By: Russ Kamp, Managing Director, Ryan ALM, Inc.

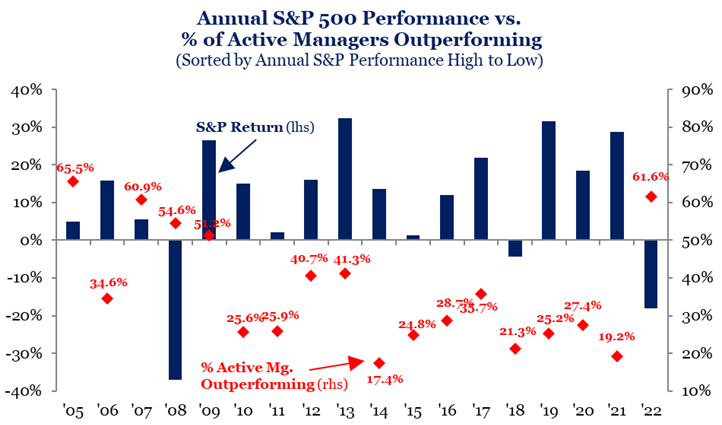

2022 proved to be a very good year for active large-cap (LC) US equity managers relative to the S&P 500 even if few managers made money on an absolute basis. For the first time since 2009, a majority of LC equity managers outperformed. It has been a long-time coming, but it shouldn’t be surprising.

Chart from Strategas Securities

The outperformance is a direct reflection of portfolio construction biases inherent in most equity strategies. First, the S&P 500 is a capitalization-weighted large-cap index that is driven by momentum. For the past 10+ years, Technology stocks lead the market and thus the S&P 500. This sector concentration and mega-cap biases made it very difficult for the average equity manager to outperform given their more equal-weighted exposure. Few managers construct portfolios with a cap weighting preferring to invest more equally in their portfolios. This creates an average cap weighting that tends to be much smaller than the index. Furthermore, most US equity managers overweight Value as a screening tool choosing portfolio holdings based on some relative price comparison – P/B, P/E, P/CF, P/S, and/or P/FCF. Again, the S&P 500 is a fully invested, momentum-driven, capitalization-weighted index that will beat a significant majority of managers in rising equity markets that have been enjoyed nearly annually since 2009.

So what happened in 2022? Well, we finally had a market that favored both Value and small-cap. With regard to Value, the S&P 500 Value index declined -5.1% in 2022, while the S&P 500 Growth Index was down a whopping -29.4%. With regard to small cap, the magnitude of the outperformance was more muted, but it still contributed to the outperformance of active managers relative to the S&P 500, as the S&P 600 was down -16.1% versus the S&P 500’s -18.1%. More important, the equal-weighted S&P 500 was down only -11.5%. Furthermore, we have a declining equity market that favored any firm that had a cash reserve, even a small one.

When all three market influences present themselves, it isn’t surprising that a majority of equity managers will outperform. What is surprising is the fact that only 61.6% of managers did. This gets back to the problem of fees. Not only do managers need to beat the S&P 500, but they need to do that after fees, which can be a difficult hurdle given how modest an index fee can be (< 5 bps).

What is the probability that these trends persist? As the graph below suggests, the Growth vs Value “cycle” tends to be lengthy. In this case, Growth’s underperformance has just begun. If previous cycles are any window into the future, it appears that Value has much more room to outperform. If that’s the case, it may be time to shift to more active equity strategies.

Graph by Ryan ALM, Inc.

Did you take some profits from your Growth manager(s) when it reached its most recent peak relative performance?