By: Ronald J. Ryan, CEO, Ryan ALM, Inc.

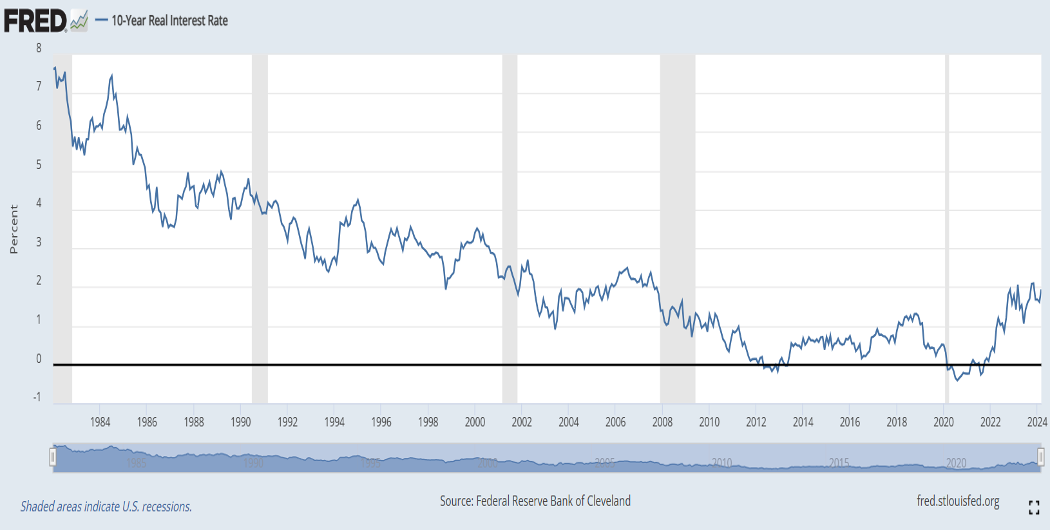

Chairman Powell and the Fed have consistently said they want real rates. The Fed primarily focuses on the Personal Consumption Expenditures (PCE) as their gauge of inflation. Currently the PCE is at 2.7%. What the Fed has not said is the target level of real rates. Historically, real rates as measured by the St. Louis Fed have averaged about 3.0% although the trend line has decreased steadily since the 1980s (see graph below). With the PCE at 2.7% today a 2% to 3% real rate would suggest a 4.70% to 5.70% 10-year Treasury nominal rate. With the 10-year Treasury at 4.66% today, it would seem that there is no reason for any cut in rates by the Fed. In fact, there may be more reason to increase rates.

The question remains… where will inflation (as measured by the PCE) level off? Who knows since there are too many factors to consider. The major causes of inflation today seem to be:

- Excessive Government Spending

Biden 2025 budget of $7.3 trillion is 12.3% higher than the 2024 budget of $6.5 trillion. Jamie Dimon, CEO of JP Morgan Chase, warns that excessive deficit spending is inflationary and that interest rates could spike up to 8%. The Biden Administration Student Loan forgiveness package could increase the deficit by $430 billion if successful.

- Oil Prices

West Texas Intermediate (WTI) Crude oil prices are up over 19% in 2024.

- Red Sea Attacks

About 12% of global trade goes through here to the Suez Canal. Ships now have to be rerouted around southern tip of Africa creating a delay of about two weeks at a cost of $3,786 per vessel or about $1 million per week. According to Drewry World Container Index costs are up over 90% YoY.

- Francis Scott Key Bridge Collapse

One of the largest ports in America handling $80 billion in cargo annually. Estimated closure costs = $15 million per day with closure expected for two to three years.

As always, the motto “let the buyer beware” (Caveat Emptor) seems to apply here.