA Update Through April 15th

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

We hope that you had a wonderful Easter or Passover celebration this past weekend. With regard to the PBGC’s latest update (as of April 15th), no new plans filed an application. The last to do so was the New York-based, Pension Plan of the Printers League – Graphic Communications International Union Local 119B, New York Pension Fund, covering 1,213 participants. This plan has filed an SFA application to receive roughly $85 million. To date, none of the Priority Group 3 members (>350,000 participants) have submitted an application with the PBGC.

We are pleased to report that two plans that had received prior notice that their applications had been approved received the payments totaling $238 million and covering 2,250 participants. This activity brings to seven the number of approved and paid SFA applications. Each of these plans filed its application under the Priority Group 1 category. As we reported last week, 36 plans have filed an application with the PBGC representing a very small percentage of the expected number of applications and $s associated with this legislation. Obviously, there is much more to come.

Ryan ALM Q1’22 Pension Monitor

We are pleased to share with you the Ryan ALM Q1’22 Pension Monitor. Despite the fact that pension assets had a challenging quarter, pension liabilities fell to a greater extent, as US interest rates rose rapidly in response to the US Federal Reserve’s intent to aggressively address the current inflationary environment. US corporate plans operating within a FASB construct appreciate this fact. Those plans – public and multiemployer pension systems – utilizing accounting methods under GASB are probably unaware that pension liabilities had substantial negative economic growth during the quarter, as they use the return on asset (ROA) assumption as the discount rate for their pension liabilities. Under this accounting framework, it appears that pension assets dramatically underperformed liability growth.

Given the significant differences produced by these two accounting methodologies, it is no wonder that inappropriate decisions with regard to contributions and benefits are made from time to time. An aggressive Fed may lead to significantly higher US interest rates. Will this action have a greater impact on pension assets or liabilities? Check-in with us at either ryanalm.com or kampconsultingblog.com to see how this story unfolds.

Not a Correlation of 1, But Certainly Strongly Positive

Bitcoin recently staged a strong recovery bringing the price back to nearly $47,000 after having tested the $32,000 level. Was this “recovery” driven by the currency’s own fundamentals or was it the result of the Nasdaq 100, which also enjoyed a strong rally in March? I’ve mentioned on several occasions that I believed that Bitcoin was trading more like a meme stock than an inflation hedge. Here’s a recent chart highlighting the correlation of Bitcoin with Nasdaq’s performance, which indicates an all-time high correlation of 0.695. I’m not surprised.

ARPA Update as of April 8, 2022

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

The PBGC has provided its most recent update on the filing of SFA applications and approvals. Since August 2021, 36 multiemployer pension plans have filed for Special Financial Assistance (SFA) under ARPA. To date, 10 plans have received approval from the PBGC totaling $2.04 billion of which $1.1 billion has been paid. All of the pension plans that have filed their applications have been in either Priority Group 1 or Priority Group 2. Priority Group 3 plans (those >350,000 participants) were eligible to begin filing as of April 1st. Fortunately, none of the plans that have filed applications have had their potential award rejected.

Given the estimated $95 billion in potential cost assigned to this legislation, there is much activity remaining, as only 2.1% of the estimated cost of the legislation has been awarded to date. Recent 2022 market performance for assets may help plans that have yet to file. A lower starting asset base will enhance the potential grant award. Lastly, we are still awaiting word from the PBGC on their Final, Final Rules. It has been nearly 9 months since the PBGC announced its Interim Final Rules.

Ryan ALM, Inc. Q1’22 Newsletter

We are pleased to share with you the Ryan ALM, Inc. Newsletter for the first quarter of 2022. Despite a very rough start to the year for the capital markets, the present value of pension liabilities (based on an average 12-year duration) underperformed the “average” asset allocation, by roughly 4.4%. As a result, Pension America once again witnessed an improving funded status. For pension plans that use GASB for their accounting standard, this outperformance on the part of plan assets versus plan liabilities may be hidden from view.

It’s the Magnitude That Has My Attention

By: Russ Kamp, Managing Director, Ryan ALM, Inc.

The first quarter 2022 performance returns are rolling in and as we’ve been reporting they aren’t good. They aren’t good for equities, VC, BONDS, and likely other segments of our capital markets! With regard to fixed income, the Bloomberg Barclays Aggregate Index (formerly the Lehman Aggregate) posted its weakest quarter since 1980. In fact, the -5.9% return during the first three months is nearly twice as bad as any quarterly result since the bond bull market took hold in 1981’s third quarter. The Aggregate index has posted negative quarterly results in 19% of the 162 quarters since the fourth quarter of 1981, so a negative result isn’t rare by any stretch of the imagination. However, the largest negative quarterly result during that entire time was only -3.37% registered during Q1’21.

Given the US Federal Reserve’s recent comments regarding their singular focus on nipping inflation in the bud, this result may become a trend. For comparative purposes, there have not been more than two consecutive quarterly losses in the last 40+ years. Will the likelihood of 6 more Fed rate increases to come lead to a string of negative results? Are pension sponsors prepared for this potential event? Remember: what might be quite negative for pension assets may in fact be beneficial from a pension liability perspective. Are you monitoring your plan’s liabilities regularly in order to carefully match pension assets with those liabilities? Call us. We will show you how it is done.