By: Russ Kamp, Managing Director, Ryan ALM, Inc.

The recent banking crisis was driven in large part by the rapid rise in US interest rates that created losses for SVB’s investment portfolio (Treasury holdings) and other banks and drove depositors to seek higher yields available on short-term Treasuries (disintermediation). Fortunately, the intensity of the crisis has been moderated by the FDIC increase in insured deposits and the Fed Bank Term Funding Program, but are banks and the US markets in the clear? My crystal ball is no better than anyone else’s, but my guess is that the relative calm experienced in the last week or so may be premature.

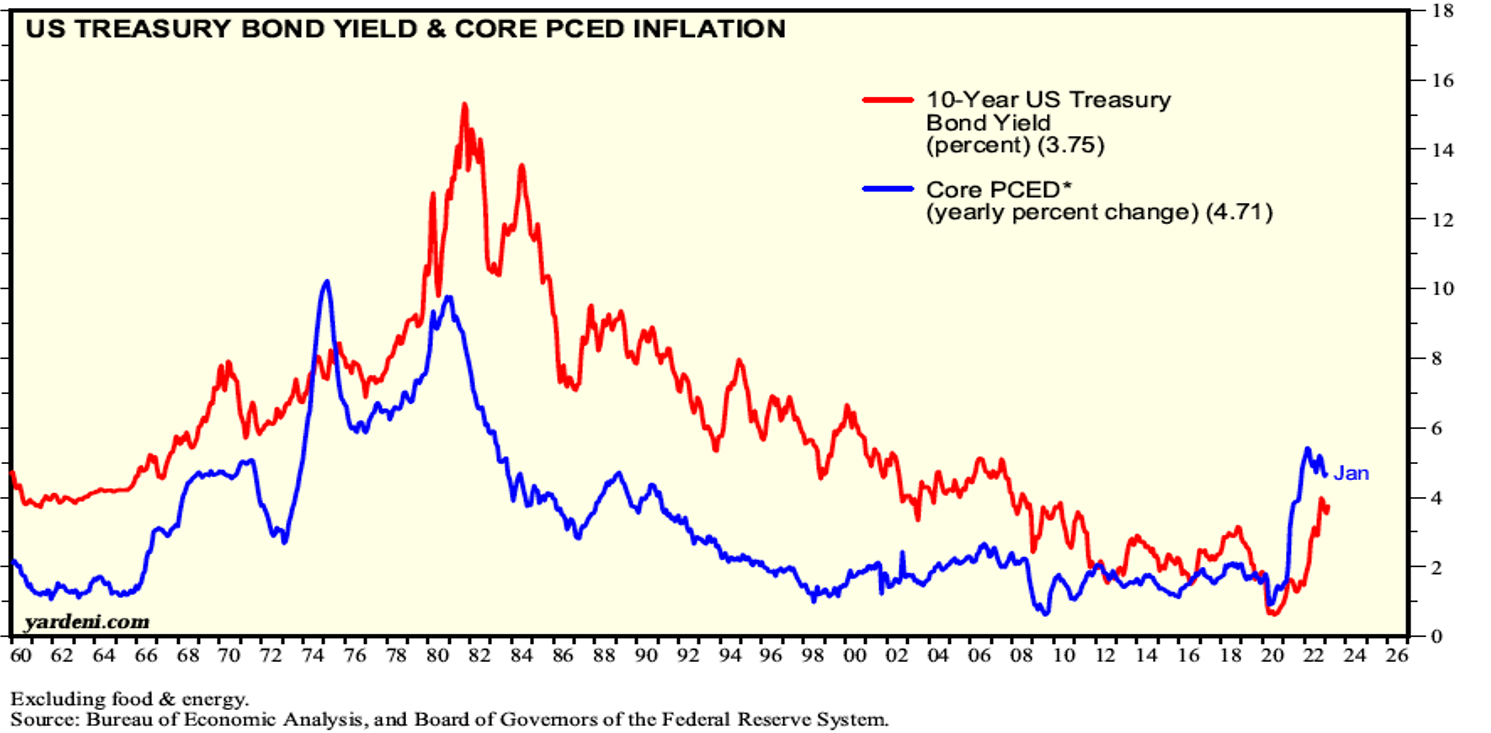

The Federal Reserve has indicated that its objective has not been completed. As a result, US rates, or at least the Federal Funds Rate, will continue to rise as the Fed tries to tamp inflation toward the 2% level. Today’s release of the PCE inflation (the Fed’s preferred measure) indicator highlights the fact that the Fed still has some work to do, as the 0.3% reading and 4.6% YOY result are still well above the 2% annual objective.

As if concerns related to the Treasury market aren’t enough, US Corporate bonds, which were issued at record levels during the pandemic are on the cusp of being refinanced at record levels too. The issue, historically low-interest rates have been replaced by much higher rates as the Fed tightens. The impact on Corporate America’s profitability may be meaningful. Here are some facts:

Bond issuance in 2020 stood at a record $2.275 trillion – up 60.4% over 2019.

80.1% of the issuance was investment grade.

As of 2021, the outstanding debt of nonfinancial corporations in the US was $17.7 trillion.

American companies owe > $10.5 trillion just in bonds relative to $8.8 trillion prior to the pandemic.

88% of bonds issued in 2020 are callable – it was 40% of issuance in 2005

Debt to EBITDA ratios have risen from 2.2 to 2.5.

The total nonfinancial debt to mature could reach $968.5 billion by 2025, compared to $570 billion in 2022.

Therein lies the problem. Will corporate America be able to successfully refinance the mounds of debt accumulated during the pandemic when US interest rates were at historically low levels or will the need to issue more debt as substantially higher rates impact a company’s R&D, dividend policy, earnings, employees, etc?

As Cash Flow Matching (CFM) specialists, Ryan ALM has chosen to invest almost exclusively in US corporate bonds, as they provide a premium yield that further reduces the costs associated with defeasing pension liabilities through asset cash flows. It is incumbent on us to make sure that none of our portfolio holdings default, as a situation such as that could substantially impact the portfolio’s ability to produce the necessary cash when needed. I am extremely pleased to report that Ryan ALM has never experienced a default in its nearly 19-year history. Our proprietary Approved List system has numerous quantitative and qualitative filters in our research process that have helped us avoid any potential disaster.