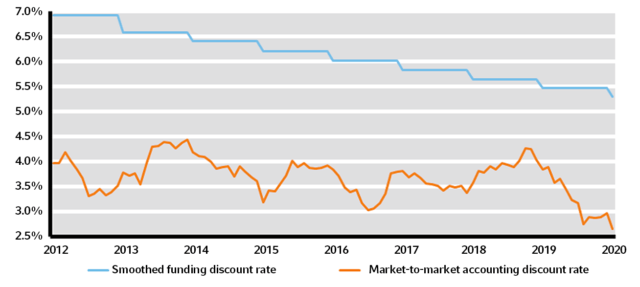

Corporate America continues to use different discount rate methodologies to measure and fund their pension plan’s liabilities. According to Russell Investments, the use of smoothing techniques (90%/110% corridor and 25 years) would create a discount rate of roughly 5.5% today, while a true marked-to-market discount rate would be about 2.5%. Plans claiming to be “fully funded” using smoothing are likely much worse off. The folks at Russell estimated that a plan claiming to be fully funded when using smoothing, would actually be only about 76% if the plan had a duration of about 12 years. A plan at 90% funded with an average duration of liabilities at 16 years might be truly funded at only 64%. Wow!

This certainly has implications for future contributions, PBGC premiums, the ability to engage in risk transfers, and other pension matters. Oh, and by the way, according to Russell “barring future changes to pension law, sponsors ought to be mindful of the coming phase-out of funding relief. With the ongoing decline in the 25-year average determined by the IRS, and the 90%/110% corridor expanding from 2021, the effects of funding relief will increasingly wear away. Contribution requirements will increase for many plans, bringing marked-to-market liabilities into economic reality.”

chicken and egg? NO, one should first use an appropriate discount rate objective then invest accordingly. Not, set a high discount rate then try to chase returns( like Central States Pension Fund) Notice corporate pensions are using 3-4.5% discount rates, and Central States was using 7.5%.

Hey Tom – Under ideal circumstances there would be ONE accounting standard (IASB) for the discounting of pension liabilities. Regrettably, we have three! It would be financially difficult to change this overnight, but some move over 10-15 years might be appropriate. Thanks.

Hello Russ, math is the language of science and math is the simple language of pensions. It is frustrating to hear non-mathematical people analyze the pension crisis. Because there was faulty math (inadequate contributions and/or pension over promises) there are victims–the human element. To me, there is a distinct difference between “earned” and “promised”. Earned is a mathematical term and promised is the human element. People should at least know why this crisis happened, and I’d venture to say that many do not. To repeat, inadequate contributions and/or over promises are the sole reason for the pension crisis, NOT active to retiree ratios, market downturns, poor investing and life longevity. These factors may exacerbate a faulty model, however. Adequate funding is all that is necessary.

Hi Tom – When DB pensions were first introduced, they were managed like lottery systems. They knew what that future benefit would cost and they took a present value calculation of that future benefit and they defeased that liability. The contributions were adequate for that benefit payment. There is no question that inflated discount rates reduced contributions inappropriately. When plans under contributed, they were forced to inject more risk into their asset allocation and the combination was like throwing gas on an open fire.

No DB pension plan should rely upon or need more bodies. Each participant’s benefit should be calculated and funded on its own or you do in fact have a Ponzi scheme. You are right, the math is the math. Trying to get more returns from the markets in lieu of contributions is just foolish. Unfortunately, those mistakes will not be corrected by trying to generate more returns at this time. In my humble opinion, the only way to close the funding gap is to provide an infusion of cash through a loan. The negative cash flow is too great to make up the underfunding now. Russ

Russ, you are exactly correct. You reiterated what I said in a somewhat different manner. Unfortunately, just knowing what happened won’t fix the damage. However, moving forward, hopefully these same mistakes won’t be repeated. At the least, I feel the Government owes the retirees and actives a complete explanation on what they specifically plan to do if anything—and soon!