By: Russ Kamp, Managing Director, Ryan ALM, Inc.

At yesterday’s press conference following the release of the latest Fed Fund Rate (FFR) increase, Federal Reserve Chairman Powell was asked if he believed that financial conditions have eased, which would make the Fed’s job of combating inflation that much more challenging. His reply was somewhat shocking to me, as he said “no”. Really? The investment community has been aggressively buying US Treasury securities in the face of Fed tightening. How much? The US 10-year Treasury yield is currently 3.36% (9:15 am) having peaked at 4.25% just 3 months ago (10/24/22). That certainly seems like significant easing to me, and it isn’t relegated to the 10-year either, as the yield curve’s inversion has grown steeper.

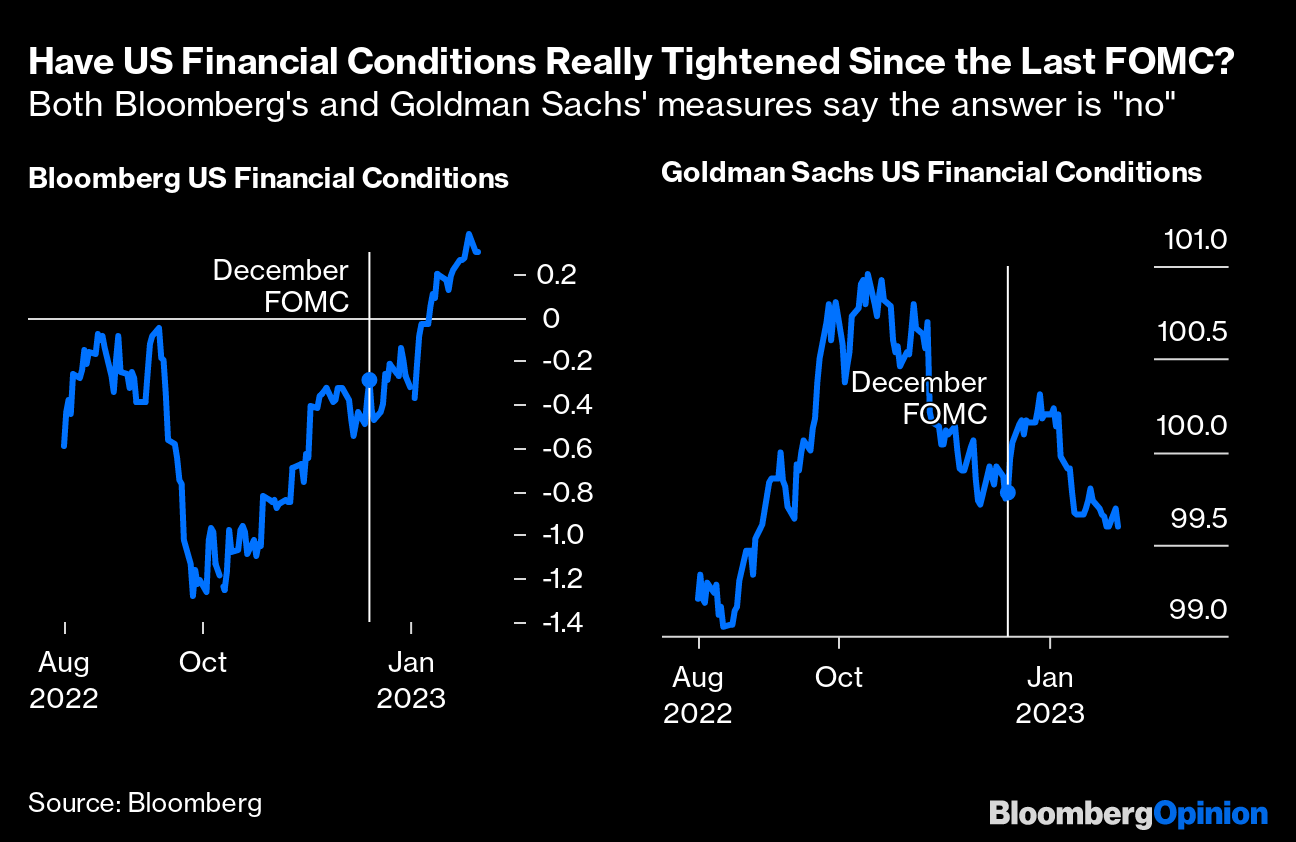

As further proof of financial conditions easing, I share with you two charts. The graph on the left is from Bloomberg and the one on the right is produced by Goldman Sachs.

Bloomberg’s financial conditions reading shows easing when the line is rising, while Goldman’s highlights easing when the line is falling. Clearly, these two readings are in sync. Both measures are revealing considerable easing. Powell may not believe that conditions have eased, but clearly, economic growth is not being thwarted to any great measure. We still have an incredibly strong labor market environment with wage growth that may be moderating still showing 5%+ annual growth. Mortgage and auto loan rates have fallen by 1% or more from peaks achieved in the fourth quarter.

Again, Powell may not currently recognize the easing, but eventually, he’ll have to come to that conclusion. Powell and the Fed Board have reiterated their posture of further increases, yet those pronouncements are being ignored by the “STREET”. If in fact, economic conditions have eased (dramatically) the Fed may be forced to continue to raise the Fed Funds Rate aggressively until they actually achieve the desired 2% inflation rate. The investment community cheered Powell’s comments regarding the future path of smaller increases, and I believe that they still anticipate rate cuts before year-end. I just don’t see it and neither does the Fed. One of these entities (the Fed or investment community) will have significant egg on its face come December. How that translates into market performance is anyone’s guess at this point.