By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Well, Wednesday, April 12th marked another release of a CPI data point. As predicted, headline inflation as measured by the CPI showed a reduction in the annual rate that was slightly better than forecast. As a result, both equity and fixed-income markets rallied rather dramatically at the open. If the headline was all you read, your response to the news would have been understandable, but if you took the time to dig a little deeper, it wouldn’t have taken long to read that the “core” inflation reading had actually risen to 5.6%. I’m not sure that I could do the “new math” being taught to fourth graders, but I do appreciate the fact that 5.6% is well above the Fed’s 2% target inflation rate.

You see, the US Federal Reserve continues to promote the idea that they are focused (singularly) on creating price stability. Furthermore, they have announced that they will NOT pause the increases in the Fed Fund’s Rate (FFR) until it is clear that inflation is on a meaningful path to that 2% level. So far, that evidence hasn’t presented itself. How long that takes is anyone’s guess?

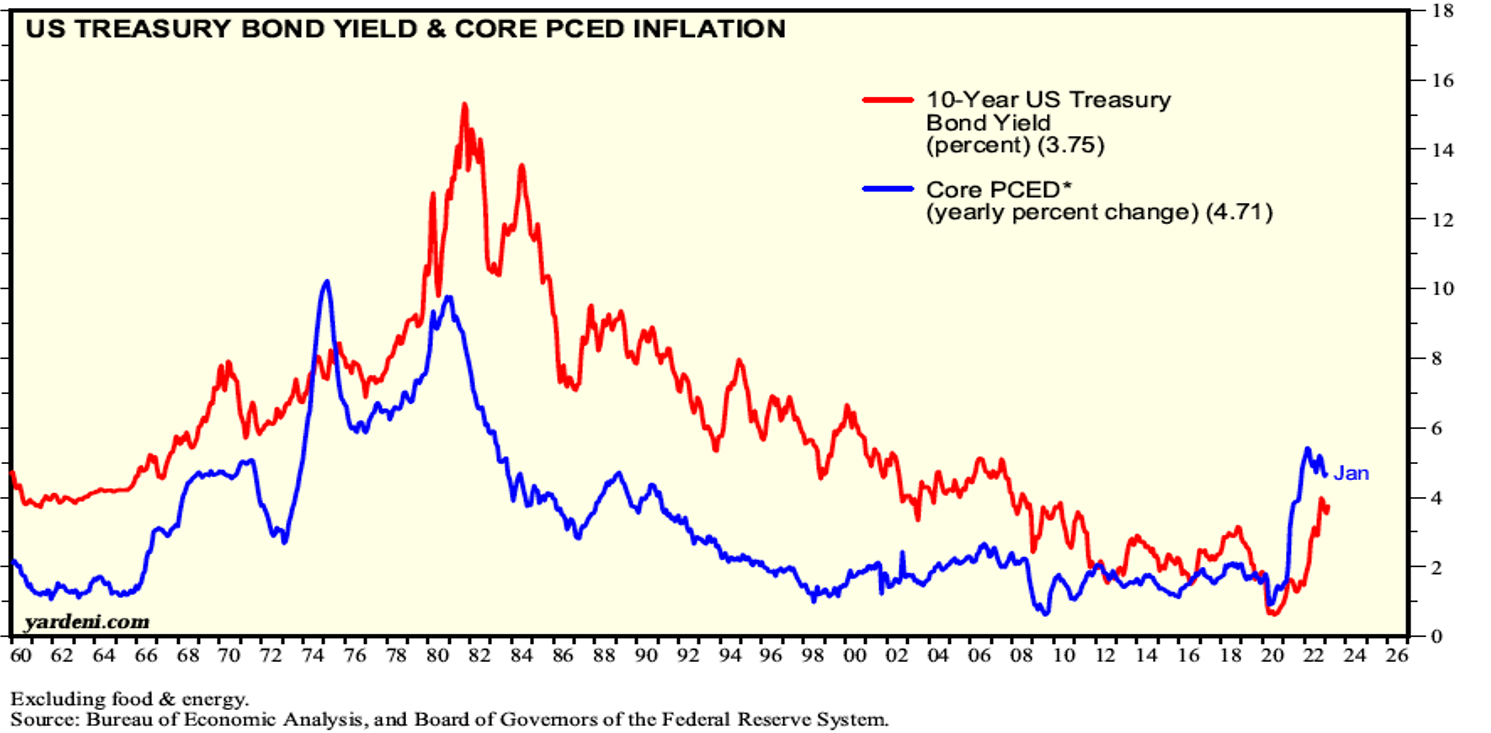

I recently attended the TexPERS conference in Austin. I had the pleasure of listening to Richard Bernstein, CEO/CIO, of Richard Bernstein Advisors, discuss the current economic environment. I think that Richard does a great job getting behind the numbers. The chart below was shown during his session. It is published by the Federal Reserve Bank of Atlanta. I found the information to be both dramatic and compelling. Again, if you are only focused on the headline CPI then this data is likely new to you. Most meaningful to me is the fact that 6 of 9 important inflation indicators are now higher than they were one year ago just before or concurrent with the FOMC’s first increase in the FFR. As you know, there have been an additional 8 increases bringing to 4.75%-5.0% the current level for the FFR.

Despite these facts, there was a euphoric response to the announcement of today’s CPI. Do market participants really think that they know more than the Fed? Do they think that the US Federal Reserve is kidding when they say that they don’t see an easing in rates this year? Have the last forty years of easy money and Fed support anytime there was a wobble in the markets really clouded judgment today? Fortunately, I am not in the game of forecasting interest rates. Our focus at Ryan ALM is taking the guessing risk out of investing by carefully matching asset cash flows through investment-grade bonds with a pension’s liability cash flows. Not having to guess how markets react is so comforting. Being able to tell your plan participants that their benefits are SECURE is equally, if not more, comforting. I highly recommend adopting a Cash Flow Matching strategy that gets you out of the game of guessing not only actions that are outside of your control but the market’s reaction to those events, which aren’t always logical.