We are very much looking forward to presenting “Pension Lessons Learned” with the Opal Group beginning on April 15th. This is the first in a series of Ryan ALM and Opal Group webinars addressing this important topic. But, in order to discuss potential lessons learned from this crisis, we need to reflect on what lessons were learned following the Great Financial Crisis of 2007-2009, when pension America saw its funded status plummet and contribution expense dramatically escalate.

Unfortunately, with regard to the private sector, we continued to witness an incredible exodus from defined benefit plans and the continued greater reliance on defined contribution plans, which is proving to be a failed model. That activity appears to have benefited corporate America, but how did that work for plan participants, who are now forced to fund, manage, and then disburse this benefit through their own actions, which is asking a lot from untrained individuals, who in many cases don’t have the discretionary income to fund these programs in the first place.

With regard to public pension systems, we saw a lot of action. There were steps to reduce the return on asset assumption for many systems – fine. But, that forced contributions to rise rapidly, creating a greater burden on state and municipal budgets that began to siphon precious financial resources needed for other social issues. In addition, there was great activity in creating additional benefit tiers, in which newer plan participants, and some existing members, were asked to fund more of their benefit through new or greater employee contributions, longer tenures before retirement, and more modest benefits to be paid out at retirement. Again, not a pension lesson learned, but a penalty for participants.

Multiemployer plans were certainly not immune to these developments. We have seen greater contribution expense and lower ROA targets for these plans, too, but have we seen improved funding? We have more than 300 multiemployer plans that went into 2020 in either Critical status or worse, Critical and Declining status. Given what has transpired in the markets to begin this year, it is highly likely that a number of other plans will have seen their funded status deteriorate to the point that they are also in Critical status.

It seems to me that most of the “lessons learned” have nothing to do with how DB pension plans are managed, but rather asks that plan participants bear the consequences of a failed pension model. A model to has focused on the ROA as if it were the Holy Grail. Pension plans should have been focused on the promise that was made to their participants, and not on how much return they could generate, which has done very little in terms of return, but certainly created a lot more uncertainty and volatility. As we’ve been reporting, equity and equity-like exposure within multiemployer and public pension systems was greater coming into 2020 then where they were in 2007. What lesson was learned?

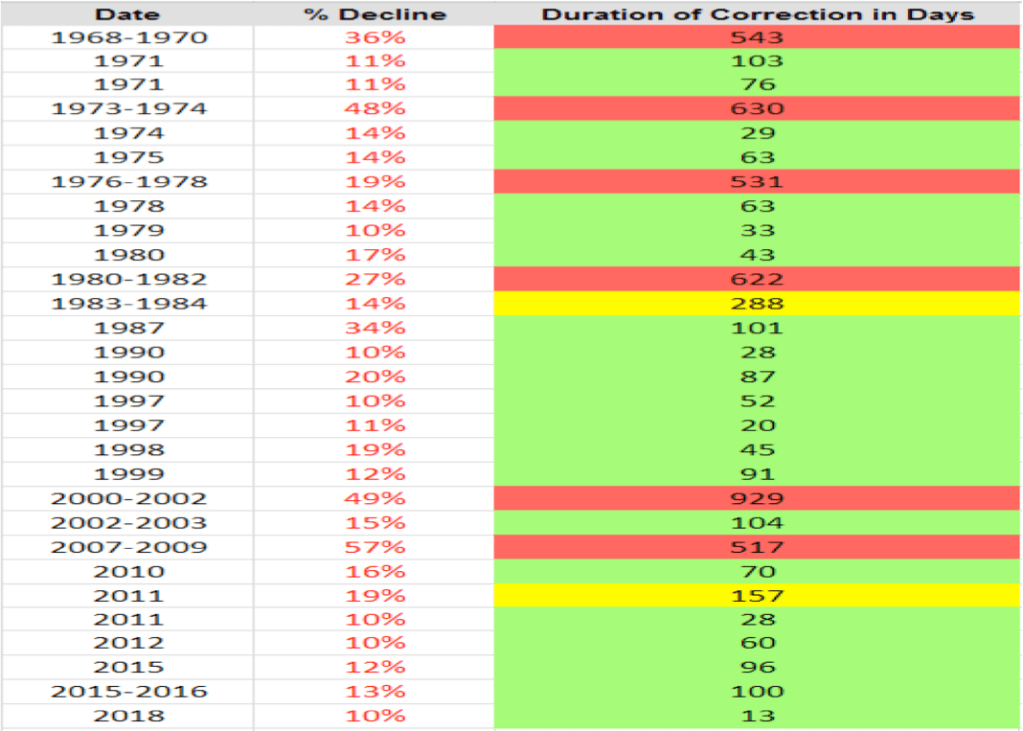

Pension America is once again suffering under the weight of declining asset values and falling interest rates. When will we truly learn that continuing to manage DB plans with a focus on return is NOT correct? The primary objective needs to be securing the promised benefit at low cost and prudent risk. Shifting wads of money into private equity and thinking that you’ve diversified away equity exposure is just silly. Too much money has flowed into private equity that would have likely diminished returns prior to our economy being shut down. The consequences from an economy that has been placed on life support are likely to result in private equity valuations being sliced by 33% to 50%. That won’t help a plan’s funded status!